Monthly Mortgage Digest

Rates Are Up, Buyers Are Still Out: What March 2026 Means for Your Pipeline

.png)

In late February, the average 30-year mortgage rate dipped below 6% for the first time in years. Buyers got excited. Then, in just five weeks, rates shot back up to 6.46%.

That swing caught a lot of people off guard. But here's what the headlines missed: buyers kept shopping anyway. Pending home sales rose 4.6% in March compared to last year, and the number of people actively browsing listings online was up 32%.

This digest breaks down what caused the rate jump, why there still aren't enough homes to buy, and what your clients are doing right now - even with rates back above 6%. The lenders and real estate agents winning this spring started moving before the dust settled. Here's what you need to know.

What's Happening in the Market

1. Rates Dropped Below 6% - Then Shot Back Up in Five Weeks

For one brief moment in late February, mortgage rates fell to 5.98% - the first time below 6% in years. It felt like a turning point. Then, almost immediately, rates climbed back up. By late March, the average 30-year rate had jumped nearly 50 basis points to 6.46%. As of early April, rates are sitting at 6.43% - still well above where they were six weeks ago.

Why did this happen? A few things hit at once.

- Global Conflict Pushed Oil Prices Up - Tensions overseas sent oil prices toward $100 a barrel. Higher oil prices mean higher inflation. When inflation goes up, mortgage rates tend to follow.

- The Government Proposed Big New Spending - A large increase in federal spending made investors nervous about how much the country is borrowing. The bond market reacted by pushing interest rates up across the board - and mortgage rates moved with them.

The Federal Reserve held its rates steady at its March meeting - it's taking a wait-and-see approach. Fannie Mae's March forecast still projects rates falling to 5.7% by the end of 2026. But that forecast was made before rates spiked again. The Mortgage Bankers Association expects rates to stay above 6% for all of 2026. For now, plan around 6%-6.5%.

What this means for lenders:

- Check your pipeline: Anyone you pre-approved in February at 6.1% is now looking at a higher payment. Call them today and check if they've locked their rate. If they haven't, this is an urgent conversation.

- Skip the rate refinance, start the equity conversation: Right now, most clients aren't going to refinance to get a lower rate. The refinance conversations worth having are about equity: home equity loans, cash-out options for people who need to cover big expenses.

- Run a buydown scenario: For buyers currently under contract, run a seller-paid rate buydown scenario. A buydown lets the seller pay to lower the buyer's rate for the first year or two. It's often more effective than a price cut.

What this means for agents:

- Re-qualify your February buyers: Buyers you worked with earlier in the year may need to re-qualify. Their pre-approval was for a lower rate. Talk to your lending partners now - before a contract surfaces the problem.

- Price check your active listings: A home listed at $400,000 when rates were 6.1% hits buyers differently now that rates are 6.4%. Make sure your listings reflect today's rate environment.

- Think buydowns before price cuts: A seller-paid buydown can save a buyer hundreds of dollars a month for the first two years - and it often costs the seller less than a price reduction.

2. Refinances Are Quiet - But Equity Conversations Are Wide Open

About 81% of homeowners in the U.S. already have a mortgage rate below 6%. That means most people aren't going to refinance right now just to save on their rate - it wouldn't make financial sense. But that doesn't mean there's nothing to talk about. Many of these same homeowners have built up a lot of home equity over the past few years. That equity is money they can access - to pay off debt, fund a renovation, or cover a major expense - without touching their low-rate mortgage.

There are some real refinance opportunities hiding in most loan portfolios. Homeowners who took adjustable-rate mortgages in 2022-2024 are now seeing their rates change - switching them to a fixed rate could give them more predictability. Purchase applications are running about 10% above last year, so for most lenders right now, new purchase loans are where the volume is.

What this means for lenders

- Review your adjustable-rate clients: Go through your past clients and find anyone who took an adjustable-rate mortgage in 2022, 2023, or 2024. Their rate may be changing soon. A fixed-rate option could be worth presenting.

- Start the equity conversation now: Don't wait for rates to drop. Clients who bought in 2019 or earlier, or who made upgrades during the pandemic, likely have meaningful equity sitting available.

- Make buydowns standard: For every active purchase, prepare a scenario showing the buyer's payment in Year 1, Year 2, and Year 3. Build this into your process so it's ready before the client asks.

3. There Aren't Enough Homes - and That Won't Change Anytime Soon

The U.S. is short about 4 million homes. That's not a new problem - it's been building for over a decade. In 2025, about 1.41 million new households formed while only 1.36 million homes were built. That gap adds up over time. Even if builders tried to build 50% more homes per year starting today, it would still take about seven years to catch up. The South is the hardest hit with a shortage of 1.62 million homes, followed by the Northeast at 952,000, the Midwest at 865,000, and the West at 660,000.

