Real Estate Agents

How Agents Can Shift From A Transactional Expert to A Trusted Financial Resource

Clients aren't just asking transaction questions anymore. They're asking whether they should tap their HELOC or save for a larger down payment. They want to know if selling now and renting for a year makes financial sense. They're questioning whether the equity in their home should fund their kid's college or stay invested in real estate.

These aren't your typical real estate questions, they're financial planning questions. And the agents who can provide them with data are the ones winning business and generating ongoing referrals.

Why 'Are You Thinking of Buying or Selling?' Is the Wrong Opening Question

The traditional agent model positions you as a transaction facilitator. You show homes, write offers, negotiate contracts, and coordinate closings. It's valuable work, but it's also becoming replaceable. Buyers are finding properties online, researching neighborhoods themselves, and questioning whether they need full-service representation.

The advisor model positions you as a long-term financial resource who specializes in real estate. You help clients understand their housing wealth in the context of their broader financial picture. You provide ongoing market intelligence that informs decisions years before a transaction happens. Over time, you become the person they call first, because you have the data about their most valuable asset.

"But I'm Not a Financial Expert..."

You're not alone in thinking this, and you're actually ahead of most agents who never question their expertise boundaries. Here's the truth: you don't need to be a licensed financial advisor to provide market intelligence about real estate wealth. You're leveraging the information you already have access to, market data, equity tracking, appreciation trends, mortgage rate environments, and positioning it as the financial intelligence it actually is.

You're not giving investment advice or tax guidance. You're sharing data about what their home is worth, how much equity they've built, and what their buying power looks like. That's your lane, and you're the expert in it.

For everything beyond that? Partner with a loan officer who thinks like an advisor. The right lending partner helps you create content, answer complex financing questions, and step in when conversations venture into mortgage strategy or loan structuring. They become your financial co-pilot, handling the lending expertise while you handle the housing market intelligence.

Together, you're providing the real estate and financing data that helps clients make informed decisions with their actual financial advisor or CPA. Always encourage clients to consult with licensed financial advisors, CPAs, or attorneys for specific tax or investment advice. Think of it as knowing your strengths, respecting your boundaries, and building a team that fills the gaps.

Three Conversation Shifts That Transform How Clients See You

The shift to advisor happens in conversations, content, and consistency. It's not a one-time repositioning announcement, it's a steady evolution in how agents show up for their clients.

1. Change Your Opening Conversations

Stop leading with "Are you thinking about buying or selling?" Start leading with "Let's look at what your home has done for you financially since buying it" This one question completely changes how clients see you. Agents are no longer waiting for their clients to decide they need a transaction. They’re proactively monitoring their most valuable asset for them.

When meeting with potential clients, spend the first fifteen minutes discussing their financial goals before ever talking about properties. Ask about their five-year vision, their concerns about market timing, and what they're trying to accomplish with their housing wealth. By shifting the focus of the conversation to their long term financial goals, clients tend to relax, open up, and start treating them like a trusted advisor rather than a service provider.

