Loan Officers

How to Increase Loan Volume Without Buying More Leads

You're a loan officer in a market that's finally moving again. Rates are coming down. Refis are picking back up. Buyers who've been sitting on the sidelines are starting to look. The opportunity is real.

So why does growing your loan volume still feel harder than it should?

For most loan officers, the instinct is to buy leads. More leads, more pipeline, more closed loans. It's a logical idea, but the math makes it a difficult business to sustain. Shared leads convert at 1–3%. Exclusive leads at 2–5%. By the time you factor in cost per lead and close rate, you're spending thousands of dollars for every funded loan, chasing borrowers who didn't ask for you and are getting called by four other LOs at the same time.

The loan officers who are consistently growing their pipeline, in good markets and slow ones, have mostly stopped depending on that approach. They've built something that compounds instead of resets every month. This guide shows you exactly how to do the same.

Why Purchasing Mortgage Leads Doesn't Build Volume

Before getting into what works, it's worth understanding why purchased leads are such a difficult foundation for sustainable loan volume growth. Most LOs already sense this, but the numbers make it concrete.

1. You're not the only one calling

When you buy a shared lead, that contact is sold to multiple lenders at the same time. The borrower didn't ask for you. They filled out a form and now they're getting bombarded. By the time you dial, your competitors already called.

The numbers tell the rest of the story:

- Shared leads convert at 1–3%

- Exclusive leads convert at 2–5%, but you're still closing fewer than 1 in 20

- When the deal closes, the relationship ends there

You've bought a transaction, not a client. And next month, you start over.

2. The trigger leads landscape just changed

Trigger leads used to be one of the most common prospecting tactics in mortgage: buying data on borrowers who just had their credit pulled by another lender. That window has closed.

The Homebuyers Privacy Protection Act (H.R. 2808) went into effect in early 2026. Here's what changed:

- Credit bureaus can no longer sell trigger lead data except under narrow exceptions

- Interrupt-based outreach is getting harder, not easier

- LOs building relationship-based channels now will be better positioned when it does

3. Purchased leads don't compound

This is the biggest problem with purchased leads: every dollar you spend produces, at best, one transaction. A referral compounds.

Here's what that looks like in practice:

- The agent keeps sending business because you delivered

- The past client refers their neighbor

- The relationship grows without additional spend

That's why 50–70% of a loan officer's income comes from past clients and referrals, not paid sources. The highest-producing LOs aren't spending the most on leads. They've built systems that make their existing relationships do the work.

So what does that system look like? It comes down to four things every loan officer can build, regardless of market conditions or budget.

How to Increase Loan Volume Without Buying Leads: 4 Strategies That Build Over Time

None of these strategies require a big budget or purchasing leads. They do require consistency and a clear plan. The sections below break down each one with the specific tactics, scripts, and systems you need to actually execute.

Strategy 1: Build Real Estate Agent Partnerships That Actually Send Business

Agent partnerships are the single most effective source of purchase loan volume for most loan officers.

Agent-referred loans convert at 15-25% compared to the 1–3% you get from purchased leads because:

- The borrower already trusts you because someone they trust vouched for you.

- The conversation starts warm instead of cold.

- The deal moves faster and closes more often.

The challenge for most LOs isn't understanding why agent partnerships matter. It's knowing how to build them without burning hours on networking events that go nowhere and cold outreach that gets ignored. Here's a system that actually works:

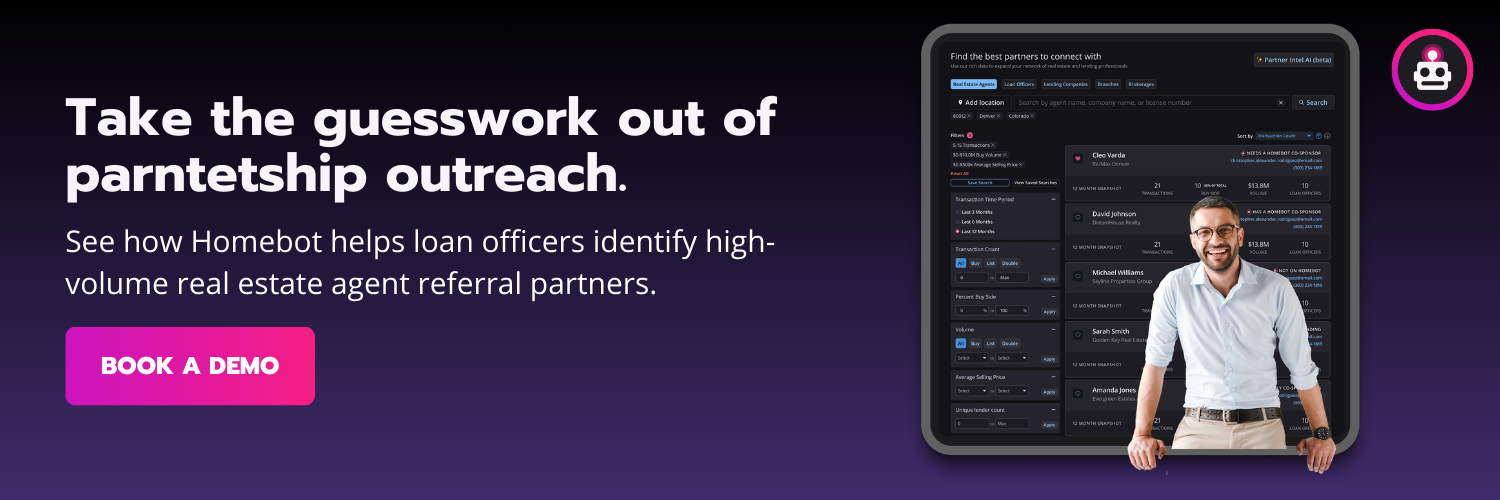

- Know who to target (not who you think)

The instinct is to go after the top producers. The agents doing 80 deals a year whose names you've seen on every yard sign in town. Those agents are fielding pitches from 30+ lenders. Your cold email is not going to break through, and even if you get a meeting, they already have a preferred lender they're not looking to replace.

The agents who are most open to building new lender relationships, and who have the most to gain from a strong one, look like this:

- Closing 15–30 transactions per year, with volume trending upward over the past two years

- Focused primarily on the buyer side, which means they need a lender on every deal

- Not locked into an exclusive lender relationship

- New to a brokerage in the past 12–18 months, or recently went independent

You can build this list by pulling MLS data in your market and filtering by transaction volume and buyer-side representation. Homebot's Partner Intel lets you search agents by location, production volume, and partnership status so you know who's actually available before you reach out.

- The 3-touch outreach sequence

The mistake most LOs make is pitching in the first message. Agents get pitched constantly. The LOs who stand out lead with something useful before they ever ask for anything. Here's the sequence that works:

- What to offer at the first meeting

Most LOs show up to the first meeting and talk about themselves. Their rates, their speed to close, their communication style. That's table stakes and the agent has heard it from every lender they've ever met. Come with something concrete they can use instead:

- A co-branded buyer financing PDF they can hand out at their next open house

- A market update specific to their farm area that includes mortgage rate context, formatted for them to share with clients

- An offer to send their past clients monthly home value reports with both your name and theirs on it, so the agent stays in front of their own database without doing any additional work

That last offer is worth spending a moment on. When you co-sponsor an agent through Homebot, your past clients receive a monthly home wealth report with both your name and the agent's name on it. The agent gets ongoing visibility in your client base, and you get ongoing presence in theirs. It's a tangible, recurring value exchange that a box of donuts genuinely cannot compete with.

- How to keep the relationship alive between referrals

The most common reason LO-agent relationships fade is simple: the LO disappears between referrals. There's a burst of energy around each closed deal and then silence until the next one. Agents notice. A consistent presence is what earns priority status over the other lenders in their phone. Here's a monthly system that keeps you visible without being annoying:

- Send a monthly market update. On the first of the month, send a short text or email specific to their price range and farm area. Two sentences. Useful information, not a newsletter.

- Build a one-pager for their listings. When one of their listings has assumable loan potential or seller concession opportunity, put together a financing breakdown and send it over. It takes 15 minutes and they remember it for months.

- Send a handwritten card after every referral closes. Not an email. A card. It takes three minutes and almost no one does it.

- Check in quarterly about their business. Ask what's working and what's slowing them down. Then think about whether anything you do could help with the second part.