One big reason supply stays low: homeowners aren't selling. A recent ICE survey found that 62% of homeowners have no plans to sell - up from 55% in 2024. Among baby boomers, that number jumps to 80%. Many of these homeowners locked in a 3% mortgage rate during the pandemic and don't want to give it up. Active listings are up 8% from last March, but they're still 11% below their pre-pandemic level.

Fannie Mae's March report also lowered its expectations for new home building this year. Builders are dealing with rising costs, zoning restrictions, and labor shortages. Fewer new homes being built means the shortage gets worse before it gets better.

What this means for lenders:

- Reassure existing clients: Home prices aren't likely to drop in a meaningful way - there simply aren't enough homes for that to happen. That's good news for your clients' home values and equity positions.

- Get creative for first-time buyers: Look into assumable loans - where a buyer can take over a seller's existing mortgage, sometimes at a much lower rate. Also explore down payment assistance programs available in your area.

- Invest in builder relationships: New construction is worth prioritizing. Builders are offering rate buydowns and covering closing costs in ways that most regular sellers don't. If you have builder relationships, use them.

What this means for agents:

- Remind sellers they have leverage: Even with high rates, there are more buyers than available homes in most markets. A well-priced listing will get attention.

- Focus on life-event sellers: The sellers most likely to move right now are people with something pushing them - a new baby, a divorce, a job change, a need to downsize. These are your listing conversations.

- Bring up new construction with every buyer: Builders are offering deals - rate buydowns, covered closing costs, waived fees - that you won't find on most resale homes.

4. Buyers Kept Showing Up in March - Even as Rates Climbed

Despite the rate jump, the numbers show buyers stayed active. Pending home sales - contracts signed but not yet closed - rose 4.6% compared to last March. That's the second-highest monthly total since the pandemic housing boom ended in mid-2022. Even more telling: people browsed 32% more listings per day on major home search platforms than they did last March. Buyers are looking. They just need to be helped across the finish line.

Mortgage applications rose 3.2% in early March, and purchase volume was running about 10% above the same time last year. Home sales in February rose 1.7% from January - a sign that the market had real momentum before rates spiked again. According to ICE, March affordability was the best it's been for that month in four years. In 99 out of 100 major markets, buying a home was more affordable in March 2026 than it was in March 2025.

The average home value is $365,545. Homes that get listed are going under contract in about 19 days. About 22.6% of listings had a price cut in March - down slightly from last year - which means most sellers are pricing accurately from the start.

What this means for lenders:

- Focus on purchase loans: This is a purchase market right now. Every pre-approval you complete this month is a potential closed deal this spring or summer.

- Get buyers ready before they shop: Help them get their paperwork done before they find a house, not after. With homes going pending in 19 days, there's no time to scramble once a buyer falls in love with a property.

- Have a buydown ready for every negotiation: It could be the difference between a deal and a dead end.

What this means for agents:

- Price for today's rates, not February's: The 32% jump in listing page views tells you buyers are paying close attention. Make sure your listings look sharp and reflect the current rate environment.

- Help buyers get financing done first: With homes pending in 19 days, buyers who have financing ready before they shop will beat out the ones scrambling to get pre-approved after the open house.

- Use price cuts as a negotiating signal: About 1 in 4 listings took a price cut last month. That's a window for buyers - and a good reason to help sellers price right the first time rather than face a reduction later.

5. Buying a Home Is the Hardest It's Been Since 1985 - But There Are Tools That Help

The National Association of Realtors' Housing Affordability Index fell to 78.3 in February - the lowest reading since August 1985. When this index drops below 100, it means the average household doesn't earn enough to comfortably afford the average home. At 78.3, a buyer would need to earn about 28% more than the current U.S. median income to make it work. The average monthly mortgage payment hit $2,695 in late March - and that's before property taxes, homeowner's insurance, and maintenance costs.

But affordability isn't equally bad everywhere. ICE's April report found that homes in the Midwest and Northeast are getting more affordable month over month. Western markets, especially coastal California, are still very expensive. The important number: in 99 of 100 major markets, buying a home costs less than it did a year ago - even with rates above 6%. That's a message worth sharing with clients who think now is a bad time to buy.

Three tools are making the biggest difference for buyers right now: assumable loans (taking over a seller's existing low-rate mortgage), seller-paid rate buydowns (the seller covers the cost of temporarily lowering the buyer's rate), and down payment assistance programs. These are real affordability options that can make the math work when rates are high.

What this means for lenders:

- Learn how assumable loans work: VA and FHA loans from 2020-2022 often have rates below 4%. A buyer who can take over one of those loans instead of getting a new one at 6.4% saves a lot of money. These deals take more time, but the savings are real.

- Map your down payment assistance options: Know every program available in your market and put together a simple reference list for your agent partners - it'll make you more valuable to them.

