Loan Officers

The Problem with Trigger Leads: Why Listing Alerts Are More Valuable for Loan Officers

.png)

More leads sound great, until you’re buried in cold calls and ghosted by borrowers. When it comes to leads, more isn’t always better… especially if they’re trigger leads.

Trigger leads are sold by credit bureaus the moment a borrower applies for a mortgage. While they might seem like an easy way to find potential clients, they come with big downsides. Borrowers get bombarded by multiple lenders, conversion rates are low, trust is out the window, and intent is unclear. Just because someone applied for credit doesn’t mean they’re ready to move forward.

The fact is, trigger leads aren’t reliable. Even lawmakers are over them. With recent legislation making its way to the Senate, trigger leads could be seeing their last hoorah.

Top originating loan officers aren’t wasting resources on trigger leads. Instead, they’re leaning into more modern tools that surface real-time client behavior like listing alerts, home search activity, and affordability checks. These tools allow you to focus on real behaviors, like home searches, equity engagement, and affordability checks, so you know when a client is actually ready to buy, sell, or refinance.

If you’re tired of chasing cold, non-exclusive trigger leads, this is your playbook for success.

What Are Mortgage Trigger Leads?

To be a successful lender, timing is everything. The sooner you can identify serious buyers and sellers, the better your chances of building a connection and closing the deal. That’s why many loan officers turn to trigger leads in the first place. But how do they actually work, and are they as effective as they seem?

Here’s how mortgage trigger leads works:

- A borrower applies for a mortgage or pre-approval.

- Their credit inquiry is flagged as a trigger event by credit bureaus.

- Credit bureaus sell the borrower’s contact information to multiple lenders.

- Those lenders immediately flood the borrower with calls, emails, and texts, often creating a frustrating, spam-like experience.

In theory, it sounds like an easy way to connect with active borrowers. But in practice, trigger leads lack real intent, are highly competitive, and often leave loan officers chasing cold prospects. Instead of reaching motivated buyers or sellers, you're competing for attention in a crowded, impersonal race.

Why Mortgage Trigger Leads Are Dead

While trigger leads might seem like a quick way to find potential clients, they come with major downsides, from intense competition to low conversion rates. Let’s dive into why they often aren’t worth the investment.

1. They lack buyer or seller intent

A credit pull could mean they’re ready to move… or just curious after one too many late-night Zillow scrolls. Hard to say. Without context, you're reaching out blind, hoping to land a deal with someone who may not be ready to move forward.

2. They’re sold to multiple lenders

Trigger leads aren’t exclusive. Multiple lenders buy the same borrower’s information, flooding them with outreach. This creates a race to the bottom, where loan officers compete on speed and pricing rather than building real relationships. Many borrowers tune out the noise, leaving your outreach ignored.

3. Trigger leads have high cost and low ROI

How much do trigger leads cost? Trigger leads typically cost $30–$100 per lead, depending on borrower profile and exclusivity. But since multiple lenders are bidding for the same borrower, your cost per funded loan skyrockets.

Even worse, trigger leads often result in a high volume of low-quality leads. One study found that only about 2-3% of trigger leads actually convert into closed loans. That means for every 100 leads you purchase, you might only close two or three loans, while competing with dozens of other lenders for the same borrower’s attention.

Paying for the same lead as your competitors doesn’t just drive up marketing costs. It also lowers your conversion rate. Instead of investing in high-intent opportunities, you're fighting for attention in an oversaturated market.

4. A poor borrower experience = lower engagement

Getting hit with five calls, three emails, and a text before lunch? Not exactly the dream home buying experience.. Some report trigger leads as spam, making it even harder for loan officers to break through the noise. And perhaps most critically, this is a surefire way to damage trust before a single conversation can even happen.

5. They bring compliance & ethical concerns

Many borrowers aren’t aware their data is being sold, leading to trust issues. While trigger leads are legal under the Fair Credit Reporting Act (FCRA), their aggressive use has led to growing industry pushback. Some states have even introduced legislation to restrict or ban them.

Why First-Party Engagement Like Listing Alerts Are a Better Alternative to Trigger Leads

If trigger leads leave loan officers chasing low-quality, high-competition prospects, what’s the better approach? Mortgage intent signals.

