Marketing Strategy

What Is a Home Report? Comparing the Top Platforms for Loan Officers and Real Estate Agents

A homeowner checks their home's value for a few core reasons:

- They're thinking about buying

- They're thinking about selling

- They want to tap their equity for funds

As a lender or realtor, these are the moments you want to know about, ideally before the client googles "how much is my house worth" or starts scrolling Zillow.

That’s the value of an automated home report. A home report puts the data in their hands first: their current value, the equity they've built, what's selling near them, and what they could do with that equity, all branded to you. The homeowner gets useful information. And you stay in front of them at the exact moment they're starting to consider a move.

So if you’re a lender or realtor looking for an automated way to stay in front of your database, you’ve come to the right place. This post breaks down what a home report is, which mortgage and real estate marketing tools offer it, and how industry pros are using these tools to turn their database into life long repeat clients.

What Is a Home Report?

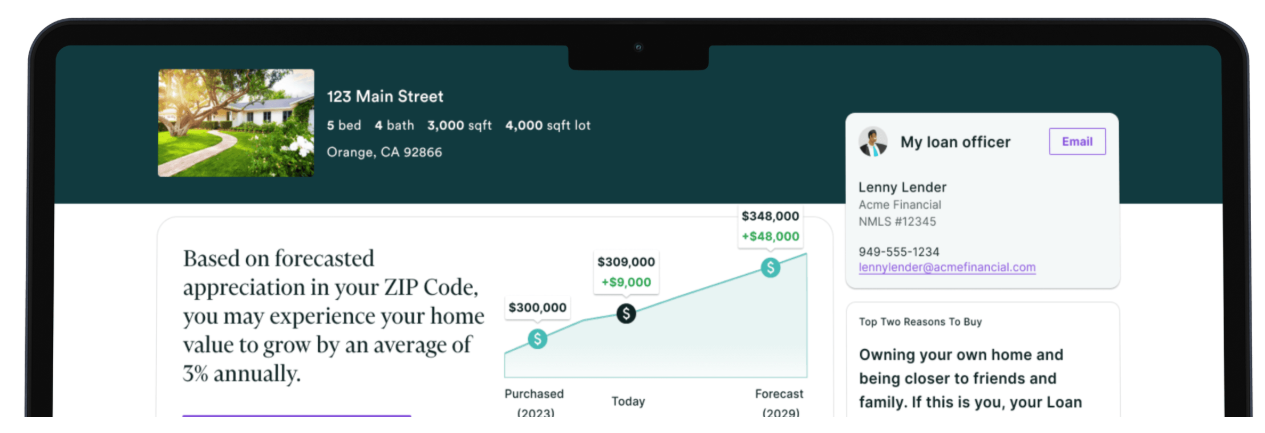

A home report is a personalized monthly summary sent directly to a homeowner. It shows them what their specific property is worth right now, how much equity they've built, what's happening in their local market, and what financial moves they might consider. It's branded to the loan officer or real estate agent who sent it.

A home report is not to be confused with a generic market newsletter. A newsletter tells a homeowner what the Phoenix metro is doing. A home report tells them what their home at 4821 West Chandler Blvd is worth today, how that compares to last month, and whether the equity they've built since they bought it opens up any interesting options.

At a glance, a home report typically includes:

