Loan Officers

Lead Generation for Mortgage Loan Officers: The Complete Playbook

.png)

Summary

- What this covers: Eight lead generation strategies for mortgage loan officers, ranked by cost and time to ROI.

- Why it matters: Trigger leads are gone. Purchased lead economics are brutal. The lenders winning right now are the ones with systems, not just tactics.

- What you’ll identify: Which mortgage lead gen strategies fit your situation, and how to layer them into a system that builds over time.

- What’s included: A channel-by-channel breakdown, a self-assessment scorecard, and a framework for building a mortgage lead gen system you own.

- Who it’s for: Loan officers and mortgage brokers who want to stop depending on purchased leads and start building a pipeline that compounds.

Most loan officers watch a volatile rate environment and wait. Waiting for rates to settle, for volume to come back, for borrowers to start calling again. Meanwhile, the contacts sitting in their database are quietly checking their home values, running equity scenarios, and wondering if the numbers make sense yet. Those LOs have no idea.

Mortgage lead generation has always rewarded loan officers with a system over the ones with a strategy. Trigger leads are gone (RIP). Purchased lists convert at 1-3%. The borrowers most likely to transact with you aren't on someone else's data file. They're already in your database, and they're already thinking about it.

This guide covers how to find them, and how to build the pipeline infrastructure that surfaces opportunities in any market.

3 Reasons Why Lead Generation for Mortgage Has Changed

The rules, the economics, and the competitive landscape have all shifted at the same time. Here’s what’s different and why it matters for how you build your pipeline.

1. Trigger Leads Are Gone

As of March 5, 2026, the trigger leads ban is in effect. Credit bureaus can no longer sell the data of consumers who just had their credit pulled. The carve-outs are narrow: an existing relationship or explicit consumer consent.

The interrupt-based prospecting channel that let lenders poach borrowers mid-application is closed.

2. Purchased Lead Economics Were Already Broken

The ban didn't change the math. It just made it harder to ignore.

- Shared purchased leads convert at 1–3%

- Exclusive leads rarely close more than 1 in 20

- Cost per funded loan from purchased sources often exceeds $1,000 once you factor in lead cost and time spent on unqualified contacts

Most high-producing LOs figured this out years ago. The ban accelerated a shift that was already underway.

3. The Math Has Always Pointed to Relationships

87% of mortgage business comes from referrals and past clients:

- 50% from referrals

- 37% from existing lending relationships

- Agent-referred leads convert at 15–25%

The highest-producing loan officers aren't spending the most on leads. They've built systems that make their relationships do the work.

The 8 Best Lead Generation Strategies for Mortgage Loan Officers

These aren’t ranked by what sounds impressive. They’re ranked by where your time and money compound fastest. The highest-ROI channels are the ones closest to you, your database, your agent network, your reputation in the communities you’re already part of.

1. Your Existing Database: The Highest-ROI Mortgage Lead Gen Strategy You’re Ignoring

If you've closed 50+ loans, you have 50+ people who already trust you and own a home that's changing in value every month. No lead vendor can give you that.

The problem isn't the asset. It's the system. Most borrowers forget their LO's name within a year of closing despite being satisfied customers who would gladly refer. Without consistent touchpoints, that relationship decays.

What a database system looks like in practice:

- Monthly personalized outreach: Not a newsletter. Something specific to each client's home value, equity growth, and refi scenario at current rates. Generic market updates don't produce results because they're not relevant to anyone in particular.

- Behavioral signals: Clients who are quietly running refi scenarios or engaging with home value data are often closer to transacting than the ones who call out of nowhere.

- Triggered outreach: Rate drops, listing alerts, equity milestones. Natural moments to reach out with something relevant.

