Loan Officers

Mortgage Refinance Leads: How to Generate Them on Autopilot

How to Generate Mortgage Refinance Leads on Autopilot

-

What this covers: A four-step system for generating mortgage refinance leads from your existing client database, automatically.

-

Why it matters: Rates are volatile, the refi window opens fast, and most LOs don't have a system in place when it does.

-

What you'll identify: Which clients in your database are refinance-ready right now, and which ones need a few more months of nurturing.

-

What's included: The rate gap framework, a rate-drop alert setup, a passive nurture strategy, and a behavioral intent playbook.

-

Who it's for: Loan officers who want to stop guessing and start working a ranked, ready-to-call refinance lead list.

Rates hit 7.8% in 2023. Some of those borrowers are sitting in your database right now.

21.2% of U.S. homeowners with a mortgage have a rate above 6%, and according to Redfin, 1 in 5 of them could save money by refinancing today. Only 9.1% have actually done it, the lowest take-up rate since early 2020.

The mortgage refinance leads are there. The system to find them isn't.

Most loan officers are either blasting generic rate drop emails that get ignored, or manually reviewing loan files one by one and still missing the window. This guide lays out a better approach: one that runs automatically, surfaces the right clients at the right time, and keeps you in front of your database between rate moves so you're not starting cold when the market opens up.

Why Mortgage Refinance Leads Are Different From Purchase Leads

Purchase leads come from outside your sphere: Zillow forms, open house sign-ins, paid advertising. You're competing with three other LOs who got the same contact at the same time, and you're starting cold.

Refinance mortgage leads are different in three specific ways that matter for how you build your system:

1. The math on cold leads is brutal

- Shared leads convert at 1-3%

- Even exclusive purchased leads rarely close more than 1 in 20

- By the time you factor in cost per lead and time spent on cold contacts, the economics push toward the same conclusion every time

The fact of the matter is, 50-70% of a loan officer's income comes from past clients and referrals, not paid lead sources. Top producers aren't spending more on leads. They've built systems that make existing relationships do the work.

2. Your most exclusive refi leads can't be bought

The term "exclusive mortgage refinance leads" usually refers to leads not resold to other LOs. But the truly exclusive refinance lead is a past client in your own database. Someone who checks all four boxes:

- A rate above today's market

- Enough remaining loan term to justify closing costs

- Sufficient equity to qualify

- Hasn't started shopping elsewhere

No lead vendor can sell that relationship to your competition. It's built on a closed transaction. The question is whether you have a system to surface it.

3. The window opens fast and most LOs aren't watching

Refinance volume doesn't move gradually. It spikes.

- The MBA Refinance Index was 81% higher year-over-year as of early March 2026

- The borrowers who acted were already engaged with their lender before rates moved

- The lenders who captured that activity didn't send a rate blast at 3pm on a Wednesday

Their clients were already opening monthly home value updates. When rates moved, the follow-up was a warm conversation, not a cold pitch.

✅ Quick Check: When rates dropped earlier this year, how many past clients did you proactively reach out to, versus how many called you first? If it was mostly inbound, your database engagement system has a gap.

How to Generate Mortgage Refinance Leads on Autopilot: A 4-Step System

The system has four parts. Each one builds on the last. Together, they replace manual database reviews and reactive rate blasts with a process that runs continuously and surfaces the right clients at the right time.

Step 1: Identify Who in Your Database Is Refinance-Ready Right Now

The goal is a ranked call list, not a spreadsheet you rebuild every time rates move.

1. The rate gap rule

A 0.75% rate reduction is a more reliable threshold than the traditional 0.50%, once you account for typical closing costs of 2-3% and a 24-36 month payback horizon.

| Loan Balance | Rate Reduction | Est. Monthly Savings | Break-Even (est.) |

|---|---|---|---|

| $350,000 | 0.75% | $115-130/month | 24-30 months |

| $500,000 | 0.75% | $165-185/month | 18-24 months |

| $650,000 | 0.75% | $215-240/month | 16-20 months |

| $800,000 | 0.75% | $265-295/month | 14-18 months |

| $1,000,000 | 0.75% | $330-365/month | 12-16 months |

| $1,500,000 | 0.75% | $495-545/month | 10-14 months |

* Estimates based on a rate reduction from 6.75% to 6.00% on a 30-year fixed mortgage. Actual savings vary based on remaining loan term, closing costs, and current market rates. Verify with your loan origination software before using in client conversations.

2. The four qualification variables

- Rate gap: Current rate vs. today's market, needs to clear your break-even threshold

- Loan age: 2022-2023 originations at 6.5-8% are the core target. 2020-2021 closings at sub-3% are not.