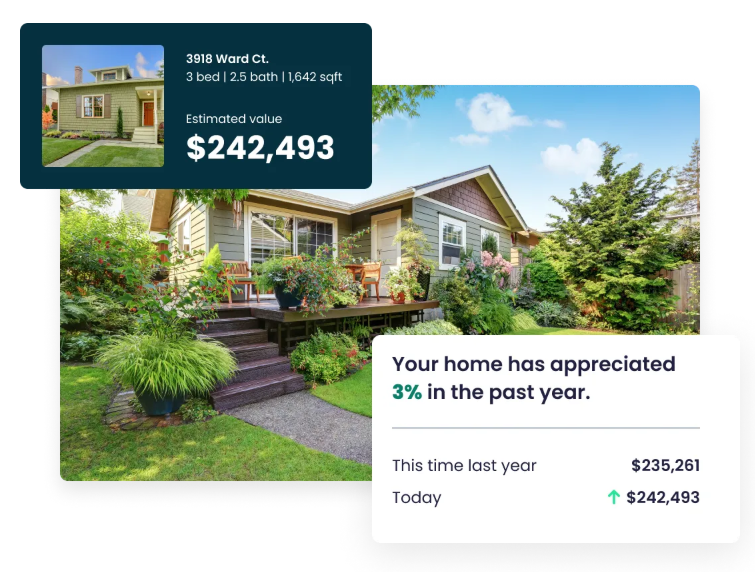

- Current home value based on automated valuation models (AVMs)

- Equity tracking month over month, in both dollars and percentage

- Local market context for the homeowner's specific neighborhood

- Personalized financial scenarios such as refinance, cash-out, or move-up calculations

- The professional's branding on every module, every month

Homebot calls its version the Homeowner’s Digest, a monthly branded email delivered to every client in a professional's database, automatically. The Homeowner's Digest is the engagement layer for loan officers and real estate agents who want to turn ongoing engagement into repeat clients without manual outreach at scale.

The category term "home report" is becoming a standard way loan officers, real estate agents, and homeowners search for this type of tool. Different platforms include different modules, pull from different data sources, and operate on different professional workflows. We'll get into the details below.

What's Inside Homebot's Homeowner's Digest

The Homeowner's Digest is an interactive platform covering different aspects of a homeowner's financial picture. Below is what each section shows the homeowner, and what it surfaces for the loan officer or real estate agent on the other side.