- Include insurance in every payment estimate: In some markets - especially Florida and Gulf Coast states - homeowner's insurance costs have risen sharply. Give buyers the full picture of the monthly cost, not just principal and interest.

What this means for agents:

- Use buyer math to ground pricing conversations: Show a seller that their buyer is budgeting $2,695 a month in principal and interest before taxes and insurance, and suddenly the list price conversation gets a lot more grounded.

- Know which listings have assumable loans: If a seller has a VA or FHA loan from 2020-2022, that loan may be transferable to the buyer at a much lower rate. Find these listings in your MLS before the other agent does.

- Think buydowns before price cuts: A seller-paid rate buydown often saves the buyer more money per month in Years 1 and 2 than an equivalent price reduction would.

6. Some Markets Are Hot. Some Are Cooling. Know Which One You're In.

The housing market isn't one thing right now - it's hundreds of local stories. Data shows pending sales surged 20.5% in West Palm Beach, FL in March, while New Brunswick, NJ and Nassau County, NY saw pending sales fall 19%. These places are in the same national market but are experiencing completely different realities. ICE's April report shows the Midwest and Northeast posting the strongest monthly price gains in nearly a year, while some Western markets are still softening. Home prices nationally are up 0.4% year over year.

Realtor.com's supply data shows where the housing shortage is worst. The South has the biggest absolute gap - 1.62 million missing homes. But the Northeast is the most undersupplied relative to how much it's building. It was actually the only region to improve in 2025, with new construction hitting its highest level since 2015. In many Midwest cities, homes are much more affordable than the national average - but there still aren't enough of them.

The national headlines don't tell you what's happening in your specific market. The agents and lenders who know their local numbers - active listings, days on market, how often homes sell over asking price - have a huge advantage right now.

What this means for lenders:

- Know your market category: A lender working in an affordable Midwest city has a different pitch than one working in coastal California. Tailor your approach accordingly.

- Prepare for hesitation in stretched markets: Rate-sensitive markets feel rate increases much faster. If you work in one of those markets, be ready for buyer hesitation and have affordability solutions prepared before you need them.

- Follow the pending sales data by ZIP code: The markets showing acceleration right now are where you should be concentrating your outreach.

What this means for agents:

- Ditch the national stats: Use your ZIP code data instead. How many active listings are there right now? How fast are homes going under contract? What percentage took a price cut? These are the numbers that matter in client conversations.

- Identify your leverage markets: The best sellers' markets right now are places where prices are improving but inventory is still low. If your market fits that description, your sellers have real leverage.

- Have the relocation conversation: For buyers with flexibility - remote workers, retirees - the Midwest offers dramatically better affordability. It's worth bringing up.

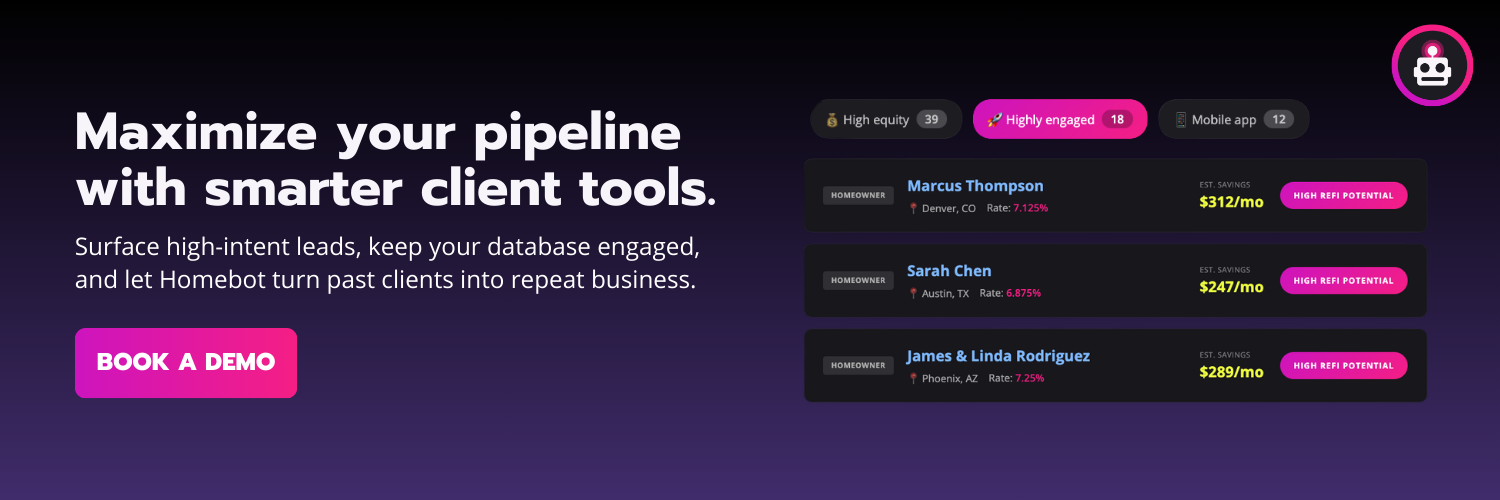

What We're Seeing Inside Homebot

1. Buyers Are Actively Searching - Not Just Browsing

Listings-search was the top source of client activity in March, driving 734,985 sessions on the platform. Listing-details came in second at 540,730, and Home Digest views at 311,020. Clients are looking at specific homes with intention. Your database is in active search mode right now, and available homes aren't keeping pace.