- Equity position: Many 2022-2023 buyers have meaningful appreciation working in their favor

- Monthly savings: A useful floor is $100/month. Below that, closing costs are hard to justify unless cash flow is the driver

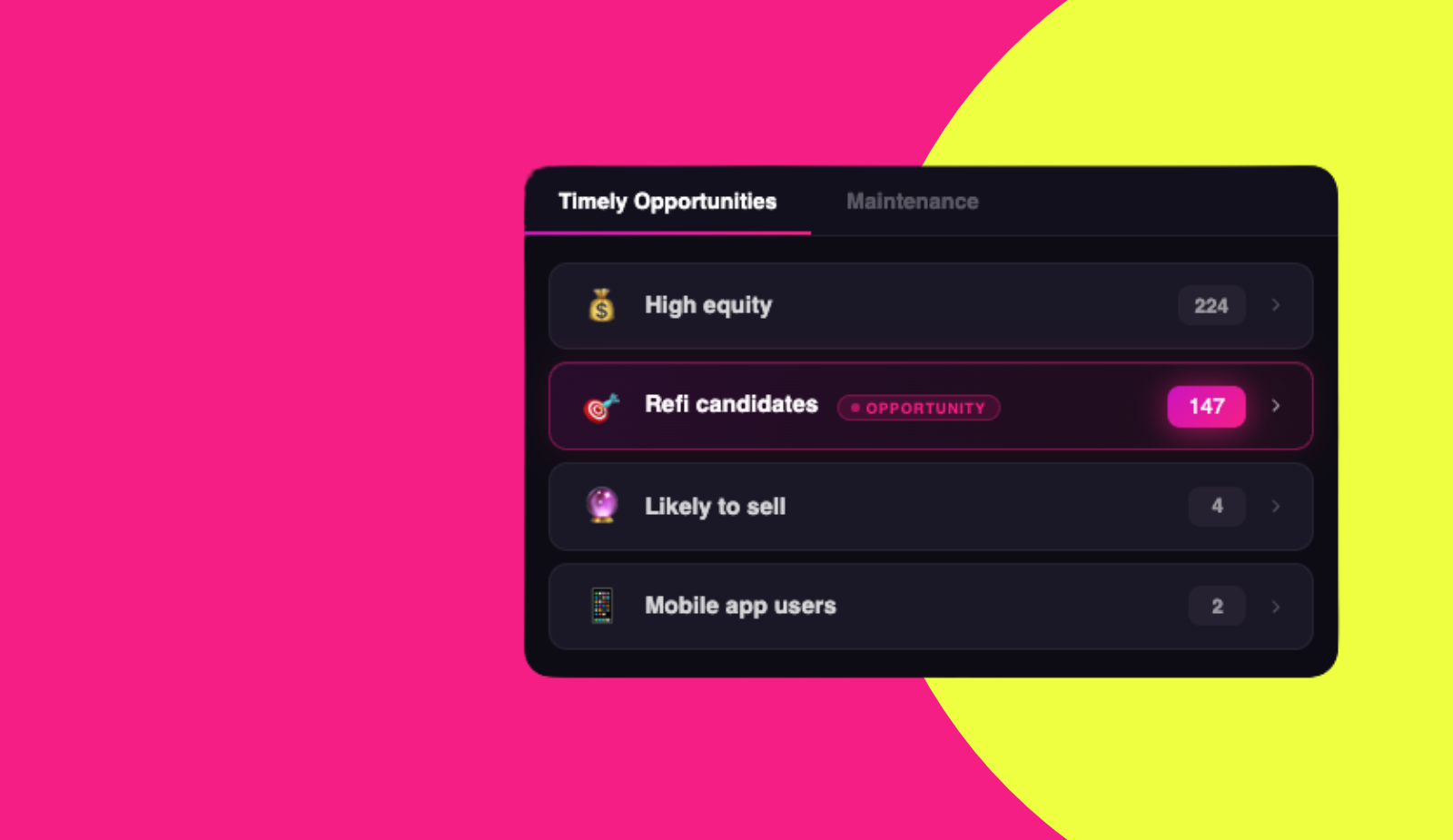