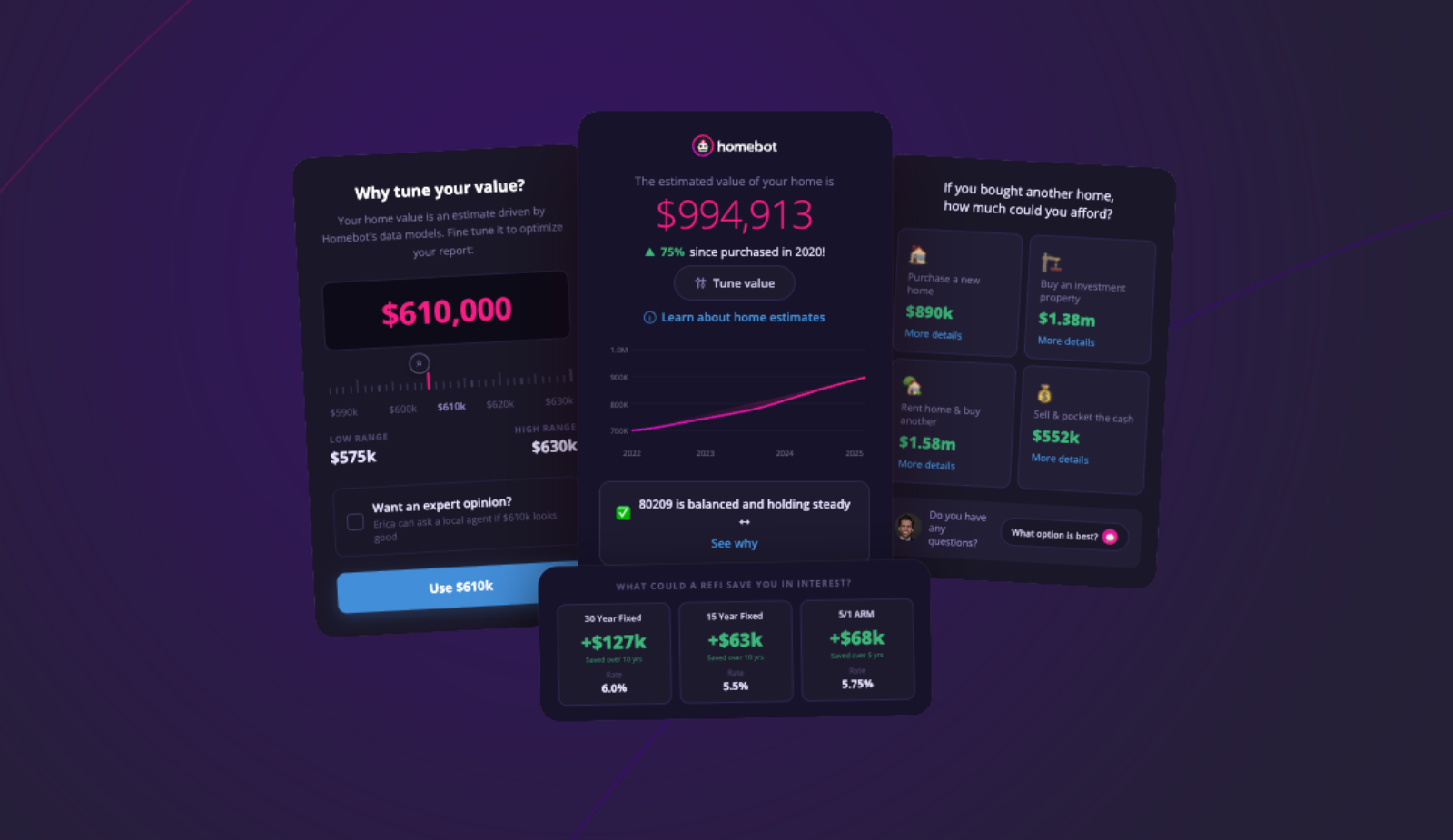

1. Home Value and Market Snapshot

What the homeowner sees:

- Current estimated property value, pulled from automated valuation models (AVMs) and updated monthly

- Tune Value, where they can submit comps or appraisal data to refine the estimate if they think it's off

