Educational

Iran, Rates, and a 4-Million-Home Gap: What March 2026 Means for Your Pipeline

.png)

Spring arrived with a jolt. Mortgage rates dipped below 6% again - then reversed course in 48 hours as geopolitical tensions reignited oil-driven inflation fears. The 30-year fixed is back at 6.12%–6.15% and still in flux.

But the underlying story didn't change. A 4-million-home supply gap isn't closing soon. Homeowners are staying put longer than ever. Refinance applications were running 150% above last year just days ago. And Homebot's platform data shows consistent homeowner engagement month after month - regardless of what rates do.

The professionals winning this spring are already in motion. Here's the breakdown.

What's Happening in the Market

1. Rates Dropped Below 6% - Then Iran Changed the Equation

The 30-year fixed touched 5.99% on February 23.. Then U.S.-Israeli strikes killed Iran's Supreme Leader on March 1. Brent crude surged more than 8%, the 10-year Treasury pushed back above 4%, and the 30-year fixed was at 6.12%–6.15% by Tuesday morning.

Bright MLS Chief Economist Lisa Sturtevant says a limited conflict likely means a temporary rate spike with a spring rebound. Compass Chief Economist Mike Simonsen put it plainly: "All we can do is evaluate the opportunity in front of us. Do we love the home? Can we afford the home? If so, that's a good signal to buy."

What this means for lenders

- Watch the March 6 BLS jobs report closely. Weak employment data could offset the Iran-driven rate spike and reopen the purchase and refi window quickly.

- Get pre-approvals locked now. Clients who are approved and ready will have a real edge when spring inventory hits in April and May.

What this means for agents

- The sub-6% window closed fast. Buyers close to acting need to hear that waiting for another dip is a documented losing strategy - this won't be the last headline.

- Use the geopolitical uncertainty as a teaching moment:: geopolitical shocks affect sentiment, but they don't change how many homes are available or what rents are doing. The fundamentals haven't moved.

2. Refinance Applications Were Up 150% Year-Over-Year.

For the week ending February 20, the MBA's Refinance Index was up 4% week-over-week and 150% above the same week last year. Refinances made up 58.6% of all mortgage activity. VA refis alone jumped 26% in a single week as the 30-year fixed hit 6.09%.

Borrowers who closed in 2023–2024 at 7.5%–8% are in real savings territory. A 75–100 basis point reduction at current loan balances typically means $200–$400 in monthly savings.

What this means for lenders and agents

- Run your 2023-2024 purchase client list this week. These are your warmest refinance leads when rates pull back - have the savings math ready before they call you.

- Waiting for a "refi rebound" to start outreach is backwards. The rebound was already happening. The LOs in front of clients converted it. The ones waiting didn't.

- Leverage tools like Homebot to flag exactly when clients are in the money on a refi - every month, not just when rates hit a headline number.

3. The Supply Gap Hit 4 Million Homes - Inventory Isn't Coming to the Rescue

Realtor.com's 2026 Housing Supply Gap Report, released March 3, found the national shortage widened to 4.03 million homes in 2025 - up from 3.8 million in 2024 and the third-largest annual deficit since 2012. Single-family starts fell to 940,000 - the lowest since 2019.

The typical homeowner now stays in their home for 12 years - nearly double the 2005 average of 6.5 years. Economists estimate it would take roughly seven years to close the gap even under an optimistic construction scenario.

What this means for lenders

- Renovation loans (203k, HomeStyle) are a direct response to low inventory. If buyers can't find the right home, help them build it. Smaller markets are already showing strong renovation loan demand.

- Affordability is the dominant conversation right now - and assumable loans are worth resurfacing with clients. Yes, they take more work to navigate, but walking a buyer through an assumable builds trust, expands their options, and keeps you in the deal. That's the definition of a trusted advisor.

- Buyer concessions are back on the table too. In markets where sellers are sitting longer, rate buydowns and closing cost credits are real tools - not just negotiating tactics. LOs who can quickly model the payment difference on a buydown scenario will win more referrals from the agents they work with.

What this means for agents

- The lock-in effect is structural, not temporary. Well-priced listings in strong markets still move quickly - don't let buyers assume more options are coming.

- Price reductions in your market are signals to buyers, not sellers. Use supply data to create urgency with fence-sitters who think waiting will bring more choices.

4. Taxes and Insurance Now Average 21% of the Monthly Payment

A new Neighbors Bank analysis of nearly 450 metros found property taxes and homeowners insurance now account for an average of 21% of the monthly mortgage payment. Homeowners insurance has risen 31% since January 2020, with premiums projected to rise another 8% in both 2026 and 2027.

These costs don't show up in the rate quote - but they show up in escrow statements. A buyer qualifying on P&I alone could face a total payment 20%+ higher than expected.