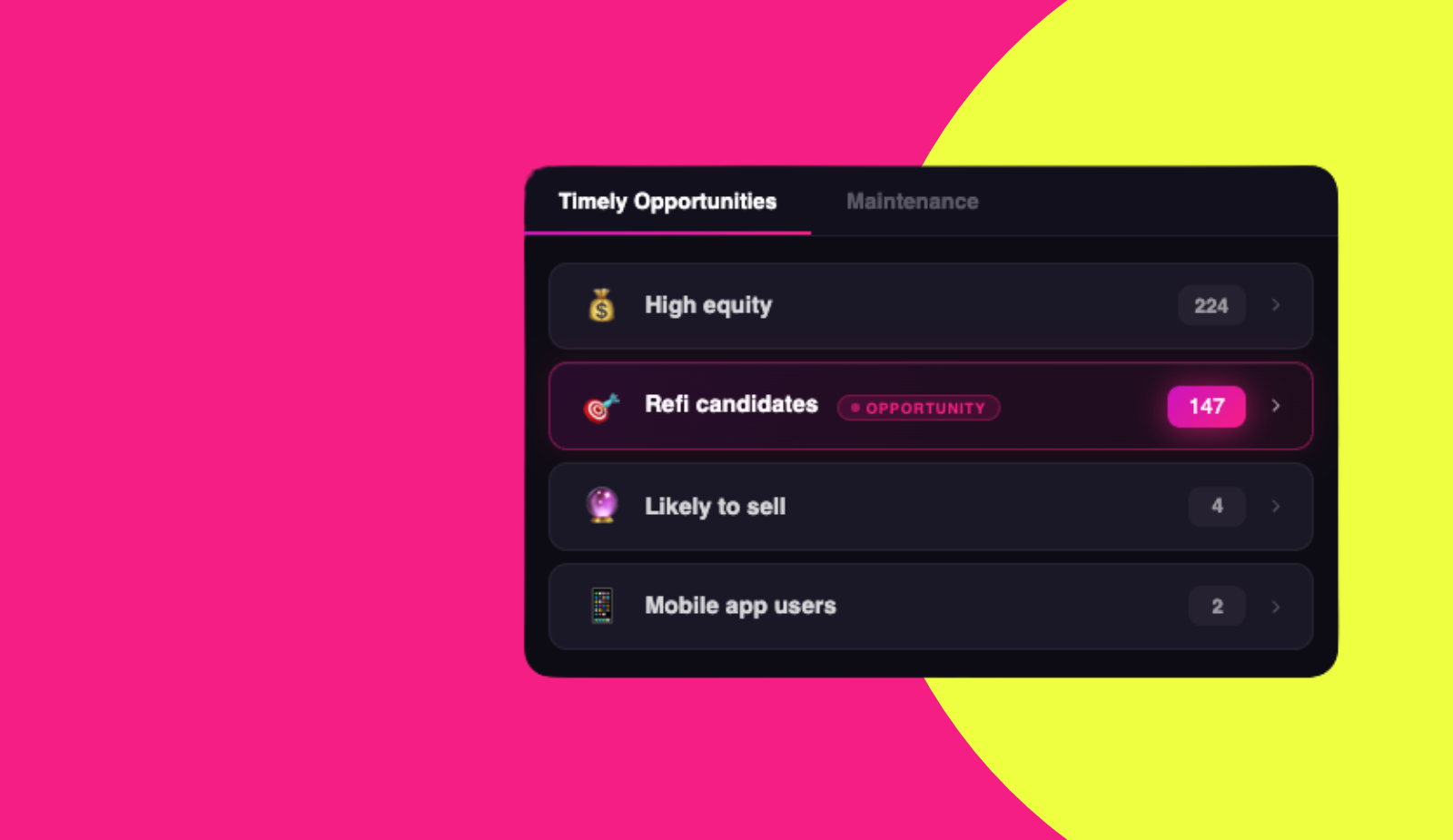

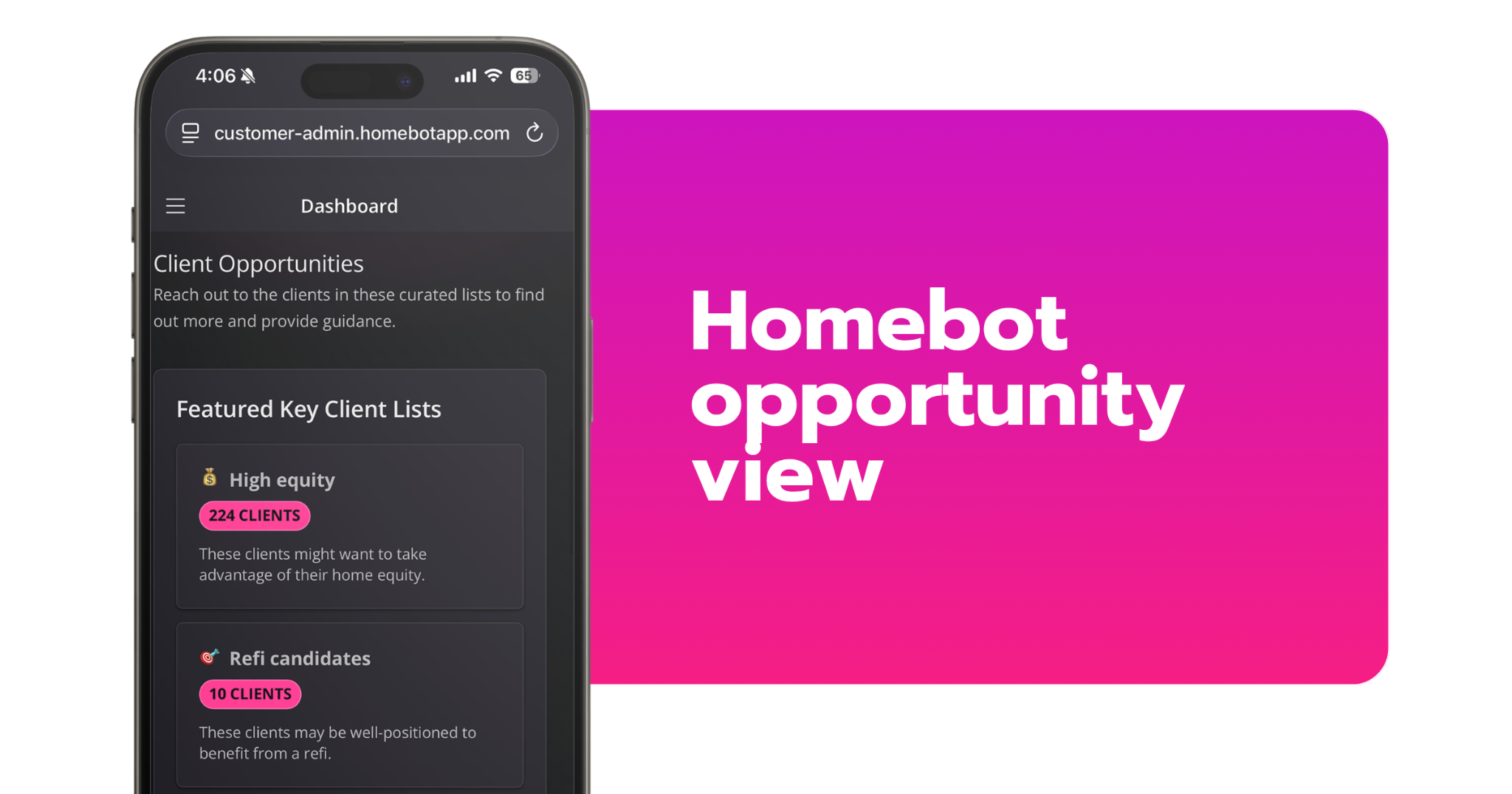

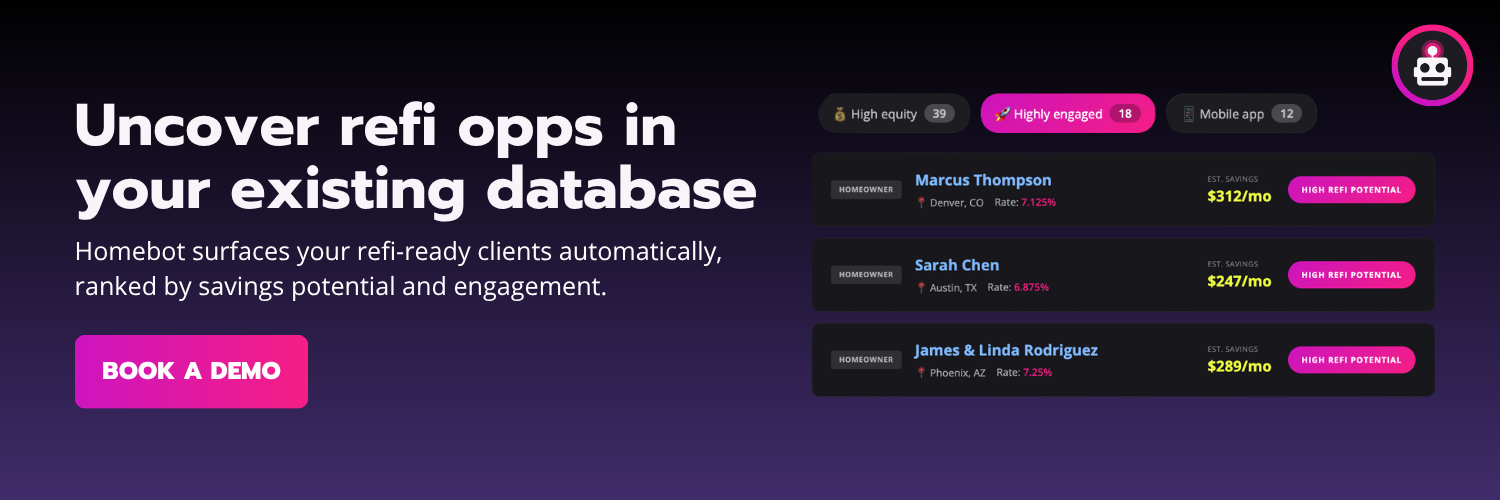

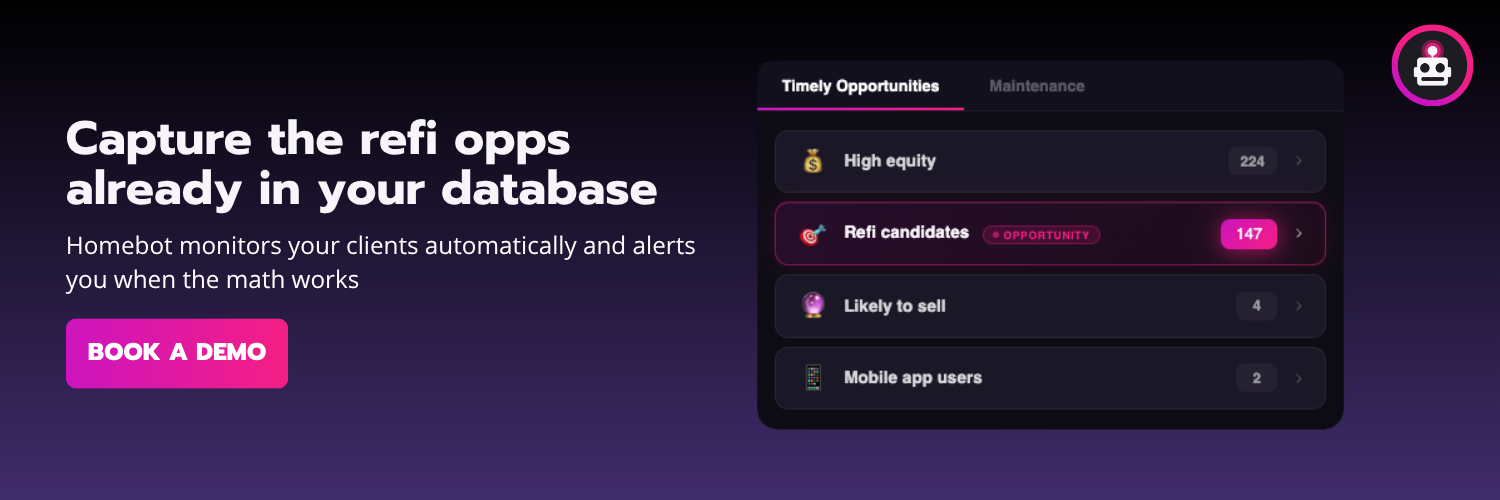

Working through this manually across 200-500 past clients isn't realistic. Homebot's Opportunities view pre-filters your database using all four variables and surfaces a prioritized call list ranked by estimated monthly savings and recent engagement with refi scenarios. You're not building a spreadsheet. You're opening a call list.

