Industry Hot Takes

RIP Trigger Leads: Here's What Comes Next for Loan Officers

TL;DR

- What this blog covers: How the trigger leads ban impacts the mortgage industry and the shift toward intent signal leads.

Why it matters: Trigger leads overwhelm borrowers, weaken trust, and perform poorly. Not to mention they’re extremely expensive. Intent signals produce higher ROI and stronger relationships.

What you’ll identify: The weaknesses in traditional lead generation and how behavioral insights can help loan officers stay ahead.

What’s included: Legislative details, strategic alternatives, and a smarter way to grow your pipeline.

Who it’s for: Mortgage professionals and lenders ready to replace outdated tactics with actionable engagement.

The way mortgage leads are bought and sold is about to change, forever.

With the signing of the Homebuyers Privacy Protection Act (H.R. 2808) into law, trigger leads—those credit-pull alerts that flood borrowers with unsolicited offers—are officially on their way out. Starting March 5, 2026, credit bureaus will no longer be allowed to sell these leads except under narrowly defined circumstances.

This is a defining moment for the mortgage industry. One that shifts the balance of power from mass marketing to meaningful engagement.

For loan officers, that means the tactics that used to work, like cold outreach, generic scripts, shared data, will soon lose their edge. The future belongs to those who lead with insight, not interruption.

If you're still relying on trigger leads, it's time to rethink the foundation of your prospecting strategy. Keep reading to unpack what’s changing, why the old model fell short, and how smart lenders are turning behavior into opportunity.

Why The Mortgage Trigger Lead Model Is Broken

Trigger leads were designed for speed. The moment a borrower applies for a mortgage and their credit is pulled, credit bureaus sell that information to subscribing lenders.

This sets off a flurry of activity:

- Dozens of lenders are alerted (at the exact same time)

- Borrowers are flooded with hungry lenders, often within hours

- Unsolicited mortgage offers start pouring in

For the buyer, it’s overwhelming. The volume of calls and messages creates confusion and stress. For the original lender, it’s a credibility hit, one they have no control over.

Instead of building trust, this experience creates friction at one of the most important points in the borrower’s journey.

The core problems behind trigger leads

It’s not just the borrower experience that’s broken. The entire trigger lead model is built on shaky ground, and it’s starting to show.

Here’s what makes trigger leads fundamentally flawed:

- Lack of insight: A credit pull tells you nothing about a borrower’s goals, timing, or financial situation.

- Shared access: Each lead is sold to multiple lenders, flooding the borrower with similar offers and diluting engagement.

- Low performance: Conversion rates hover around 2–3%, with acquisition costs ranging from $30 to $100 per lead (Internal Homebot analysis).

- Weakened relationships: Borrowers report growing frustration. In fact, the Mortgage Bankers Association notes that unsolicited offers are now one of the top complaints in the mortgage process.

Borrower dissatisfaction, weak ROI, and increasing regulatory pressure all point in the same direction: this system is no longer working. A smarter, more personalized approach is long overdue.

Breaking Down the Trigger Leads Ban: What’s Inside H.R. 2808

You might be wondering: What does the new law actually do?

In short, H.R. 2808 amends the Fair Credit Reporting Act to prohibit consumer reporting agencies from selling trigger leads, except in narrowly defined use cases. Industry and consumer advocates alike, ranging from the Mortgage Bankers Association to the National Consumer Law Center, have pushed for this protection.

According to America’s Credit Unions, the law’s primary aim is simple: protect consumers from predatory practices and restore control over their personal financial data.

What H.R. 2808 means for loan officers

The ban on trigger leads creates a critical shift in how loan officers generate and compete for originations. Without access to credit-triggered lead lists, the playing field changes in three key ways:

- Less inbound noise: Borrowers will no longer be overwhelmed by unsolicited offers after a mortgage inquiry. This gives you a clearer opportunity to build trust and deepen the relationship.

- No more reactive outreach: The old model relied on speed over substance. Lenders scrambled to connect with borrowers based on a credit pull, often too late and with little context. With trigger leads going away, you’ll need to shift from reactive marketing to proactive engagement, guided by real-time behavior and intent signals.

- Greater pressure to own your database: In this new landscape, your database is your most valuable asset. Winning means reaching clients before the market does, using behavioral data to understand their needs, personalizing your outreach, and deepening relationships that drive long-term value.

This law marks a turning point. And it favors the professionals who are ready to ditch noise for nuance, who engage early, deliver real value, and act on data, not assumptions.

Mortgage Lead Generation in a Post Trigger Lead World: Listing Alerts & Predictive Insights

Now that the Homebuyers Privacy Protection Act is law, loan officers are stepping into a new era of lead generation, one built on trust, privacy, and smarter engagement. This shift moves the industry away from mass outreach and toward strategies that prioritize intent and personalized connections.

Rather than relying on generic data points or cold outreach, the focus is shifting to behavioral signals that reveal true client intent:

- Listing views

- Equity checks

- CMA requests

- Affordability calculations

These actions are powerful indicators of a homeowner’s mindset, showing exactly when they’re starting to think about selling or refinancing.

Homebot’s lead generation features capture these signals and turn them into real opportunities. By surfacing high-intent activity from your own database, the platform helps you focus your energy on the right clients at the right time, so you can build relationships, not just chase leads.