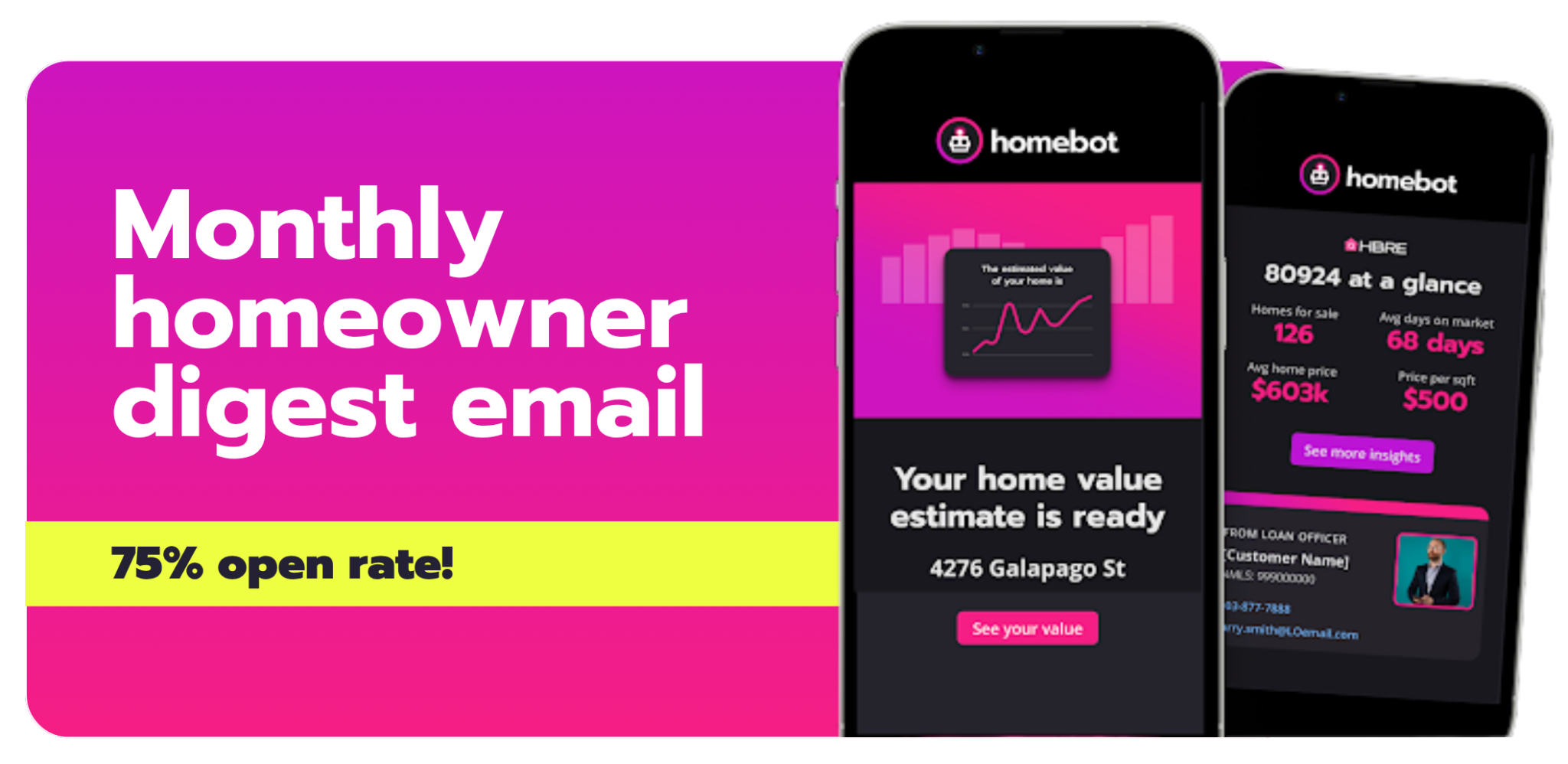

Homebot's Home Digest automates the monthly touchpoint, delivering personalized home wealth insights under your name with a 75% open rate. When clients show engagement signals, the platform surfaces them so you're calling people who are already thinking about it.

✅ Quick Check: How many loans did you close 2–4 years ago? Those clients are your highest-probability refinance leads right now. Do you have a system to reach them before a competitor does?

2. Real Estate Agent Partnerships: The Highest-Volume Purchase Lead Source

Agent referrals convert at 15-25%, compared to 1-3% for shared purchased leads. The math isn’t close. If you close 20 purchase loans this year, the majority will trace back to an agent relationship.

The challenge is building those relationships without wasting time on agents who aren’t looking for a new lender partner. A few realities worth knowing:

- The top-producing agents in your market are fielding pitches from 30+ lenders. Cold outreach to them rarely works.

- The agents most open to new lender relationships are mid-tier producers: closing 15-30 transactions a year, trending upward, buyer-side focused, not locked into an exclusive arrangement.

- 96% of top loan officers say their strongest referral source is agent partners, which means the competition for those relationships is real.