Agent partnerships are your primary source of new purchase business. But the most overlooked source of loan volume isn't new at all. It's already sitting in your CRM.

Strategy 2: Past Client Re-Engagement Is Your Highest-ROI Mortgage Lead Nurturing Channel

The mortgage industry has specifically low borrower retention rates with only about 18-20% returning to their original lender for their next mortgage.

The reason comes down to a nurturing problem.

- Most borrowers say they’d happily use their lender again

- But only 13% can remember their loan officer's name a year after closing.

They didn't stop trusting you. They just forgot you existed. The fix isn't more follow-up hustle. It's a system that keeps you in front of them consistently, with something valuable enough that they actually want to open it.

- Segment your database so you know who to call first

Your CRM probably has everyone lumped together. That's why it feels overwhelming. Before you do anything else, segment your contacts into four tiers based on opportunity and urgency:

- Call your Tier 1 contacts this week

Not email. Call. A phone call from you, referencing their specific home and loan, is something most of your competitors will never do. It takes about three minutes and it immediately sets you apart. Here's a script that doesn't feel like a sales call:

- Put Tier 2 and Tier 3 on autopilot

You can't personally call 300 people every month. And you shouldn't have to. For Tier 2 and Tier 3 contacts, the goal is simple: stay visible and deliver enough value that they think of you when the moment comes.