Why Homebot’s listing alerts & predictive insights outperform:

Behavioral signals from Homebot unlock high-intent leads already in your database, helping you act sooner and more strategically. Here’s how Homebot gives you the edge, backed by data, built for performance, and tailored to your book of business:

- Accuracy: Homebot’s predictive insights draw on over 150 million rows of behavioral and demographic data to predict potential sellers with 89% accuracy in the top 50% of scores.

- Efficiency: Lenders using Homebot have seen up to 5x improvements in marketing performance by prioritizing highly engaged clients.

- Privacy-safe: Signals originate from clients engaging directly with your services and content.

- Exclusivity: Leads remain within your ecosystem, not shared with competitors.

Tools that prioritize high-intent engagement

Homebot’s platform features deliver behavioral visibility and intelligent prioritization:

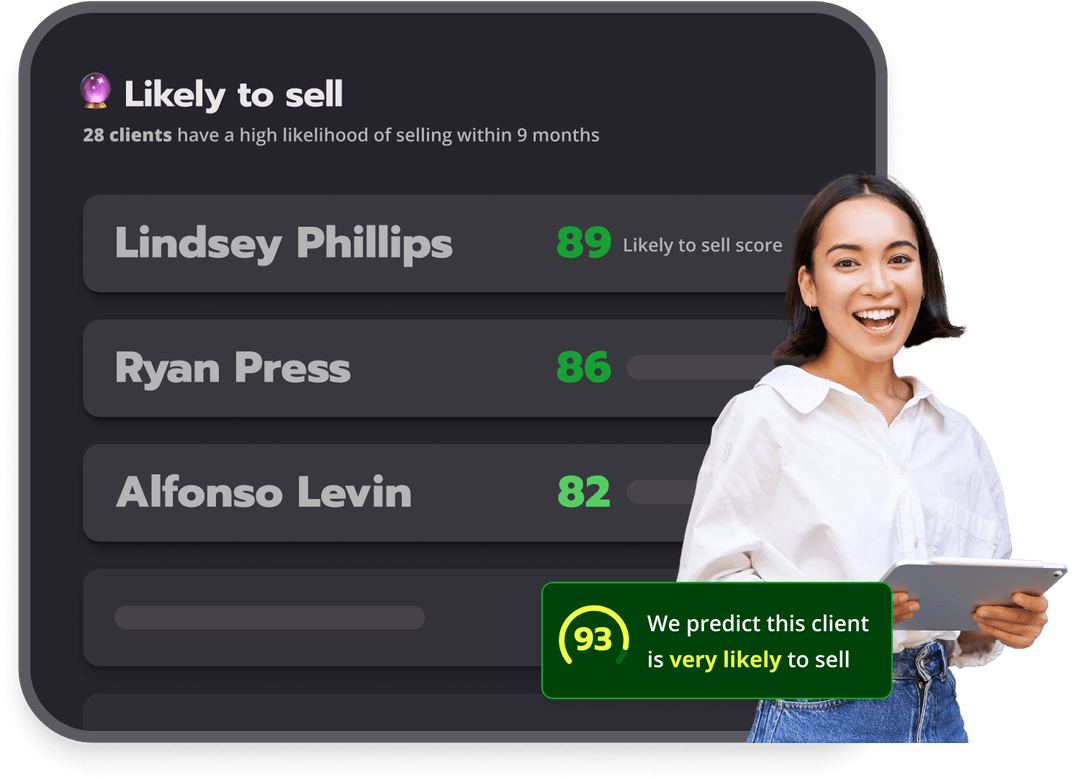

- Likelihood to Sell Score: This machine learning model analyzes equity, home tenure, listing activity, CMA requests, and more. It predicts which clients are most likely to sell within the next nine months.

- Deep Search Tracking: Homebot detects when users browse listings and measures the frequency of their activity. These signals highlight purchase intent with actionable clarity.

- Engagement Triggers: Loan officers receive timely alerts when users take meaningful steps, such as exploring affordability, checking equity, or re-engaging with Homebot content.

- Partner Intel: This feature aligns real estate agents and loan officers. Both parties can monitor shared client engagement, ensuring coordinated and timely outreach.

Conclusion: Lead With Data-Backed Intent, Not Overpriced, Over-Spammed Trigger Leads

The industry is at a turning point. With the Homebuyers Privacy Protection Act being signed into law, loan officers are stepping into a landscape that rewards strategy over speed. Generic outreach and shared data signals no longer deliver the trust, efficiency, or ROI today’s buyers expect.

Intent signals are the path forward. By leveraging behavioral data from your own database, you gain a smarter, privacy-first way to identify who’s ready to act. And how to engage them meaningfully. Homebot gives you the tools to turn signals into action, and action into closed loans.

Ready to replace low-yield leads with legit financing needs? Book a demo with Homebot.

Trigger Lead FAQs

What is the trigger leads Congress ban?

The proposed legislation, H.R. 2808 and S. 1467, restricts the sale of consumer credit data that triggers unsolicited mortgage marketing.

Why are trigger leads being banned?

They result in spam-like outreach, low conversion rates, and poor borrower experiences. Consumer and industry groups support the move.

What are intent signals?

Behavioral indicators—such as listing views, CMA requests, and affordability checks—that suggest a client is preparing to buy, sell, or refinance.

How does Homebot generate intent signals?

Homebot analyzes over 150 million rows of proprietary user engagement and demographic data to surface clients most likely to transact.

Are intent signals compliant?

Yes. They originate from direct client activity on your platform and do not rely on third-party credit data.