Building agent partnerships that actually produce:

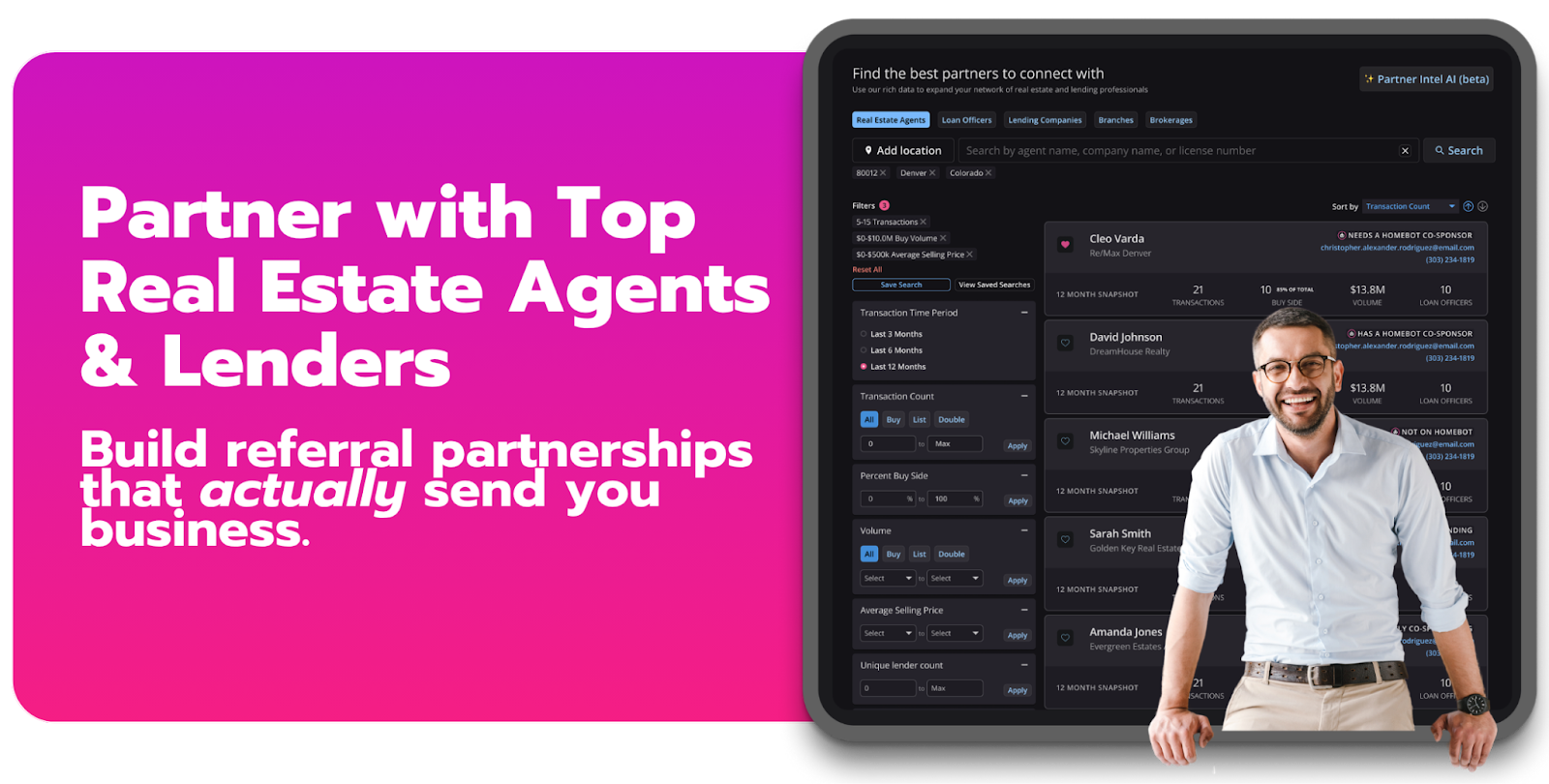

- Find the right targets first: MLS data filtered by production volume and buyer-side representation. Homebot’s Partner Intel lets you search agents by location, volume, and partnership status, so you know who’s available before you reach out.

- Lead with value, not a pitch: The 3-touch outreach sequence that works: something useful about the market → a specific financial breakdown on one of their listings → a coffee ask. No pitch until you’ve given something.

- Co-brand on their client base: When you’re working with an agent, Homebot’s co-sponsorship feature automatically brands both of you on the borrower’s monthly home digest. The agent’s clients see both of you as their trusted team. When they’re ready to move, you’re already their lender.

✅ Quick Check: How many of your active agent partnerships sent you a referral in the last 90 days? If the answer is fewer than half your partners, you have inactive relationships that need either more value or a cleaner exit.