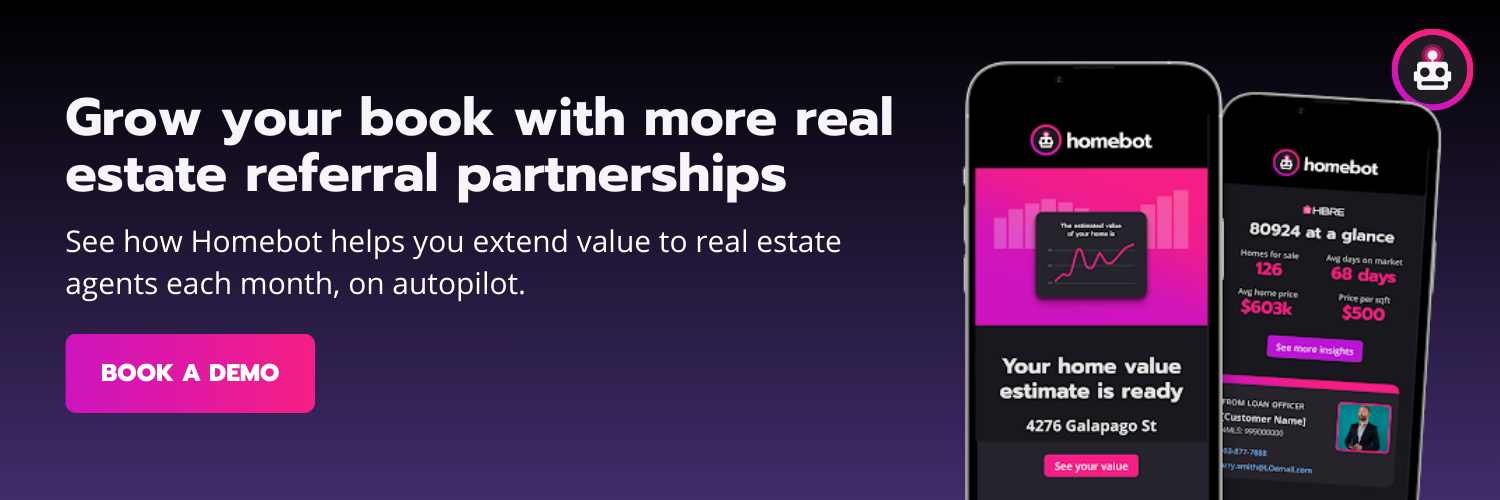

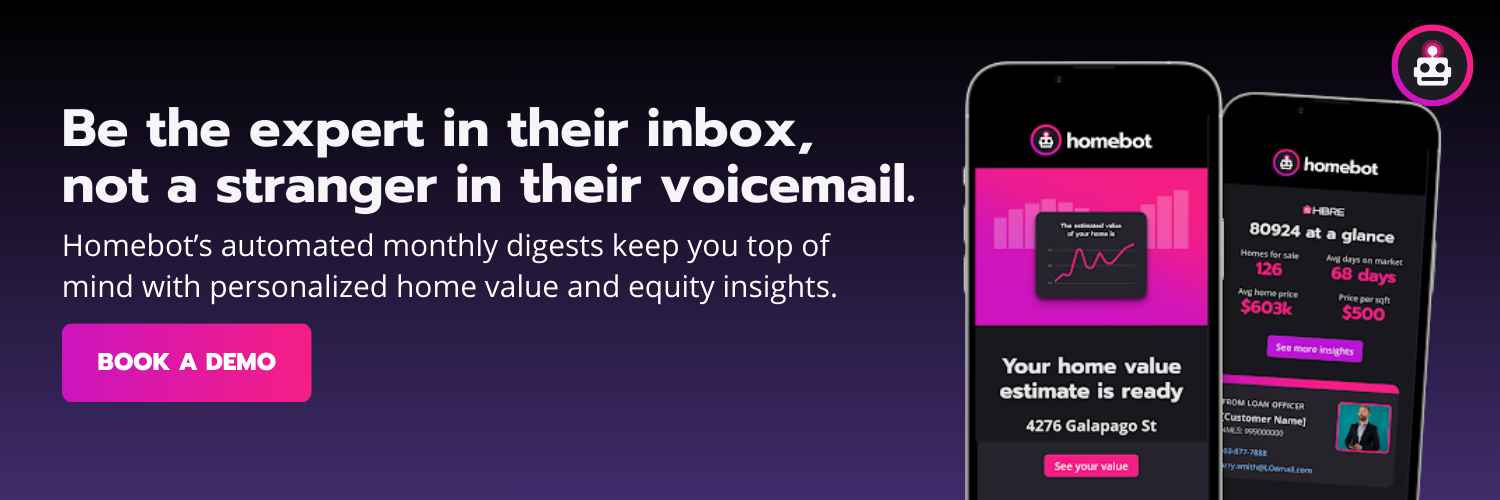

Homebot's Home Digest does that automatically. Each month, your past clients get a personalized report that shows:

- Their current estimated home value

- How much equity they've built

- What they could potentially do with it

All of it delivered under your name and branding. It achieves a 75% open rate because the content is specific to that person's home, not a generic market update blasted to everyone at once. Your name shows up in their inbox every month with something they actually want to read. That's what solves the 13-month memory problem.

- Let engagement signals tell you who's ready to move

The other thing that consistent monthly touchpoints give you is visibility into who's actively thinking about making a move, before they call you.

When you know what your contacts are doing, you can reach out at exactly the right moment instead of guessing. A few signals worth acting on immediately:

- Repeated clicks on home value content. A client who clicks the home value section of their monthly report three months in a row is thinking about something. That's worth a call.

- Sudden browsing activity after a long silence. A client who starts exploring home search listings after two years of inactivity is probably looking at a move-up. Get ahead of it.

- A listing alert on a past client's home. When a client's home appears on the MLS, they're in motion right now. Homebot's listing alerts notify you the moment that happens so you can be the first call about their next purchase loan.

That kind of proactive outreach is what separates LOs who grow during slow markets from LOs who wait for the phone to ring.

- What a 150-client database is actually worth

If the math on past client re-engagement still feels abstract, here's a concrete way to look at it. Run these numbers against your own database size:

That's the revenue sitting in a modest database before you've made a single cold call or spent a dollar on lead generation. It just requires a system to surface it.

Use the Calculator to Determine What Your Database is Worth

Agent partnerships bring you new borrowers. Your existing database brings you back the ones who already chose you once. Both channels grow over time. The third thing that ties them together is visibility, and that's where your personal brand comes in.

Strategy 3: Build a Loan Officer Personal Brand That Makes Your Name Familiar Before the Referral

Here's a scenario most loan officers have experienced:

- An agent refers a borrower to you

- You call, and they're lukewarm

- They've never heard of you and they're not sure why they should trust a stranger with one of the biggest financial decisions of their life

The warm referral is actually a cold introduction.

A personal brand changes that dynamic. When someone in your market has seen your content for six months, they already know who you are by the time you call. The introduction becomes a reunion.