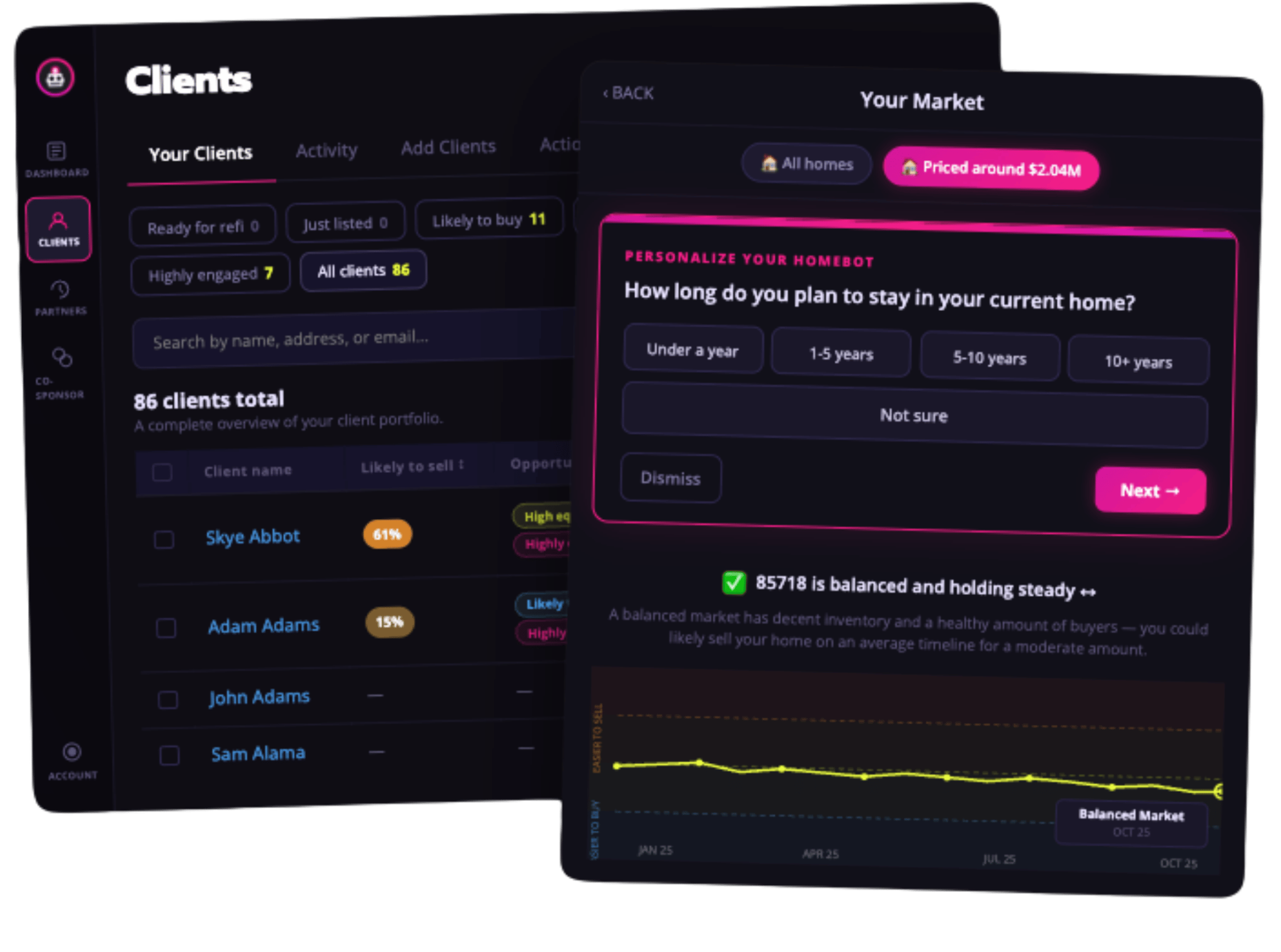

- Market Temperature, showing whether their neighborhood is currently a buyer's market, seller's market, or neutral

What it means for loan officers and real estate agents:

- Real-time activity in your feed when a homeowner adjusts their value or engages with the market temperature section

- A client checking market conditions is often the first behavioral signal that they're thinking about moving, before they've said a word to you

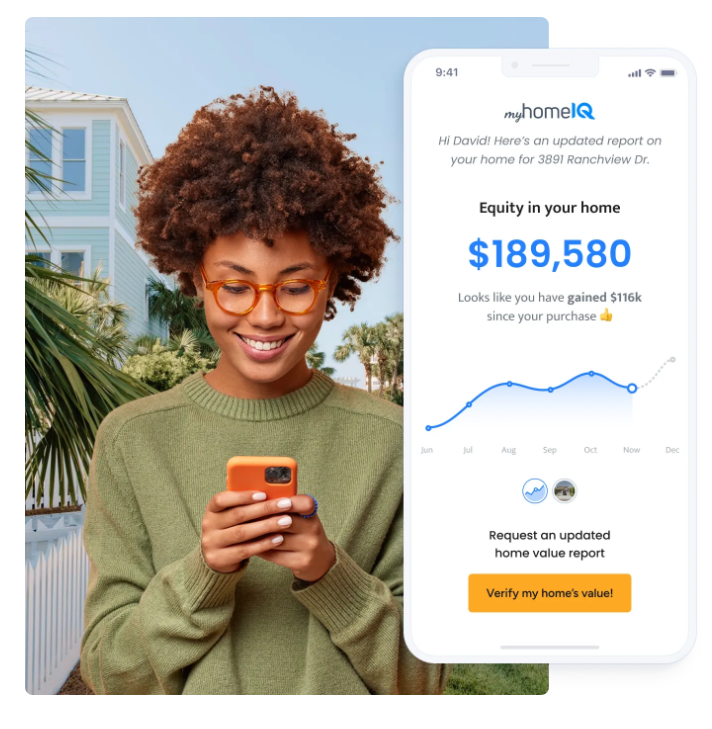

2. Equity Tracker

What the homeowner sees:

- Estimated equity built since purchase, expressed in both dollar amount and percentage

- Month-over-month equity changes alongside the home value estimate

- A tangible way to watch their net worth grow (or shift) without opening a financial app

What it means for loan officers and real estate agents:

Equity gains are one of the clearest signals for opening a refinance, cash-out, or move-up conversation. The average mortgage-holding homeowner currently sits on roughly $302,000 in equity, with about $195,000 of that tappable. A client who can see they've accumulated $180,000 in equity since they bought four years ago is generally already evaluating their options. The digest puts the data in their hands and frequently leads them to initiate the conversation directly.