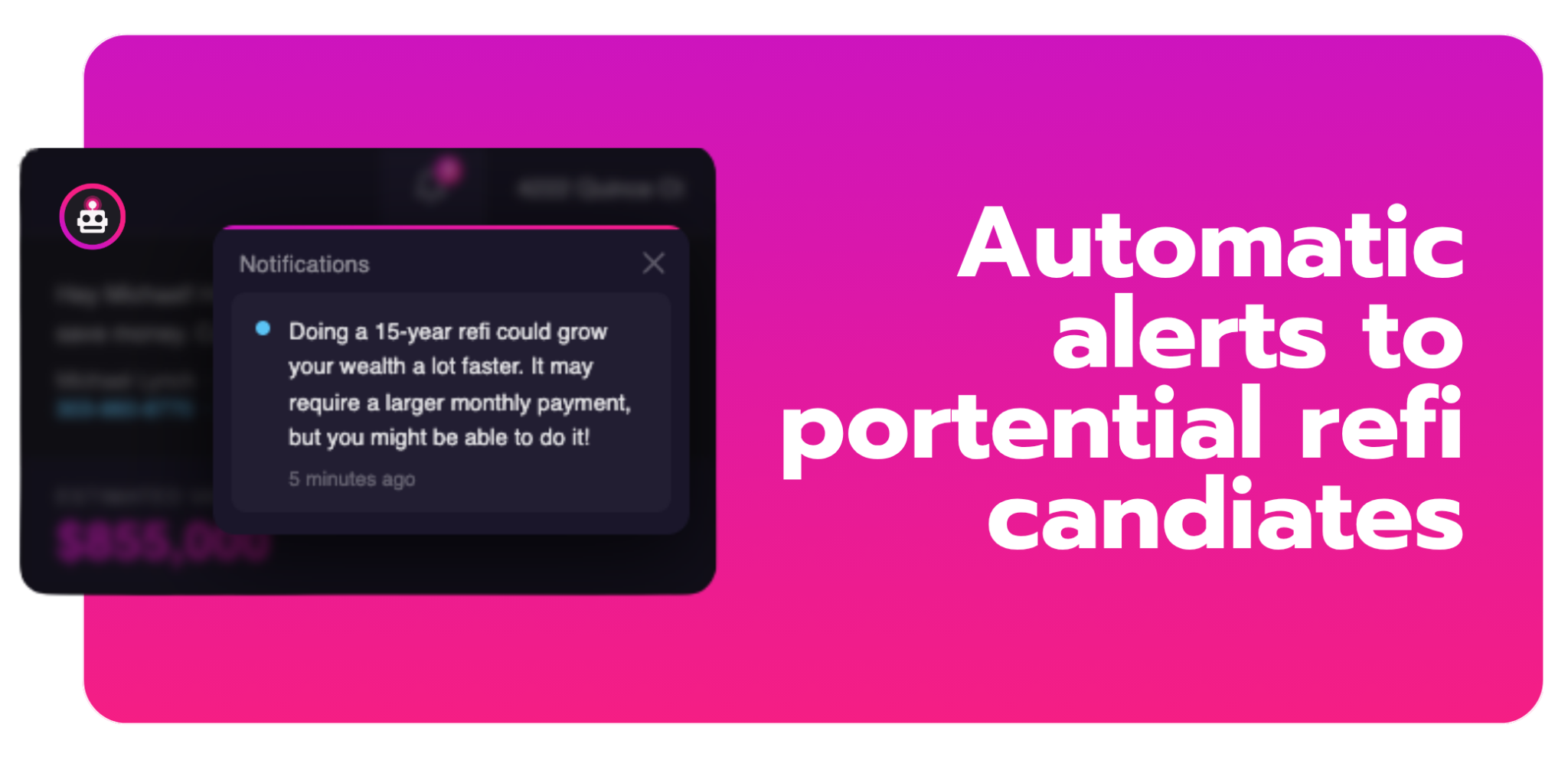

Step 2: Set Up Rate-Drop Alerts That Fire Before Clients Start Shopping

When a sustained rate move happens, you have days, not weeks, before the most rate-sensitive borrowers in your database start getting calls from other lenders.

What a real rate-drop alert looks like

- Generic blast: "Rates fell, you might want to call people."

- Personalized alert: "Based on your 6.9% rate on a $380,000 balance, you could save approximately $210/month."

One reads like marketing. The other reads like advice. The difference shows up in open rates: 20% vs. 75%.

Two market timing signals worth watching

- 10-year Treasury: 30-year mortgage rates follow with a 1.5-2% spread. Sustained movement here is a leading indicator.

- MBA weekly application data: Rising refi volume confirms rate-sensitive borrowers are actually moving, not just window-shopping.

How it runs automatically

When Homebot detects a client has crossed a savings threshold, engagement emails fire under your name and branding without you doing anything. The client responds to you, not to a rate app.