What this means for lenders

- Run full PITI on every pre-approval, not just principal and interest. A borrower who qualifies on the rate quote alone could be hundreds short at closing once taxes and escrow are factored in.

- Existing homeowners on fixed-rate loans may be experiencing payment creep through annual escrow adjustments. That's a natural opener for a refinance or equity review conversation.

- Homebot’s private home search experience includes affordability calculators your clients can factor in taxes, insurance, and carrying costs.

What this means for agents

- Get insurance quotes for specific addresses before making offers - especially in Florida and coastal Texas, where insurance can represent 15-20% of the monthly payment. Deals fall through over this.

- Make insurance cost part of the buyer consultation upfront. A home that looks affordable at the listing price may not be once full carrying costs are on the table.

5. The Midwest Is Outperforming. The Sunbelt Is Correcting.

Cotality's March 2026 Home Price Index showed national appreciation at just 0.74% year-over-year in January - down sharply from 3.43% at the start of 2025. The Midwest posted 3.56% average annual growth, led by Illinois (+4.91%), Wisconsin (+4.78%), and Nebraska (+4.75%). In the Northeast, New Jersey (+5.6%) and Connecticut (+5.26%) outperformed.

Meanwhile, pandemic-era boom markets are correcting: Florida fell 2.36%, Colorado dropped 1.31%, and Texas was down 1.09% year-over-year as higher insurance, property taxes, and mortgage rates weigh on demand.

What this means for lenders

- Midwest and Northeast buyers present stronger qualification profiles right now - lower purchase prices mean lower loan amounts and more manageable DTI ratios. These are good markets to be active in.

- If you're writing loans in Florida or Texas, underwrite conservatively. Insurance cost volatility in those markets adds risk that doesn't show up in the rate quote.

What this means for agents

- Midwest and Northeast markets offer a genuine first-time buyer opportunity in 2026: lower entry prices, tighter inventory, and steady appreciation - a more durable combination than cooling Sun Belt markets.

- If your listings are in Florida or Texas, pricing expectation conversations need to happen before you go live. Sellers are still anchored to 2022 comparables that no longer hold.

6. Timing the Market Is a Documented Losing Strategy

HousingWire's recent analysis lays out the cost clearly: buyers who waited through 2024 for rates to fall below 6% saw that moment arrive - briefly - and watched it evaporate within 48 hours of an Iran headline.

What this means for lenders

- Every month a borrower waits is a month of higher rent and no equity buildup. Run the math with clients on what a 12-month delay actually costs them in foregone principal paydown and appreciation.

- Frame the refi conversation the same way. Waiting for a "perfect" rate while sitting at 7.5% costs real money every month. The right rate to refi is the one that improves their situation today.

What this means for agents

- If clients waited through DOGE volatility, tariff headlines, and now a Middle East conflict - what event are they actually waiting for? Make that question explicit.

- Frame urgency around the supply gap, not the rate. Rates fluctuate. A 4-million-home shortage is structural - and the buyer who acts today has less competition than they will in six months.