Client engagement behaviors like listing alerts, home searches, or equity activity, indicate when someone’s preparing to buy or sell a home. Listing alerts are a perfect example. When a client consistently views homes or saves properties, it signals real readiness, without needing to buy third-party data. These engagement triggers tell you who’s serious, right from your own database.

Rather than chasing cold leads, tracking these signals means you’re engaging with clients at the moment they’re most receptive… when they’re actively exploring their options. Here’s how third-party trigger leads stack up against first-party client engagement insights:

1. Intent signals show real interest in buying or selling

A credit inquiry alone doesn’t confirm if a borrower is actively looking for a home or refinancing with intent. Mortgage intent signals, on the other hand, track actions that indicate a borrower is getting ready to make a move.

Here are some high-value signals that suggest real intent:

- Home search activity – Clients repeatedly viewing listings in a specific price range or location.

- Equity engagement – Homeowners checking their home value or exploring cash-out refinance options.

- Affordability calculations – Borrowers testing mortgage calculators or adjusting loan scenarios.

- CMA (Comparative Market Analysis) requests – Homeowners evaluating whether it’s time to sell.

Each of these actions tells you why a borrower is engaging… not just that they had their credit pulled.

2. First-party leads are exclusive to you

Unlike trigger leads, which are sold to multiple lenders, intent signal leads are based on your own client database and your exclusive engagement data. This means:

- No competing with multiple lenders for the same borrower.

- No cold outreach. Just warm, data-backed conversations.

- Higher response rates and stronger client relationships.

3. Higher conversion rates & better client relationships

When you reach out to a client based on their actual home search behavior, equity engagement, or mortgage planning, you’re speaking to them at the right moment… not bombarding them with an unsolicited pitch.

This results in:

- More meaningful conversations.

- Higher engagement rates.

- Stronger trust and long-term client loyalty.

4. Lower cost, higher ROI

Because first-party leads focus on high-quality, high-conversion opportunities, loan officers using them see:

- Lower cost per funded loan.

- Less time wasted on cold leads.

- More closed deals with less effort.

Rather than competing in a crowded space with expensive, low-converting leads, listing alerts and other engagement signals allow you to prioritize the right clients and maximize ROI.

How To Start Leveraging Listing Alerts and Behavioral Insights with Homebot

Your database is powerful, but only if you have the right tools to track and act on it. Homebot surfaces these high-value insights in real time, helping loan officers engage with the right clients at the right time.

Homebot’s Predictive and Behavioral Insight Features

Homebot provides exclusive, data-driven predictive insights that help loan officers prioritize high-intent clients and increase conversions based on their actions within the platform. Here’s how it works:

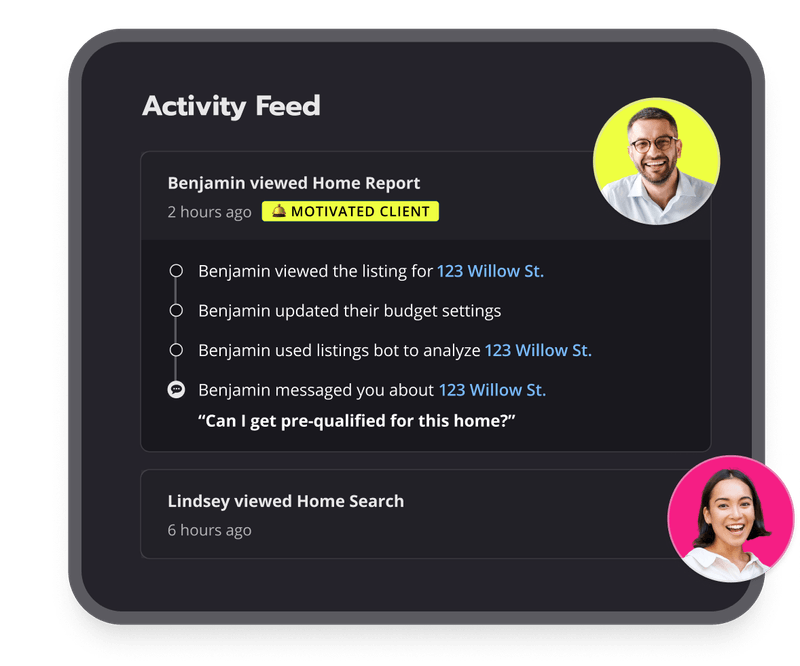

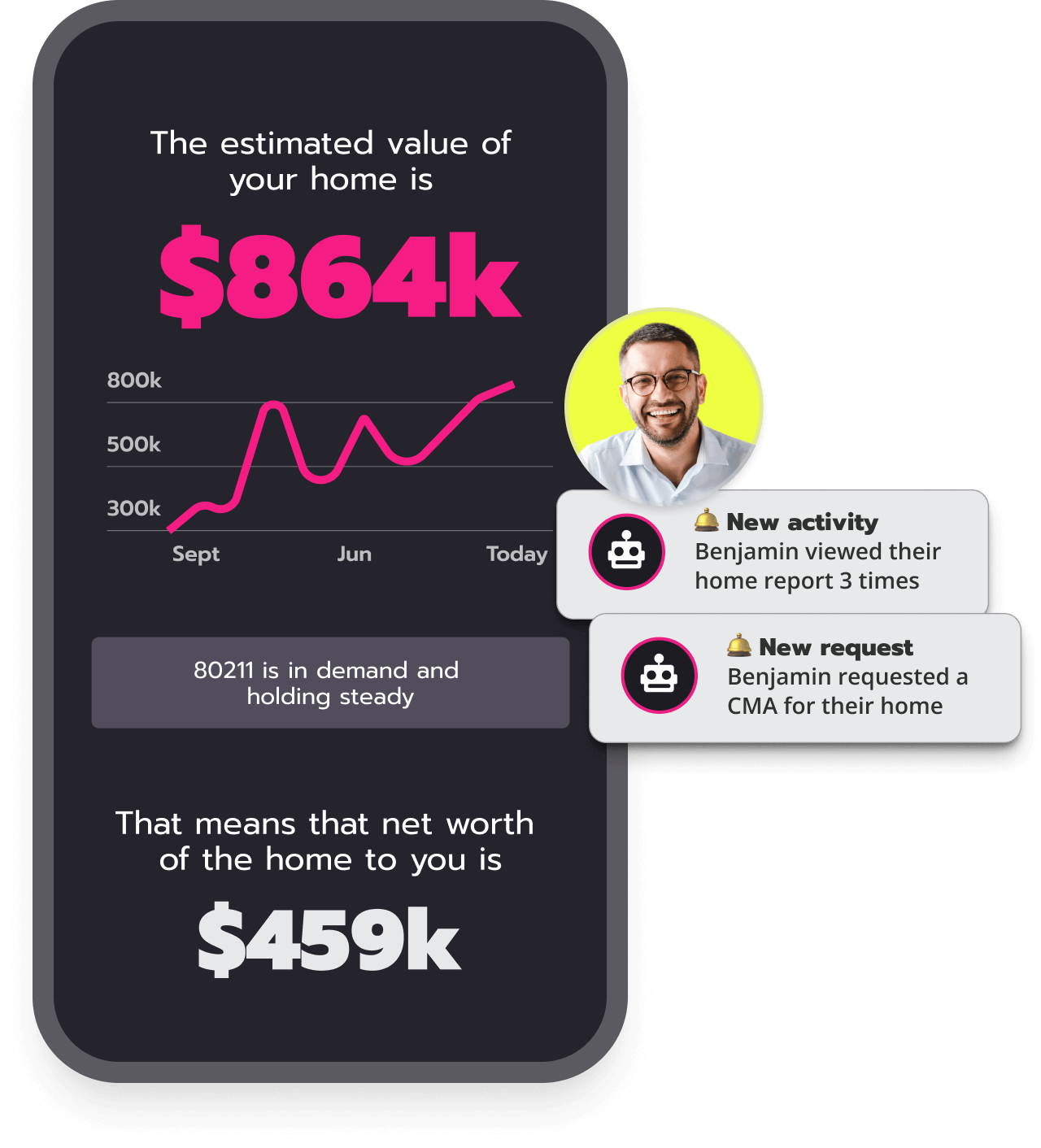

- Deep Search tracking

Through Deep Search, you can see exactly which properties a client is viewing, how often they return to certain listings, and what price ranges they’re considering. This allows loan officers to proactively discuss financing options before a client reaches out to a competitor.