✅ Quick Check: Do you have a way right now to see which clients would save at least $150/month if rates dropped 0.50%? If you'd need to build a spreadsheet to answer that, you'll be too slow when the window opens.

Step 3: Keep the "Not Yet" Clients Warm Without Chasing Them

Not every client is refinance-ready today. Some are 0.25% away from a meaningful threshold. Some need another year of appreciation to clear equity requirements. These aren't dead leads. They're warm prospects with a defined horizon.

Two angles worth staying in front of

- Rate gap: Monthly home value and rate updates keep clients aware of where they stand. When the math clears, the conversation is already warm.

- Equity: For clients who bought in 2020-2022, meaningful appreciation may make cash-out worth exploring even when the rate difference is marginal. Home improvement, debt consolidation, investment, reasons to access equity exist independent of rate environment.

The 13-month problem

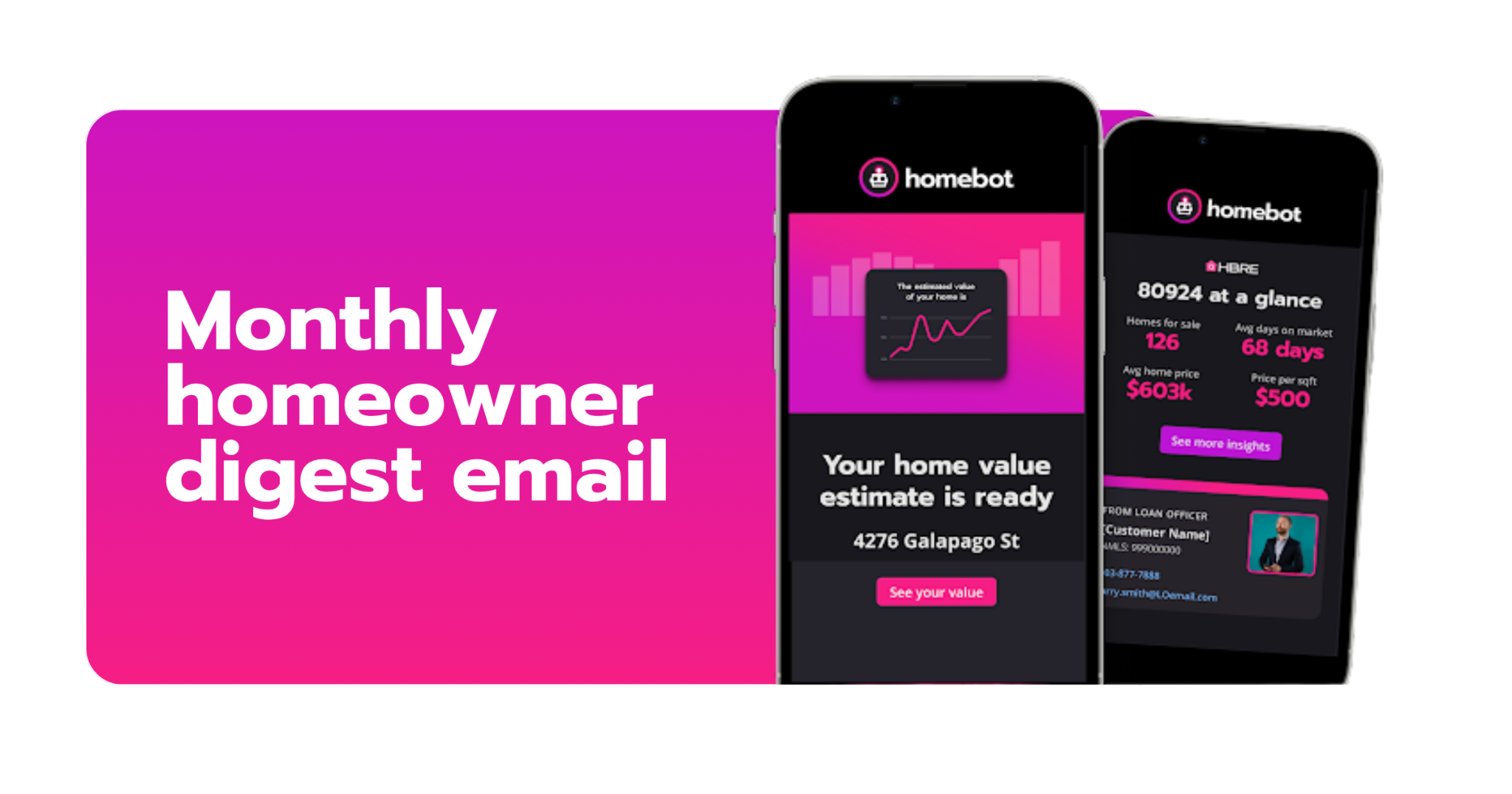

71% of clients forget their LO's name within 13 months of closing. Not because they were unhappy. Because nothing kept them connected.