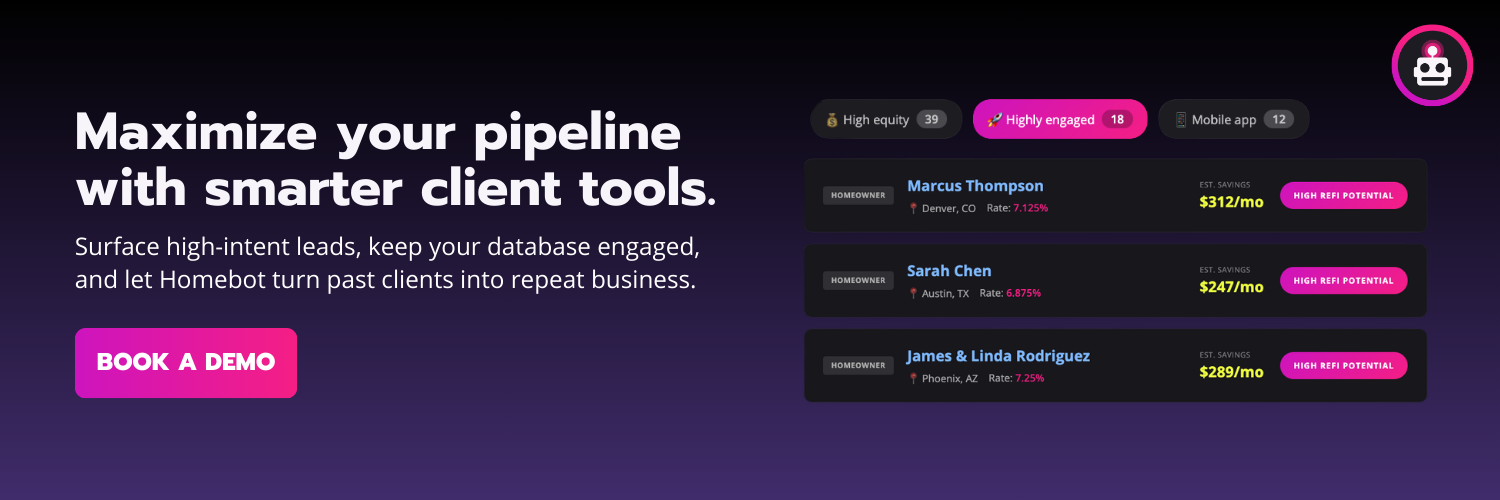

What We're Seeing Inside Homebot

The patterns in Homebot platform data for January and February 2026 tell the same story the headlines are telling - just from the homeowner's side. Across 5.77 million tracked clients, engagement held largely steady month-over-month. The opportunity to surface conversations doesn't require a rate catalyst.

Listing search behavior confirms buyer intent is real

Listings-search was the top DM source in both January (791k) and February (699k) - a slight pullback consistent with the late-February rate move, but still well ahead of 2025 levels. When homeowners are actively searching listings inside Homebot, they're evaluating whether a move makes sense. That intent exists every month - it just needs a nudge from you.

Home Digest DMs are up 41% - homeowners are watching their equity

The 41% jump in Home Digest DMs tells a specific story: homeowners aren't browsing listings right now, they're checking in on their own home's value. That's the lock-in effect in action. They're not ready to sell, but they're paying close attention to what they're sitting on. This is exactly the moment to open a conversation about what that equity can do - whether that's a HELOC, a cash-out refi, or just understanding their net proceeds if they did decide to move. Homebot's Home Digest surfaces this automatically - it's the nudge that starts the conversation before you have to.

CMA requests are down 12% - but don't read that as disengagement

Fewer formal CMA requests month-over-month isn't a sign that homeowners are losing interest in selling. It reflects the rate volatility in late February - homeowners pulled back from active evaluation mode when the 5.99% window closed. The selling intent is still there (1,280 selling actions in February). The CMA pullback just means those conversations need a reason to restart. Rate stability this spring is that reason.

'Selling' actions lead the platform - and that's actionable right now

The top client action in Homebot in both months was "selling." This mirrors national data showing homeowners staying put longer while watching equity grow. Homeowners checking their equity but who haven't listed yet are exactly the clients who need a direct net-proceeds conversation - not just a home value update.

Consistent engagement month-over-month is the whole point

February's numbers held largely steady relative to January - and that's the argument against waiting for a rate catalyst to engage your database. 1.6 million client actions in February alone. Homeowners checking home values, running purchase scenarios, requesting CMAs - at volume, every month. The professionals acting on that data consistently will outconvert those waiting for a favorable rate environment to justify outreach.

6 Actions to Take This Week

- Run your 2023-2024 purchase client list today. Anyone who closed at 7.5% or above has a real refinance conversation to have when rates return to 6.00%-6.10% - which is exactly where we were two weeks ago. Have the savings math ready before they call you.

- Reach out to clients engaging with the Home Digest. A 41% jump in Home Digest DMs means homeowners are actively watching their equity. Start with a simple question: do they know what they could do with what they've built? HELOCs, cash-out refis, and net-proceeds conversations all begin here.

- Restart CMA conversations with clients who went quiet in late February. The 12% drop in CMA requests tracks directly with the rate spike. Those homeowners didn't lose interest - they paused. A check-in this week with a current market update is a low-pressure way to reopen the door.

- Start affordability conversations that include the full PITI picture. With taxes and insurance now averaging 21% of total payments, buyers who budgeted around a rate quote alone may find a shortfall at closing.

- Reconnect with fence-sitters using the Iran situation as context, not alarm. The volatility this week is a teachable moment. The underlying fundamentals haven't changed: low inventory, rising rents, and steady appreciation in strong markets.

- Prepare renovation loan options for clients stuck on inventory. The 4-million-home supply gap isn't closing anytime soon. A 203(k) or HomeStyle loan is a differentiated conversation most competitors aren't having.

Closing Thought

March is reminding everyone that this market doesn't wait for certainty. The professionals winning this spring are already in motion - who ran their refinance lists before the Iran news hit, who had CMA conversations with Homebot clients before rates ticked back up, who helped buyers build conviction rather than waiting for a rate they could feel good about.

The structural story hasn't changed: not enough homes, not enough inventory, and 5.77 million homeowners whose equity and buying power are shifting every month. Homebot surfaces those signals consistently - regardless of what rates do. The data is in front of you. Act on it.

Ready to see which clients are ready to move? Request a Homebot demo →