2. Provide Regular Financial Updates

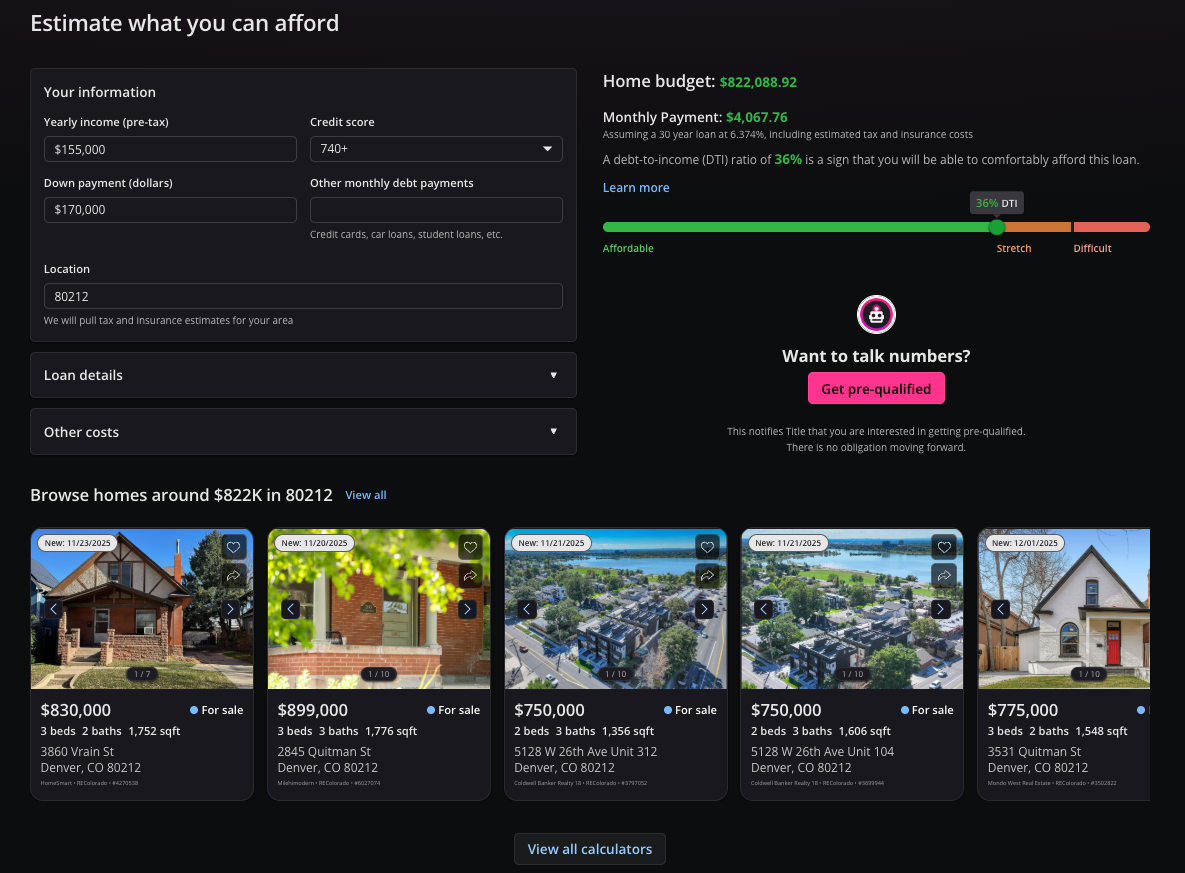

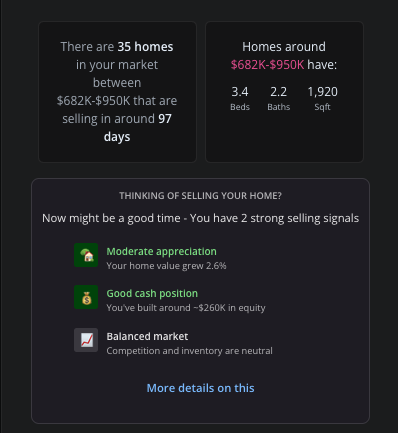

Consider sending clients personalized financial updates that show what their equity position looks like, how much their home has appreciated in the past year, and what that means for their buying power.

This is where having the right tools makes all the difference. Platforms like Homebot can handle this at scale, by sending each client a monthly digest showing their current equity, estimated home value, neighborhood trends, and potential financial moves available to them. You're providing advisory-level intelligence that’s scalable.

3. Answer Questions They Haven't Asked Yet

Advisors anticipate needs. Start creating content and having conversations that address the financial questions your clients will face in the next 6-18 months.

If you work with a lot of homeowners, create resources about how to leverage equity for home improvements to increase value, and whether paying down the mortgage or investing extra cash makes more financial sense. If you serve downsizers, discuss strategies for structuring home sales to minimize tax exposure and the financial implications of aging in place versus moving. Partner with a trusted loan officer and tax professional to create content around subjects you are unsure of.

The Tech Stack That Makes You Look Like a Financial Genius

Positioning yourself as an advisor only works if you can back it up. Invest in tools that provide personalized, accurate data you can confidently share.

Homebot: Automated Financial Intelligence for Every Client

Homebot automatically delivers personalized financial data to every homeowner in your database each month, equity position, current home value, refinancing opportunities, and buying power based on their actual property and market conditions. No manual calculations, no spreadsheets, just actionable intelligence at scale.

You'll see which clients are actively engaging with their data and what topics they're exploring, so your follow-up conversations are timely and relevant instead of generic check-ins that feel like sales calls.

Here's the thing about becoming an advisor: it's about showing up consistently. When clients receive valuable insights from you every month, you become their go-to financial resource by default. You're top of mind not because you're pestering them, but because you're providing ongoing value they'd pay for elsewhere.

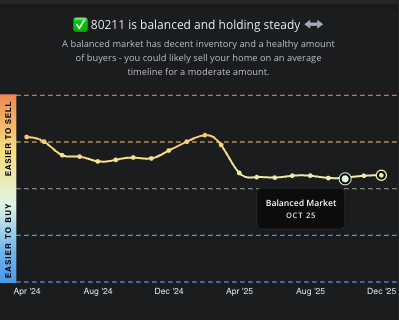

Comparative Market Analysis Tools That Go Beyond Comps

Your CMA shouldn't just show what nearby homes sold for, it should show clients what those sales mean for their financial position. Use tools that let you overlay equity calculations, illustrate net proceeds after closing costs, and compare the financial outcome of selling now versus waiting 6-12 months based on different appreciation scenarios.