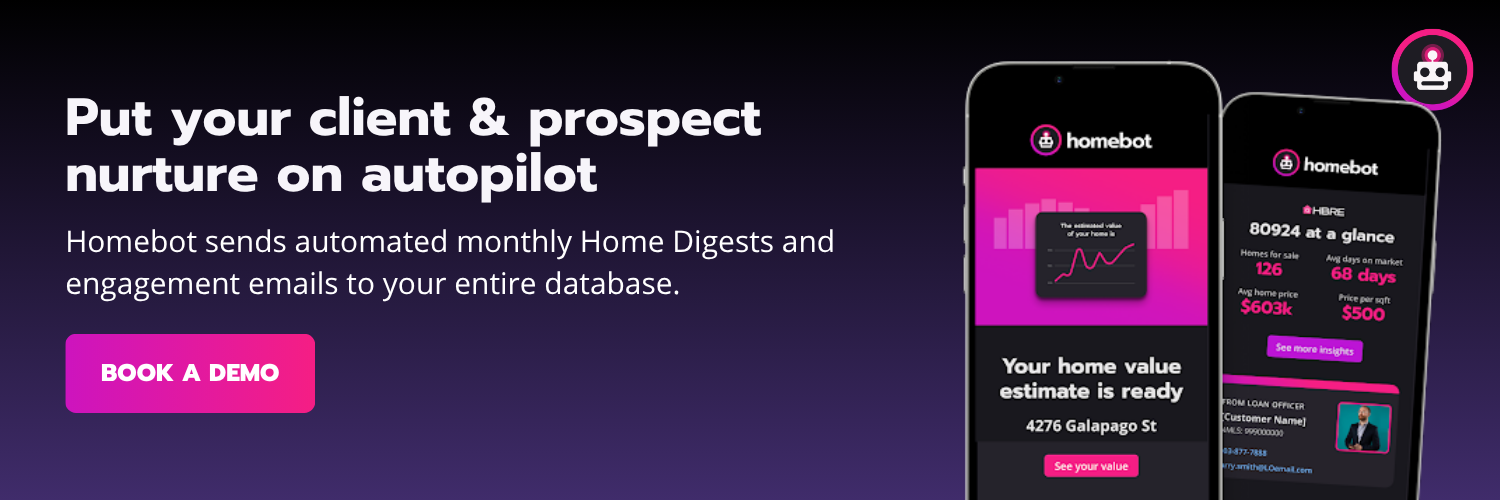

The touchpoints that work aren't generic newsletters. They're personalized insights tied to the client's actual situation: home value, equity position, what their refi scenario looks like at today's rates. Homebot's Home Digest delivers exactly this, monthly, automated, under your name. The 75% average open rate is because the content is specific to their home and their money.

When a client who's been getting your monthly digest for 18 months crosses into the refi window, you're not calling cold. You're continuing a conversation they've been having for a year.

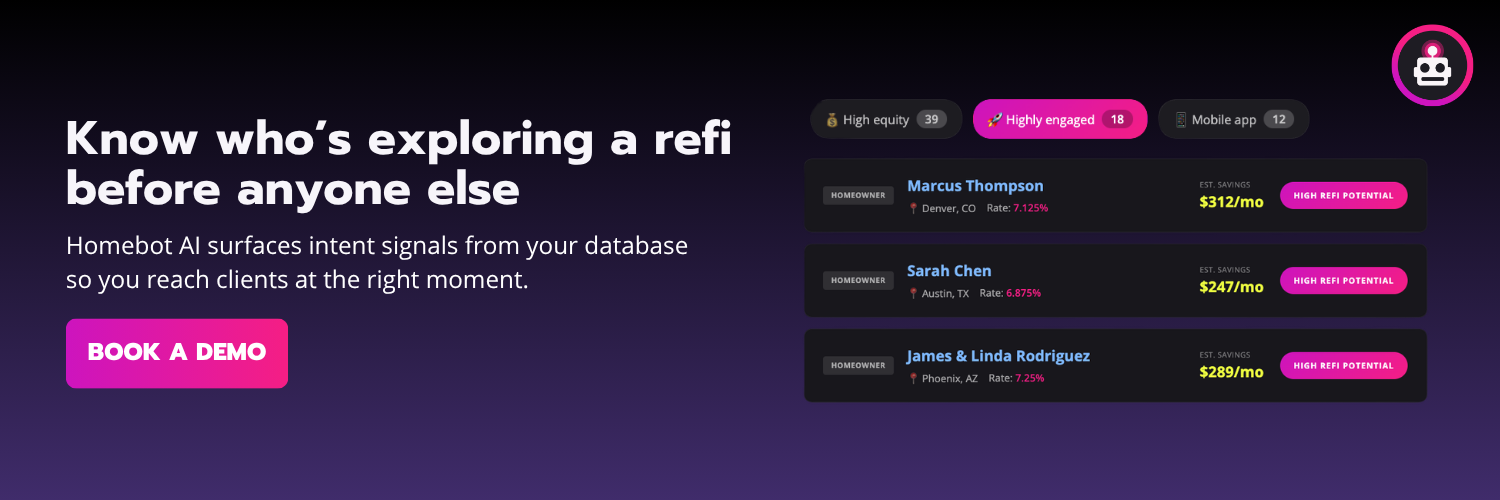

Step 4: Act on Intent Signals Before the Client Reaches Out

The best refinance lead isn't the one who calls you. It's the one who's been quietly running refi scenarios in their home digest for the past six weeks, before they've talked to anyone else.

There are several key mortgage intent signals to watch:

- Repeated refi scenario engagement: Returning to the refinance view 3+ times in 90 days means they're running the math, not just curious

- Frequent home value checks: Clients actively tracking equity are preparing for a financial decision

- Cash-out scenario exploration: Signals the client is thinking about a move, even if they haven't decided what kind

What changes when you have context

- Without a signal: "Hi [Client], wanted to reach out about current rates."