That compounds in ways no single tactic does. Content marketing generates 3x more leads than outbound marketing and costs a fraction of the price per lead over time. The investment is your time, not your marketing budget.

- What to post (specific examples, not vague advice)

You don't need a production team or a social media strategy doc. You need something true, useful, and specific to your market. These five content types work well for loan officers and require nothing more than a phone and something worth saying:

- The "one loan = five pieces of content" system

You close loans every month. Each one of those closings is a content asset waiting to be used. Here's how to turn a single deal into a week's worth of content without spending more than 30 minutes on it:

- LinkedIn post: "Closed this one for a first-time buyer who thought they needed $80K down. We got it done with $14K. Here's what made the difference." (Anonymize the details. Keep the numbers.)

- 60-second phone video: Walk through the loan structure out loud, the same way you'd explain it to a client. Film it on your phone. No editing needed.

- Email to your database: "Quick note on something I've been doing for buyers dealing with tight down payments lately." Three paragraphs. Link to the video.

- Instagram or Facebook story: Same deal, distilled to one sentence and one number. "Helped a buyer get into a $480K home with $14K down this week. DM me if you want to know how."

- Agent outreach: "I just closed something interesting in your farm area. Worth a coffee to walk through it?" Now you have a reason to reach back out to an agent you've been meaning to follow up with.

Neel Dhingra built a significant loan pipeline through exactly this approach: real deal examples, educational content, and consistent posting that made his name familiar long before borrowers needed a lender. Get his 2026 content strategy for lenders here.