For real estate agents, this same number is the entry point for listing conversations. Pew Research found that home equity accounts for a median of 45% of homeowner net worth, which means a client looking at their equity number is looking at nearly half of what they're worth.

3. Refinance Scenarios

What the homeowner sees:

- A personalized refinance scenario surfaced when rates shift or equity crosses a threshold

- Estimated monthly savings and break-even analysis

- A side-by-side view of the current and proposed payment, based on their actual loan details

What it means for loan officers:

- A primary mechanism for retaining refinance business that would otherwise migrate to a competitor when rates move. Rather than waiting for a client to search for refinance rates and end up on a competitor's landing page, the Homeowner's Digest puts the calculation in front of them every month, branded to their loan officer.

- Clients who see the math work in their favor typically reach out directly to the professional whose name is on the digest.

4. Purchasing Power and Equity Explorer

What the homeowner sees:

- Purchasing Power: whether their current equity could support buying another home, helpful for clients thinking about upgrading, downsizing, or investing in real estate

- Equity Explorer: specific scenarios walking through a cash-out refinance, a move-up purchase, or an investment property

What it means for loan officers and real estate agents:

- This section is one of the most common origination points for move-up transactions inside the Homebot platform. A client who can see they qualify for a $650,000 home based on their current equity position is generally already in motion. The professional's role is to guide the next step.

- Real estate agents featured in the Homebot Network appear directly in this section, so when a homeowner starts exploring purchasing power, the agent of record is right there.

5. Short-Term Rental Potential

What the homeowner sees:

- An estimate of how much they could earn by renting their home, or a portion of it, on platforms like Airbnb

- A property-specific projection that pulls platform data and applies it to their home

What it means for loan officers and real estate agents:

- Surfaces clients who may be sitting on rental income potential they've never considered

- Opens conversations about DSCR loans, investment properties, and wealth-building strategies that go beyond the simple buy-and-hold narrative

6. W.I.N. (What's Important Now)

What the homeowner sees:

- A personalized lead section that highlights the single most relevant insight for that homeowner at that moment

- If rates have moved to create a refi opportunity, W.I.N. surfaces it. If equity has crossed a milestone, that's what leads.

- Personalized at the individual level, not the zip code level

What it means for loan officers:

- Higher engagement on the most actionable part of the report

- Stronger intent signals because clients are interacting with the sections most likely to predict their next move

7. Homeowner Check-In

What the homeowner sees:

- Periodic short check-in prompts: Are you planning to move in the next year? Are you thinking about a refinance?

- Low-pressure questions answerable in a few clicks

What it means for loan officers and real estate agents:

- Explicit intent data, not inferred behavior. When a client says they're planning to move within 12 months, they're automatically added to your Moving Soon list inside Homebot.

You don't have to guess who to call. Homebot tells you. The Homeowner Check-In paired with Opportunity Lists lets you know exactly who to reach out to when it makes the most sense.

8. Co-Branding for Both the Loan Officer and Real Estate Agent

For loan officers:

- Every module in the Homeowner's Digest is branded to you: name, photo, and contact information

- The homeowner associates all of this value with you specifically, so when they have a financial question, you're the person they think of

For real estate agents:

Through the Homebot Network, real estate agents are featured automatically in their clients' monthly Homeowner's Digests, in the exact sections where homeowners are making real estate decisions:

- The "Should You Sell" module

- The "Tune Your Value" section

- The Purchasing Power calculator

Agents appear in each of these touchpoints without paying a subscription fee. When a homeowner has a question about selling or listing, the request routes directly to the agent. The same model strengthens loan officer and real estate agent partnerships by giving both sides a shared monthly touchpoint with mutual clients.