2. CMA Requests Are Up 6.3% - Some Sellers Are Ready to Move

CMA requests went 6.3% from February to March. When someone asks for a CMA, they're thinking seriously about selling. They may not be ready to list yet, but they're doing the math. With inventory still 11% below pre-pandemic levels and homes selling in about 19 days, a well-priced listing has real advantages. Every one of these CMA requests is a listing conversation waiting to happen.

3. Home Digest Messages Stayed High - Homeowners Are Paying Attention

Clients sent 6,876 messages through Home Digest in March, down slightly from 6,988 in February but still well above normal levels. Home Digest shows homeowners their estimated home value and how much equity they've built. When someone messages after opening that report, they're not just curious - they're thinking about next stepse. That could mean selling, tapping equity through a home equity loan, or just checking in on their financial picture. Either way, they've raised their hand. Prioritize these conversations.

4. Selling Is Still the #1 Thing Clients Are Focused On

In March, selling was the top client action at 1,150, followed by ownership at 992 and purchase at 903. That's notable. Even with rates above 6.4%, homeowners are still engaging with seller content. They're not waiting for rates to drop before they start thinking about their next move. The signal is already there - the clients just need someone to pick up the phone.

5. Clients Are Already Researching Affordability Tools on Their Own

"Buy downs as a seller concession" was the second most common conversation topic in March with 17 client chats. "Assumable loans" showed up as a topic for the first time this quarter. These clients have done the math. They know buying at 6.4% is hard, and they're looking for ways around it. The professionals who already know how to explain a buydown or find an assumable loan listing have a real edge. By the time the client asks, you should already have the answer.

For Lenders:

- Start the equity conversation with your locked-in clients: Many homeowners sitting on a low rate don't realize they can still access their equity without giving it up. Reach out to your high-equity clients and show them what they've built and what options are available - home equity loans, cash-out, lines of credit. Homebot makes it easy to identify who has the most equity and surface that conversation at the right moment.

- Build a buydown scenario for every active purchase: "Buy downs as a seller concession" was the #2 conversation topic in March. Have a simple breakdown ready that shows what the buyer's payment looks like in Year 1 and Year 2 with a seller-paid buydown. This turns a hard conversation about rates into a problem with a clear solution.

- Reach out to your adjustable-rate clients: Find every client with an adjustable-rate mortgage from 2022-2024 and check in. Their rate may be changing soon. Run the numbers and reach out before they start panicking about a notice in the mail.

For Real Estate Agents:

- Follow up on every March CMA request: CMA requests went up 6.3% to 1,063 in March. These homeowners are thinking about selling. A CMA without a follow-up call is a wasted lead. Call them with a simple question: "What would need to be true for you to make a move this year?" That's the conversation.

- Give hesitant buyers a real affordability picture: Most buyers are working off a rough estimate - they don't know what a home actually costs per month once you add taxes, insurance, and PMI. Walk them through the full payment. If assumable loans are relevant in your market, show them the actual rate difference. Homebot's private search builds all of this in automatically, so buyers can explore on their own without feeling pressured.

For Both Lenders & Real Estate Agents:

- Follow up with everyone who checked in on their home value last month: There were 6,876 Home Digest messages in March. These homeowners looked at their equity and chose to reach out - that's the warmest lead in any database. Don't let it go cold. A simple message works: "I saw you checked in recently - is there anything on your mind about your home right now?"

Closing Thought

March 2026 was a tough month to make sense of. Rates swung almost half a percent in five weeks. The country is 4 million homes short, and no one is close to solving that. Buying a home is harder than it's been in 40 years. And yet - buyers kept showing up. Sellers started requesting CMAs. Clients kept messaging about their equity. The market didn't stop moving just because the headlines got loud.

That's the point. The people winning in this market are not waiting for a perfect rate. They're staying close to their clients, reading the signals early, and showing up with real answers - not just rate updates. Homebot surfaces these signals before they become obvious: who's thinking about selling, who's watching their equity, who's actively looking at listings. Use that information. The professionals who act on it in April will have the pipelines everyone else wants in June.

The clearest signal in a complicated market is the one already sitting in your database. Use it.

See what Homebot surfaces in your database: Request a demo today.