3. Past Client Referrals: The Lead That Costs Nothing

Most mortgage leads come from referrals.. Not from leads you bought. Referred leads also have a 30% higher conversion rate than non-referred borrowers, because they arrive with trust already built.

Here’s the foundation of a strong referral system:

- Be memorable after closing: Most LOs do the work to earn a referral, then go invisible and never get it. The period right after closing, and the 12 months that follow, is when your relationship either compounds or decays. Consistent touchpoints with real value keep you in the category of “my loan officer” rather than “someone I used once.”

- Make it easy to refer: When clients think of you for a friend, they need to be able to surface your contact info effortlessly. If they have to dig through old emails to find your number, the referral often doesn’t happen.

- Create referral moments: Rate drops, home value milestones, equity increases, these are natural moments when past clients think about their home and, by extension, you. A timely, relevant touchpoint at those moments increases the probability they’ll mention you to someone who’s thinking about buying or refinancing.

The clients most likely to refer are the ones still hearing from you. Monthly home wealth insights keep you top of mind passively, so when a friend mentions they’re thinking about refinancing, your name comes up naturally.

4. SEO/GEO and Content: The Lead Gen Channel That Compounds

SEO and organic search leads convert at 14.6%, higher than paid social and comparable to referrals. The difference is time: SEO takes 6-12 months to build, but once it’s running, it generates leads without ongoing spend.

There's now a second layer to this channel worth building alongside it. Generative Engine Optimization (GEO) is the practice of structuring your content so AI tools like ChatGPT, Perplexity, and Google's AI Overviews cite you when borrowers ask questions.

- AI-referred sessions jumped 527% year-over-year in the first five months of 2025..

- AI Overviews now appear in 20% of Google searches, and 47% of brands still have no GEO strategy.

The content that drives both SEO and GEO traffic is the same: educational, intent-specific, and local.

- “how to refinance with bad credit in [city]”

- “FHA loan requirements [state]”

- “how much house can I afford on $80K salary.”

These are high-intent searches from people actively exploring a home financing decision.

What an effective SEO/GEO content strategy looks like:

- Local SEO first: Your Google Business Profile should be complete, reviewed, and updated regularly. Local searches ("mortgage broker [city]") convert at higher rates because the person is ready to work with someone specific.

- Answer real borrower questions: Use Google's "People Also Ask" sections to find what your target clients are actually typing. Write answers that are genuinely useful, with specific details and cited data. Content with proper schema markup shows 30–40% higher visibility in AI-generated answers— structure matters as much as content.

- Build authority over time: One well-written post per month that answers a real borrower question compounds into a library of traffic. Consistency matters more than volume.

- Write for AI citations, not just rankings: Generative engines prioritize content that is well-organized, easy to parse, and dense with meaning. Short paragraphs, clear headers, bullets, and cited stats are the same things that make content readable for humans and referable by AI. You're not doing extra work. You're doing the same work better.

The compounding effect here is real. SEO and GEO bring new clients in the door. Your database engagement system keeps them connected long enough to refer and return. Each channel makes the other more valuable over time.

5. Google Ads and Paid Search: Fast Pipeline, Expensive Economics

Paid search puts you in front of borrowers actively searching for mortgage services right now. Unlike SEO, it can work immediately. Unlike social advertising, the intent is explicit, someone searching “mortgage rates [city]” is at least exploring.

The trade-off is cost.

- Average cost per funded loan from purchased leads can exceed $1,000 when conversion rates are low.

- Paid search typically runs $50-150 per lead with a 5-10% close rate

- Which means $500-$3,000 per funded loan depending on market and product type.

Paid search works best as a supplement to relationship-based channels, not a replacement for them. Use it to fill pipeline gaps, test messaging, or capture demand in new markets, not as your primary mortgage lead gen system.

✅ Quick Check: If you’re running paid search, calculate your cost per funded loan (not cost per lead). If it’s over $1,500, your organic and referral channels are almost certainly more efficient.

6. Social Media and Video: Awareness That Converts Slowly

Social media is a brand-building channel, not a direct lead channel. Conversion rates from social leads to closed loans run 1–3%, but the compounding effect on awareness and referral velocity is real over time.

What works:

- Short-form video on mortgage concepts: Reels and TikToks answering questions like "What's the difference between pre-qualification and pre-approval?" or "How does a rate buydown work?" build authority with first-time buyers who are just starting to research.

- LinkedIn for professional relationships: Not a consumer channel, but where you build credibility with the real estate agents, financial advisors, and HR managers who refer clients to mortgage professionals.