- With a signal: "Hi [Client], noticed you've been checking your equity recently, figured this was a good time to run through what your current rate looks like versus today's market."

The second call has a reason. The client doesn't feel cold-called. That conversation closes differently.

Homebot AI tracks these patterns and surfaces the high-intent clients in your dashboard. You don't monitor each client manually.

What the System Looks Like in Practice

Here's the full loop on a real rate move:

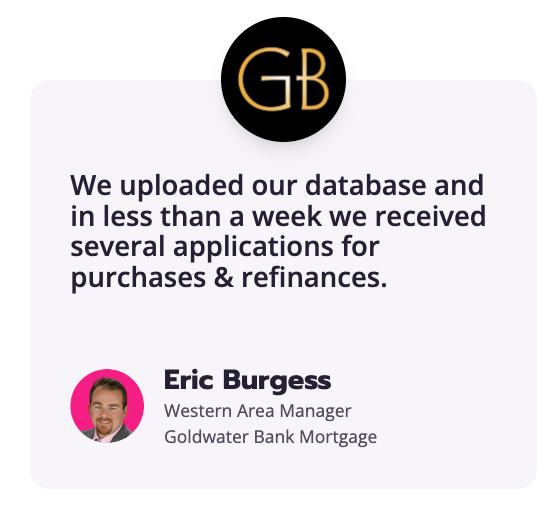

Eric Burgess, Western Area Manager at Goldwater Bank Mortgage, put it simply: "We uploaded our database and in less than a week we received several applications for purchases and refinances."

For a deeper look at how a marketing-forward lender built an entire refi opportunity workflow around Homebot, the Castle & Cooke Mortgage story is worth reading. Their team watches rate movement and sends loan officers directly to Homebot's Key Client Lists to find high-equity clients ready to refinance, 1 in 4 of their loan originations now comes through the platform.

The system doesn't replace the relationship. It makes the relationship scalable.

Conclusion: Your Next Refinance Leads Are Already in Your Database

When rates spike back up, most lenders who were manually tracking opportunities lose the thread. The database goes dormant. The next time rates dip, they rebuild momentum from scratch.

A system running in the background doesn't have this problem. It keeps clients engaged, keeps data current, and resurfaces opportunities automatically every time conditions improve.

Your action plan

- This week: Load your post-2021 database into a monitoring system. Run the rate gap analysis. Know your baseline, how many clients are within 0.75% of today's market?

- This month: Set up automated monthly engagement for every client. Home value updates, equity tracking, refi scenario modeling, personalized to each borrower.

- When rates move: Your system flags clients who crossed the savings threshold. Emails fire under your brand. You work the call list.

The window opens fast. The lenders already in front of their clients when it does are the ones who capture the volume.

Homebot's homeownership platform, including the Home Digest, opportunity detection, and engagement emails, is built to run this system automatically, surfacing the right clients, firing the right messages at the right time, and keeping your database engaged between rate moves so every conversation starts warm.

Frequently asked questions about generating mortgage refinance leads

-

The most effective mortgage refinance leads come from your existing client database, not from purchased lead lists. Past clients who closed at higher rates in 2022 to 2023 are the primary opportunity. The key is having a system that monitors their rate gap and equity position automatically, fires personalized outreach when the savings math crosses a meaningful threshold, and keeps them engaged between rate moves so the conversation starts warm. Homebot's opportunity detection automates this process across your entire database.

-

Exclusive mortgage refinance leads are leads not shared with competing lenders. The most exclusive refi lead possible is a past client in your database. No lead vendor can sell that relationship to your competitor. A past client who closed with you, trusts you, and is now sitting on a rate that's no longer competitive is your highest-quality, lowest-cost refinance opportunity. The challenge is identifying them before they start shopping elsewhere.

-

Four variables qualify a refinance opportunity: current rate vs. today's market (look for at least a 0.50 to 0.75% gap), loan age (2022 to 2023 originations in the 6.5% to 8% range are the primary target), equity position (clients need sufficient LTV margin at today's rates), and estimated monthly savings (a useful floor is $100 per month after accounting for closing costs and break-even timeline). Homebot surfaces clients who meet these criteria automatically, ranked by savings potential and weighted by recent engagement with refi-related content.

-

The autopilot approach has four components: a database monitoring system that tracks each client's rate gap and flags opportunities when conditions change; automated personalized engagement that keeps clients connected to their home value and equity data monthly; behavioral intent tracking that surfaces clients who are actively exploring refinancing before they reach out; and triggered outreach that fires under your brand when a client crosses the savings threshold. Together, these create a system that runs continuously in the background and surfaces ready-to-call opportunities without manual database review.

-

The right time to reach out is when three things are true: rates have dropped enough to create meaningful monthly savings for a specific client (usually a 0.50 to 0.75% gap or more), the client's break-even timeline on closing costs is reasonable given their plans to stay in the home, and the client has been engaged with their home wealth data recently. Reaching out based on all three conditions, rather than blasting an announcement every time rates move, is the difference between a warm conversation and a cold call. Homebot's engagement emails fire automatically when a client's individual savings threshold is crossed, so the timing is always client-specific rather than market-wide.