This co-branded model benefits both professionals. Loan officers strengthen their agent partnerships by giving agents a monthly touchpoint with shared clients. Agents get visibility inside a high-engagement platform without the overhead. And homeowners get a unified advisory team instead of a collection of people they saw once at closing.

How Home Reports Compare: Homebot Homeowner’s Digest vs. Alternatives

Homebot isn't the only platform in this space. Alternative mortgage marketing tools like Highway.ai, Fello, myhomeIQ, and HouseCanary's ComeHome platform all offer some version of a home report or homeowner engagement experience. They aren't all the same product, and the differences matter depending on whether you're a loan officer, a real estate agent, or both.

Below is what each platform includes, based on their own product pages, pricing, and feature documentation, and where the meaningful gaps are.

1. Highway (MBS Highway + List Reports Home Report)

Highway is the parent company of MBS Highway, List Reports, and the Certified Mortgage Advisor program. The Home Report lives inside the List Reports product and is sold as a standalone add-on at $169/mo, or bundled into Highway's full suite.

What the Home Report includes:

- Monthly personalized email with current and forecast home value

- Neighborhood sales activity and equity position

- Cash-out refi opportunities and PMI removal alerts

- "Readiness to Move" scoring

- Up to 1,000 client capacity

- Branded interactive landing page with clear CTAs

- LO activity feed showing what clients engage with

- Automatic agent co-branding when an agent pairs with the LO through List Reports

What it doesn't include:

- Purchasing power calculator

- Short-term rental estimate

- Break-even refi analysis

- Predictive AI seller scoring

MBS Highway's core value is market intelligence for loan officers (real-time MBS data, lock/float alerts, daily videos from Barry Habib), and the Home Report is a client-facing add-on to that rather than the product's center of gravity. Highway's own marketing claims open rates above 75%, which directly positions it against Homebot.

For real estate agents: Agents can be co-branded alongside LOs in the Home Report when the LO uses List Reports and pairs with them. There is no native agent subscription path; the agent relationship flows through the LO's account.

Price reality check: To get MBS Highway's market intelligence tools plus the Home Report, you're looking at $199.95/mo + $169/mo = ~$370/mo combined. The Home Report standalone at $169/mo competes more directly with Homebot on price and scope.

2. Fello.ai

Fello is primarily a database marketing and AI lead intelligence platform. It is not a homeowner-facing monthly report tool in the same category as Homebot or Highway, but for mortgage professionals, it does include Dynamic Home Value Reports: automated, personalized reports that can cover multiple property valuations per contact, delivered via email or directed through branded landing pages.

What the home value report includes:

- Automated personalized home value estimates with equity data

- Multi-channel distribution (email, direct mail, web landing pages)

- Engagement tracking showing who opens and clicks

- AI-powered lead scoring and behavioral signals

- Database enrichment with MLS, tax assessor, and public records data

- Starter plan at $165/mo for 500 contacts; Growth plan at $499/mo for 3,000 contacts

What it doesn't include:

- Equity explorer

- Purchasing power module

- Short-term rental estimate

- Mortgage payment breakdown

- PMI calculator

- Standalone homeowner-facing digest experience

Fello is CRM-layer software rather than a standalone homeowner engagement platform. The homeowner experience, meaning what the client sees, is a branded landing page and email sequence rather than a deep interactive financial digest. The focus is on identifying intent signals on the professional's side, not on educating homeowners about their financial position.

For real estate agents: Fello is built primarily for real estate agents and teams focused on database marketing and seller lead generation. Mortgage professionals can use it, but the tool's architecture is lead-gen-first, not homeowner-retention-first. There is no native co-sponsorship model between LOs and agents.