- Consistency over polish: A smartphone video posted every week outperforms a professionally produced video posted once a quarter.

The person who watches your content for three months before reaching out is already warm. Social builds the relationship before the conversation starts.

If you want a deeper framework for turning content into clients, Neel Dhingra's content strategies for loan officers breaks down the exact hooks, formulas, and posting cadence that convert viewers into referrals.

7. Community and Networking: The Long Game That Works

First-time homebuyer seminars, relationships with HR departments at large local employers, partnerships with financial advisors and CPAs who work with clients nearing a home purchase, these channels are slow to build and hard to scale, but they produce borrowers with no competition and high close rates.

A few that work specifically for mortgage:

- First-time buyer education events: In partnership with a real estate agent or local community organization, a quarterly seminar on the homebuying process generates leads who haven’t entered a competitive marketplace yet. You’re their first point of contact with a mortgage professional.

- Employer benefit partnerships: HR departments at companies with 100+ employees are often interested in financial wellness benefits for their employees. A lunch-and-learn on homebuying or a one-page guide distributed at onboarding costs almost nothing and positions you as the resource before the employee starts searching elsewhere.

- Referral relationships with CPAs and financial advisors: These professionals work with clients who are building wealth, inheriting money, and making financial decisions that often include home purchases or investment properties. A relationship where you provide mortgage expertise to their clients, and they refer those clients to you, is a high-quality, no-cost lead source.

- Industry trade shows and conferences: Events like MBA Annual, NAMB National, and regional mortgage conferences put you in the same room as referral partners, wholesale reps, and high-producing peers whose networks you can tap. The leads don't come from the trade show floor directly — they come from the relationships that follow. A conversation with the right agent team or title rep at a conference can produce more referral volume than months of cold outreach.

8. Online Listing Portals and Lead Aggregators: The Expensive Floor

Zillow, LendingTree, Bankrate, and similar platforms generate leads at scale, but the economics are challenging and the leads are shared with competitors. Shared leads convert at 1-3%. By the time you account for lead cost and time spent on unqualified contacts, the cost per funded loan often exceeds what you’d pay through more efficient channels.

These platforms work for some loan officers in some markets, particularly when response time is extremely fast and follow-up is systematic. But they’re rarely the foundation of a durable mortgage lead gen system. They’re a supplement to channels you own, not a replacement for them.

Building a Mortgage Lead Gen System, Not Just a List of Tactics

The loan officers consistently generating pipeline aren’t doing all eight of these things at once. They’ve built a system with a few core channels that compound over time, and they add to it deliberately as capacity allows.

A starting framework for most loan officers:

- Foundation (start here): Database engagement + past client referrals. This is your lowest-cost, highest-converting pipeline. If you have 100+ past clients and no systematic touchpoint system, that’s your first priority.

- Growth layer: Agent partnerships. Two or three productive agent relationships generating regular referrals will outperform most paid channels in volume and conversion rate.

- Acquisition layer: SEO content and local presence. Blog posts and Google Business optimization compound over time and generate inbound leads without ongoing spend.

- Demand capture: Paid search as a tactical supplement when pipeline needs filling.

The system doesn’t have to be complex. What it has to be is consistent. An LO with a simple database engagement tool running every month and two active agent partnerships will out-generate an LO with 12 disconnected tactics and no follow-through on any of them.

Mortgage Lead Generation Scorecard

Rate your current system on each channel from 1-3: 1 = nothing in place, 2 = inconsistent/manual, 3 = systematic and running.

Score interpretation:

- 8–12: Significant gaps. You’re likely overspending on lead acquisition and underinvesting in channels you own.

- 13–19: Partial system. Some channels are working but others are leaking opportunity.

- 20–24: Strong foundation. Focus on optimizing the channels already running before adding new ones.

Conclusion: Own Your Pipeline Before You Buy Someone Else’s

Trigger leads are gone. Purchased lead economics are getting harder, not easier. The loan officers who will have the most durable businesses over the next five years are the ones building lead generation systems based on relationships they own, not data they rent.

Your database, your agent network, your reputation in the communities where you work: these assets compound with time and investment. A purchased lead starts decaying the moment you receive it.

Homebot gives loan officers an automated system to stay connected with their database, identify when past clients are ready to transact, and build the kind of consistent, valuable relationship that generates referrals without you having to ask for them. It’s not a lead vendor. It’s the infrastructure that turns your existing relationships into a durable lead generation engine.

Book a demo to see how it works with your actual book of business.