When you present a CMA that says "If you sell at market value today, you'll net $347,000 after closing costs, which gives you $87,000 for a down payment on your next home, positioning you in the $625,000-$650,000 price range," you're providing advisory-level insight. When you just show them comps and say "I think we can list at $515,000," you're providing commodity service.

Mortgage Calculator Tools That Show Long-Term Impact

Show clients what different loan structures mean over 5, 10, and 30 years. Use calculators that illustrate the total interest paid, the equity built, and the financial outcome of different down payment scenarios.

When a client asks whether they should put 10% or 20% down, walk them through the numbers showing that keeping extra cash in reserves might cost them $180/month in PMI but preserves $40,000 in liquidity that could be invested elsewhere or used for home improvements that increase value.

Neighborhood-Level Investment Data

Go beyond telling clients that a neighborhood is "hot" or "up and coming." Show them the actual appreciation rates over the past 1, 3, and 5 years. Illustrate absorption rates, list-to-sale price ratios, and days on market trends that indicate whether an area is appreciating faster or slower than the broader market.

Clients who understand that the neighborhood they're considering has appreciated 18% in three years while the city average is 12% are making investment decisions, not just lifestyle decisions. Position yourself as the agent who provides that intelligence.

Partner With a Trusted Loan Officer

Your advisory positioning becomes exponentially more powerful when you partner with a loan officer who shares the same financial advisor mindset. Not all lenders are created equal. You need someone who thinks creatively about financing solutions, understands how to structure loans for clients in less-than-ideal financial situations, and views their role as a problem-solver.

The right lending partner doesn't just approve loans, they explore options most loan officers wouldn't consider. They know how to leverage gift funds, structure non-QM loans for self-employed clients, use bridge financing to help move-up buyers avoid contingencies, and find programs that work for buyers who don't fit conventional boxes. When you have a lender who can say "here's how we make this work" instead of "sorry, you don't qualify," you become the agent who gets deals done.

Through Homebot's co-sponsorship feature, you and your lending partner can both be connected to every financial question your client has. When your client receives their monthly digest showing equity position, potential refinancing savings, or buying power estimates, both you and your lender are looped in. When the client starts exploring mortgage options or asks questions about financing, you're both notified and can coordinate your response.

This creates something clients rarely experience. They're not bouncing between an agent who handles property questions and a lender who handles financing questions. They're being served by a coordinated team that understands their complete financial picture and works together to find the right home and the right loan for their specific situation.

The result? Clients feel nurtured and supported rather than transacted upon. They know you have their best interests in mind because you're not just handing them off to a lender,you're collaborating with a financial partner who's equally invested in their success. This is how you create lifelong clients who refer everyone they know, because they've experienced something fundamentally different from the typical agent-lender relationship.

When you position yourself as the advisor and partner with a lender who does the same, you're not just winning transactions, you're building a reputation as the team that helps people achieve their financial goals through real estate. That reputation becomes your most valuable marketing asset.

Real takes from our customers:

“Clients like the once a month email because it helps them understand their property value relevant to the current market. Homebot is an essential tool for my business that I can’t live without. I love how Homebot allows me to stay in touch with past clients without any effort on my part, and it is fantastic to get requests from clients asking for an updated CMA on their property. I perform annual CMA updates for all my clients and Homebot is an easy tool to store this data and deliver relevant information to my past clients.”

Heidi D., Relator on Homebot

The Referral Explosion That Follows

The advisory model creates a referral engine that the transactional model never can. Here's the reality: 88% of homeowners say they'd use their agent again, but only 12% actually do. That gap exists because with the traditional transactional approach, clients appreciate your service but forget about you once the deal closes.

When you're an advisor, especially when partnered with a trusted lender, clients think about you every time someone in their life mentions real estate, refinancing, equity, or housing wealth. You become top of mind, not an afterthought.

The referrals that come from advisory relationships are also higher quality. When choosing an agent, 35% of sellers consider reputation and 22% prioritize honesty and trustworthiness. The advisory model builds both. These referrals aren't price-sensitive leads shopping multiple agents, they're people who were told "you need to work with this agent because they really know their stuff." They come pre-sold on your value and rarely negotiate commission.

The advisory model also creates referrals from unexpected sources. Financial planners, CPAs, estate attorneys, and mortgage brokers start sending you clients because you're solving problems other agents don't have expertise in. You become part of a professional network rather than a commodity service provider competing with every other agent.

The Bottom Line

The gap between transactional guide and advisors isn't solely expertise, it's positioning. You already understand market dynamics, equity building, and real estate wealth strategies. The shift is being proactive about leading with that intelligence instead of waiting for transaction opportunities.

Clients are asking financial questions. The agents who answer them with data, not opinions, aren't just winning more business, they're building relationships that generate referrals for decades.

Interested in exploring Homebot as a potential solution? Sign up for a demo or check out a tour of Homebot.