The key distinction: Fello is a prospecting and database intelligence tool that includes home value outreach as one of its engagement channels. Homebot is a homeowner financial education platform that generates prospecting intelligence as a byproduct of client engagement. Those are meaningfully different orientations.

3. myhomeIQ

myhomeIQ is one of the closest feature-for-feature competitors to Homebot, targeting both loan officers and real estate agents with a monthly home report as its core product.

What the home report includes:

- Monthly personalized home value and equity report

- Loan payment tracker with principal vs. interest breakdown over time

- Home equity tracker with adjustable condition/details calculator

- Transaction estimator (net sheet showing what a sale would net the homeowner)

- Principal paydown forecaster for extra payment scenarios

- PMI removal alerts

- Pre-Mover Score (AI-based predictor of who's likely to sell in the next 12 months)

- Refinance certificate tools and lead generation funnels

- Free agent access when partnered with an LO on the platform

What it doesn't include:

- Short-term rental income estimate

- Purchasing power calculator

- Private home search experience for buyers

- Native partner network in the sense that Homebot has built with the Homebot Network

- W.I.N. personalization layer

- Homeowner Check-In feature for explicit intent signals

For real estate agents: Free access when partnered with an LO on the platform. Agents get co-branded monthly reports sent to their shared clients and receive alerts when a client is showing intent signals. This is a genuine differentiator for myhomeIQ. The free agent tier has driven strong adoption among agents who want a client engagement tool without a subscription cost.

Engagement numbers: Users report open rates above 83% in reviews, though these are self-reported from individual accounts rather than platform-wide figures. Pricing starts at $149/mo, making it the closest price competitor to Homebot's entry tier.

The honest comparison: myhomeIQ covers more homeowner financial ground than Highway's Home Report or Fello's home value reports. Where Homebot pulls ahead is in the depth of the homeowner experience (purchasing power, equity explorer, short-term rental, private home search), the behavioral intent data infrastructure, and the Homebot Network as a formalized lender-agent co-sponsorship model rather than a shared reporting layer.

4. HouseCanary ComeHome

HouseCanary is primarily a data and analytics company serving institutional real estate investors, servicers, and lenders. ComeHome is their consumer-facing engagement platform, positioned as an enterprise-grade co-branded home search and homeowner dashboard for banks, credit unions, and mortgage servicers.

What the homeowner dashboard includes:

- Home value insights using HouseCanary's AVM (claimed 2.7% median absolute percentage error)

- Home improvement calculator with renovation ROI estimates

- Personalized financing options

- Neighborhood data and market context

- Property search integrated with current MLS listings

- Agent matching

- Behavioral tracking across 300+ consumer signals

- Automated personalized emails about property values and market trends

What it doesn't include:

- Refi break-even calculators

- Equity explorer for move-up scenarios

- Short-term rental estimates

- Predictive seller scoring

- Standalone monthly email digest experience

ComeHome is a homeowner dashboard that sits on a lender's branded web presence rather than a standalone email product. The platform is built for loan servicers and enterprise lenders managing large portfolios, not for individual loan officers or real estate agents managing their own databases.

For real estate agents: ComeHome includes agent matching, where homeowners can be connected to real estate agents through the platform, but this is a consumer-facing feature for the lender's homeowner base rather than a co-sponsorship model between individual LOs and their preferred agent partners.

The key distinction: ComeHome is an enterprise retention tool for institutions. The comparison to Homebot is less direct. A credit union deploying ComeHome is solving a different problem than an individual loan officer trying to stay top of mind with 400 past clients.

5. Homebot's Home Report: The Homeowner's Digest

Homebot is purpose-built for ongoing homeowner engagement. The Home Digest is Homebot's core product, not a secondary feature inside a market intelligence tool or a lead-gen add-on. Every module inside it has been designed around two goals: giving homeowners a reason to open it every month, and giving loan officers and real estate agents the signals to know when to reach out.