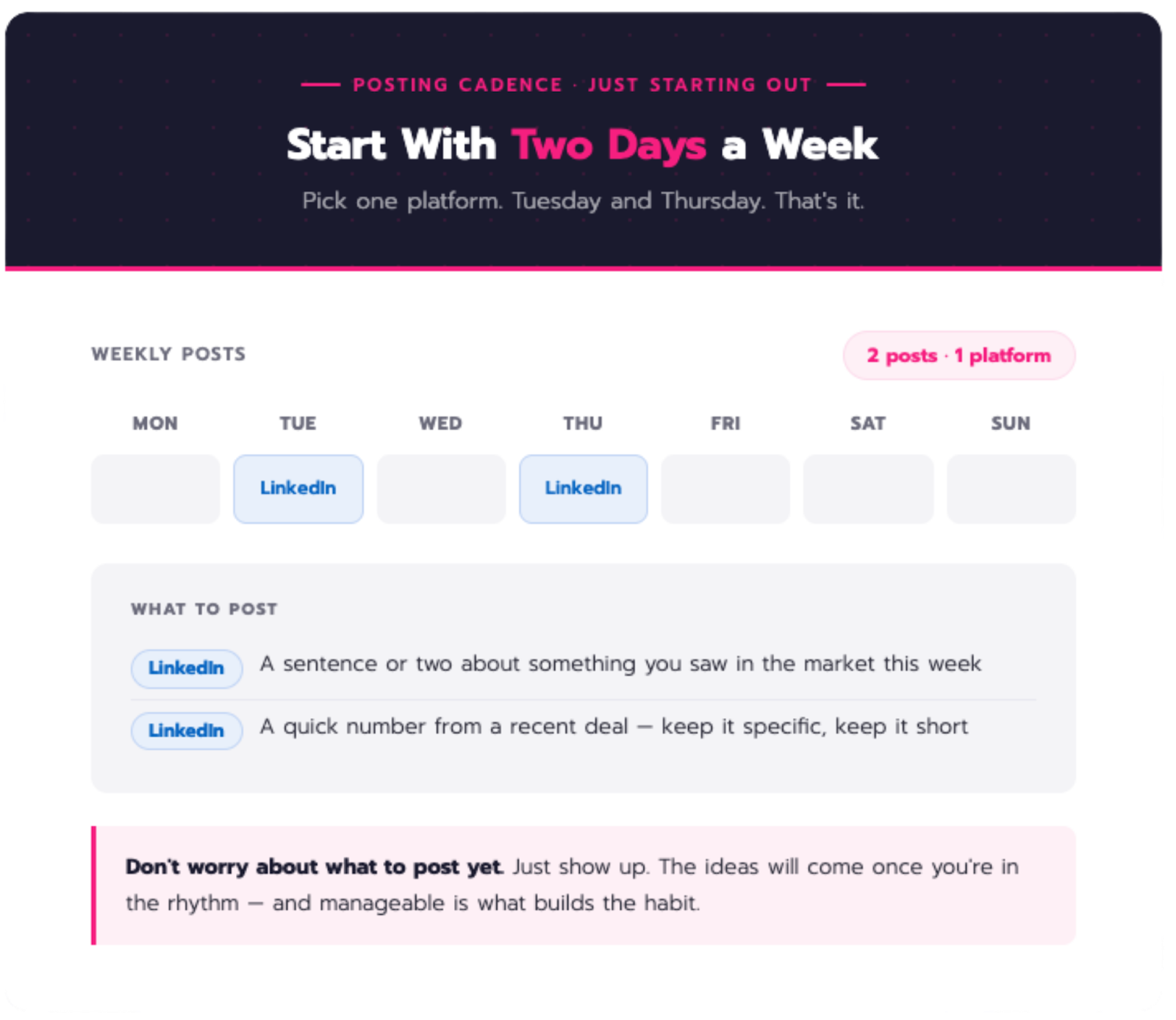

3. A posting cadence you can actually maintain

The most common mistake with personal brand building is trying to do everything at once and burning out by week three. Content is like going to the gym. You don't start by lifting the heaviest weight in the room. You build the habit first, then increase the load as it gets easier.

If you're just starting out:

Pick one platform. Post on Tuesday and Thursday. That's it. Two posts a week feels manageable, and manageable is what builds the habit. Don't worry about what to post yet. Just show up. The ideas will come once you're in the rhythm.