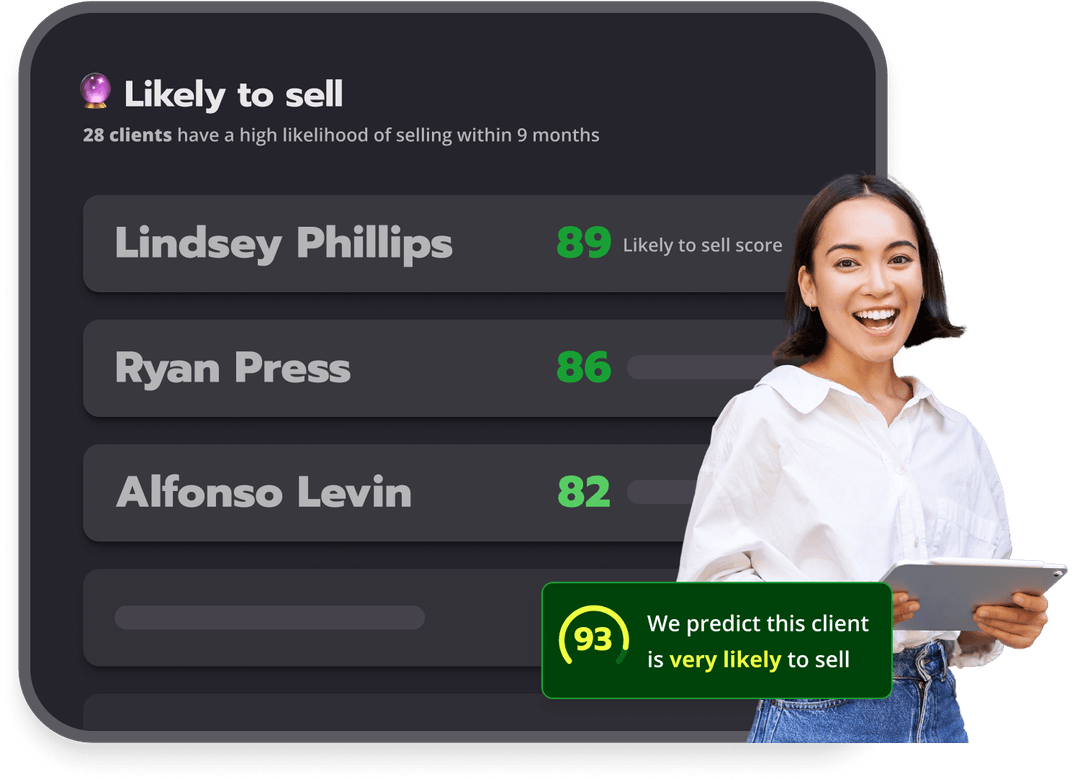

- Likelihood to Sell Score

The Likelihood to Sell Score feature uses machine learning to predict which homeowners are most likely to list their home within the next nine months with 89% accuracy. By identifying likely sellers early, loan officers can engage them before they start shopping for financing elsewhere.

- Engagement insights

Track client activity across home equity research, affordability calculations, and refinance exploration with Homebot’s AI-driven engagement insights. These signals indicate who’s actively preparing for a financial decision so loan officers can reach out with relevant options.

- Personalized outreach tools

Leveraging Homebot’s mortgage automation features, you can conduct follow-ups based on client behavior, ensuring that loan officers engage with borrowers at the perfect moment… when they’re most likely to convert.

Conclusion: Ditch Trigger Leads. Use Real Client Behavior to Close More Loans

Trigger leads may seem like an easy way to find borrowers, but mortgage intent signals are the smarter alternative if you want to see ROI and long-term, repeat clients. By tracking real behaviors, loan officers can identify high-intent clients before their competition, personalize their outreach, and close more deals with less effort.

Homebot makes this process effortless by providing real-time insights into client behavior, predictive analytics, and automated engagement tools, all designed to help you focus on warm, exclusive leads that actually convert.

Ready to connect with serious buyers and sellers before anyone else? Book a demo today.