Engagement performance:

- 75% average open rate (vs. 20-30% for generic email campaigns)

- 50% monthly engagement rate

- 8 average homeowner check-ins per year

- Platform-wide figures across 8 million+ monthly consumers

What sets it apart:

- The only platform in this category with a formalized partner network (the Homebot Network) co-branding loan officers, real estate agents, insurance agents, and title agents inside the same monthly report

- Module-level placement at the exact moments homeowners are considering a purchase, sale, or refi

- Real-time behavioral signals from every client interaction feeding directly into the professional's activity feed

- Likelihood to Sell predictive scoring (89% of moves captured in top 50% of scores)

- Mobile app for homeowners, lead capture widget, and CRM integrations

For a complete side-by-side feature comparison, including additional platforms like Afordal, RETR, and MMI, visit the Homebot alternatives comparison page.

How Loan Officers and Real Estate Agents Use Automated Home Reports to Nurture Their Database

Home reports like The Homeowner's Digest produce transactions across three primary patterns that show up consistently in customer outcomes on the platform.

1. Identifying refinance opportunities across your past clients

When mortgage rates shift to create refinance opportunities, the Homeowner's Digest automatically surfaces the personalized scenario for clients in the database whose savings cross a meaningful threshold. The loan officer doesn't need to identify candidates manually or trigger a campaign. Activity comes from the client side, prompted by the math the digest presents on a monthly basis.

This pattern shows up consistently in customer outcomes. In a customer story from Caliber Home Loans, LO Dave Thomas described the digest contributing $2 to $3 million in pipeline every month, including during a national economic downturn.

For real estate agents: The same mechanism applies to the move-up conversation. When a homeowner's equity position crosses a threshold that makes upgrading financially viable, the digest surfaces it. Agents featured in the Homebot Network appear in the Equity Explorer at the moment the homeowner is running the numbers.

2. Catching move-up transactions before they happen elsewhere

As a homeowner's equity grows, the Purchasing Power calculation in the digest shows what their position would support buying. A client who entered the platform as a first-time buyer in 2015 with $40,000 in equity and now has $195,000 can see, every month, that they qualify for a substantially larger home. The calculation is something most homeowners are not running on their own. Real estate agents using Homebot report this is one of the most common ways past clients turn into listing appointments.

For real estate agents: Cold outreach to past clients to maintain visibility is unnecessary when you're embedded in the monthly digest. By the time a client engages with their Purchasing Power calculation, they're actively considering their next home, and the agent of record is already in front of them.

3. Generating warm referrals through consistent engagement

Referrals from existing clients tend to come from situations where the client has something concrete to point to. A homeowner receiving a monthly home report from their loan officer or real estate agent has a specific, named touchpoint they reference when a friend asks about refinancing or selling. The referral path requires no outreach campaign and no incentive program. It works because the professional is already in front of the client every month with information worth opening.

This dynamic is consistent with broader research on homeowner financial behavior. As research from NAR has documented, homeowners hold dramatically more net worth than renters, with home equity often the single largest asset on their balance sheet. When a homeowner has questions about that asset, the professional whose name appears on their monthly home report is the one they call.

Conclusion: Start Sending Your Clients Home Reports

Setting up Homebot and sending automated home reports to customers is straightforward and does not require a marketing operations team.

What you need:

- Your client list, ideally as a CSV with names, email addresses, and property addresses

- Your branding details (name, photo, contact info)

- About 5 to 10 minutes to upload and configure

What you don't need:

- A design background

- A copywriter

- An hour of your week every month to maintain it

- Manual home value tracking or content creation

A simple 90-day starting plan:

- Upload your last 50 closings. These are your warmest contacts: people who closed with you recently, who know you, and who are most likely to engage.

- Configure your branding and add any agent or insurance partners through the Homebot Network for co-sponsorship.

- Track engagement and follow up. Most loan officers and agents have at least one conversation in 90 days they wouldn't have had otherwise. Many have several.

Homebot makes it simple to get your clients to sign up through the home value lead capture widget and promotional asset template library.

Ready to dig deeper? See Homebot's loan officer pricing and plans or the real estate agent pricing page for plan details or request a demo today..