- LinkedIn: A sentence or two about something you saw in the market this week

- Instagram or Facebook: A quick video or a number from a recent deal

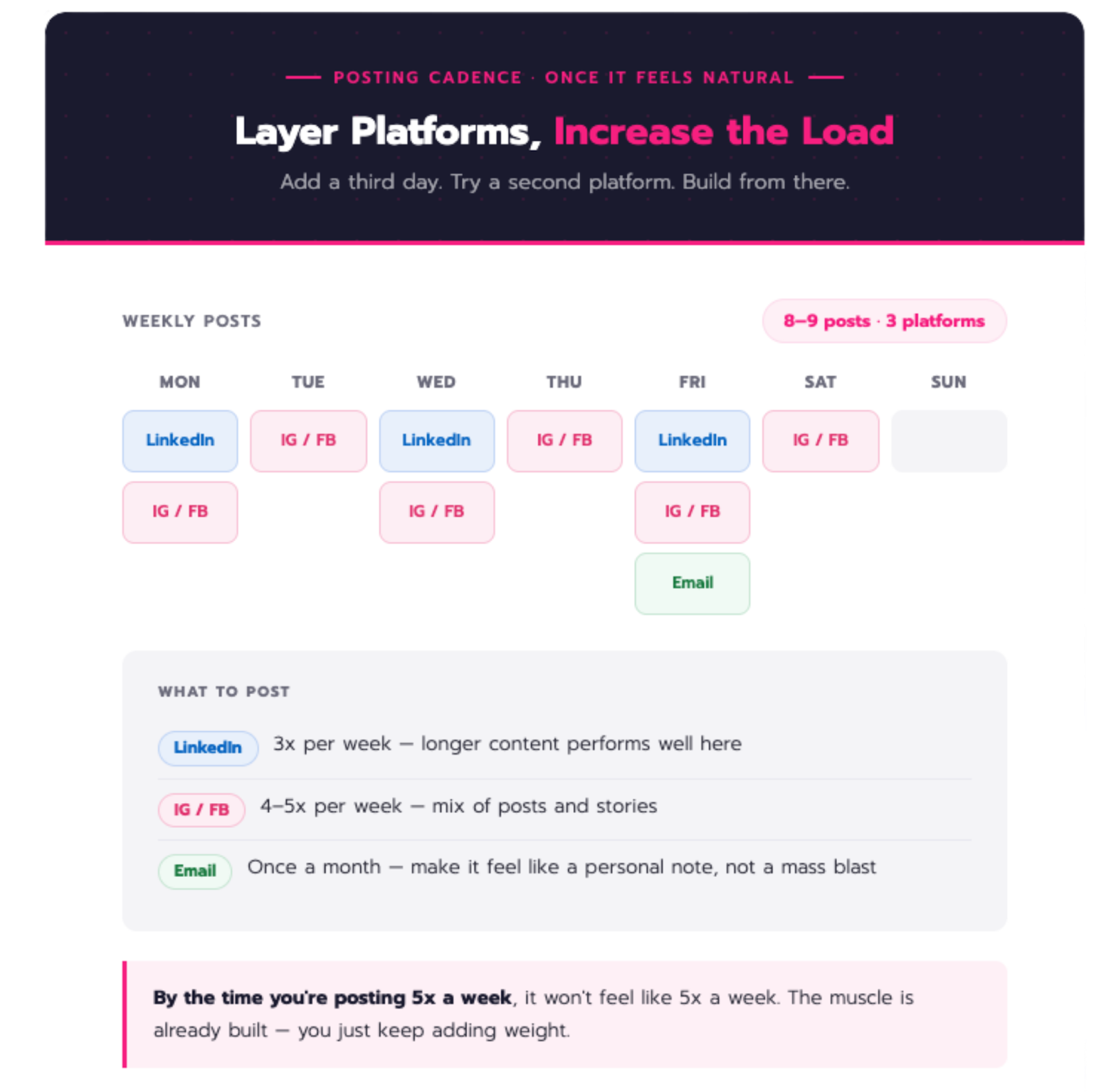

Once posting feels natural:

Start layering. Add a third day. Try a second platform. Increase your frequency gradually, the same way you'd add weight at the gym. By the time you're posting five times a week, it won't feel like five times a week because the muscle is already built.

- LinkedIn: 3 times per week. Longer content performs well here.

- Instagram or Facebook: 4 to 5 times per week. Mix of posts and stories.

- Email to your database: Once a month. Make it feel like a personal note, not a mass blast.

A visible personal brand makes your agent partnerships stronger, your past client referrals more likely to convert, and your name familiar in conversations you were never part of. It's also the bridge to the referral sources in the next section that most loan officers overlook entirely.

Strategy 4: Non-Agent Referral Sources That Most LOs Leave Untouched

Agent partnerships are your primary pipeline. But if one agent pulls back or switches to another lender, you feel it immediately. Non-agent referral sources diversify that risk and often come with almost no competition, because most LOs never think to pursue them.

These sources take longer to develop than agent relationships, but they tend to be stickier once they're established. A CPA who trusts you will send clients for years. An HR department that puts your name in their onboarding packet creates a recurring stream of relocating buyers without ongoing effort on your part. Here's how to build each one.

- CPAs and tax professionals

CPAs are in their clients' financial lives constantly. When a client asks about buying a home, refinancing to access equity, or using home equity to fund a business investment, the CPA is often the first call. Most CPAs don't have a go-to lender. They're happy to make a referral when someone they trust asks for one. You just have to be that person first.

- Divorce and estate attorneys

Divorce proceedings frequently require one party to refinance the other off the mortgage. Estate settlements often involve property buyouts among heirs or the sale of a family home requiring bridge financing. Both situations need a loan officer who can move quickly, communicate clearly under pressure, and navigate time-sensitive transactions. Attorneys refer these cases to LOs they know and trust personally.

- Find local divorce and estate attorneys through your state's bar association directory

- Lead with a specific value proposition when you reach out: "I specialize in time-sensitive mortgage situations and have closed [X] divorce refinances in the past year. I know how to keep the transaction moving even when the underlying situation is complicated."

- Offer a no-commitment consultation for any case they're working on where mortgage questions come up. Getting on the phone once and being helpful is usually enough to get the first referral

- HR departments and employee benefits teams

Companies that are actively hiring or relocating employees are a direct and often ignored pipeline to purchase borrowers. HR teams genuinely want to help incoming employees navigate the homebuying process in a new city, and most of them have no one to send those employees to. Getting your name into an employer's onboarding materials is a recurring source of warm referrals that requires almost no ongoing work once the relationship is established.

- Find companies actively hiring by checking LinkedIn Jobs or your local business journal's growth company lists

- Offer a free "mortgage basics for relocating buyers" lunch-and-learn for the HR team or a small group of new employees. Forty-five minutes, no selling, purely educational. It gets you in the room and builds immediate credibility.

- Follow up with a simple one-pager HR can add to their onboarding materials: "Buying a home in [City]? Here's who to call." Your name, your number, one clear offer of help.

- Niche positioning accelerates all of these

Having a clear niche makes every non-agent referral partnership easier to build. When you're known for something specific, referral sources know exactly when to call you.

A few examples of how that plays out:

- VA loan specialist: The veteran-focused financial planner knows exactly why to send their clients to you

- Self-employed borrowers: The CPA who works with small business owners has an obvious reason to pick up the phone

- Divorce refinances: The family law attorney knows you can handle time-sensitive, complicated transactions

The right niche is wherever your existing experience overlaps with real demand and limited competition. Some options worth considering:

- VA loans

- First-time buyer DPA programs

- Jumbo borrowers

- Real estate investors

- Self-employed documentation cases

- Divorce refinances

Pick one. Build visible expertise in it. Every referral conversation gets easier from there.

Now that you have the four strategies, the question is how to sequence them so you're building momentum without trying to do everything at once.

Your 90-Day Action Plan to Increase Loan Volume

The LOs who successfully shift away from purchased leads don't try to rebuild everything overnight. They work in phases, layering one system on top of another until the whole thing runs with minimal manual effort. Here's the sequence that gets you there in 90 days.

Weeks 1–3: Get the foundation in place

- Segment your database into the four tiers from Strategy 2. This is the most important thing you can do in week one. Everything else builds on knowing who's in your database and what they need.

- Call every Tier 1 contact personally. Use the script above. This is your fastest path to closed loans from work you've already done.

- Activate automated monthly touchpoints for Tier 2 and Tier 3 contacts so they stay warm while you focus on higher-priority outreach.

- Build your agent outreach list. Use MLS data or Partner Intel to identify 10 target agents who match the profile from Strategy 1.

- Send Email 1 to all 10 agents. Get the sequence started.

Weeks 4–8: Build the referral engine

- Follow through on the 3-touch agent sequence. Aim to have 3 to 5 coffee meetings on the calendar by the end of week 8.

- At each meeting, show up with something concrete: a co-branded tool, a financing breakdown for one of their listings, or an offer to co-sponsor their past clients. Don't just talk about what you can do. Demonstrate it.

- Pick your content platform and post 3 times per week. One idea per post. Don't let perfect be the enemy of consistent.

- Identify 2 to 3 CPA or attorney referral targets in your market. Send the outreach email.

- Set up listing alerts for your entire database so you know the moment a past client puts their home on the market.

Weeks 9–12: Let the system compound

- Send a monthly check-in to each active agent partner. One sentence with a market data point specific to their farm area. It takes five minutes and keeps you top of mind between referrals.

- Review your engagement data. Which past clients are opening monthly updates, clicking through, or showing browsing behavior? Prioritize those contacts for personal outreach before they call someone else.

- Evaluate your content. Which posts got the most engagement, saves, or DMs? Do more of that format. Drop whatever isn't getting traction and don't look back.

- By week 12, you should have 3 to 5 active agent relationships generating referral conversations, at least 2 non-agent referral sources in early development, and a database that's working for you every month without manual effort.

How to Measure Increased Loan Volume Without Buying Leads

Relationship-based pipelines take longer to show results than lead purchases, which makes it easy to lose confidence before the system fully kicks in. Tracking the right metrics each month keeps you grounded in whether you're making progress, even when the closed loans haven't caught up yet.

Final Note: The Way to Increase Loan Volume Is Already in Front of You

The loan officers growing their volume right now aren't outspending the market. They've built a system. Their past clients hear from them every month. Their agent partners send referrals because the relationship runs both ways. Their name is familiar to borrowers they haven't even met yet.

None of that requires a bigger budget or a different market. It requires the four strategies in this guide and the discipline to work them over the next 90 days.

Homebot helps loan officers put this into practice by automating the monthly touchpoints that keep past clients engaged, surfacing behavioral signals that show who's ready to make a move, and giving you co-sponsorship tools that make agent partnerships more valuable for both sides. If you want to see what that looks like for your specific database and market:

Try Homebot for yourself today.