Monthly Mortgage Digest

A New Fed Chair, a 6.53% Rate, and a Spring That Won’t Slow Down

.png)

The June 2026 Mortgage Digest: The Short Version

-

Rates climbed to 6.53%: The 30-year fixed hit its highest level since August 2025 in late May as geopolitical volatility lifted oil and inflation reached a three-year high. Kevin Warsh took over as Fed chair from Jerome Powell.

-

The spring stayed busy anyway: Pending sales rose for a sixth straight month and purchase applications ran about 7% above last year, even as week-to-week volume cooled with the rate climb.

-

Sellers adjusted, buyers rewarded them: Median list prices fell 2.4% year over year, the steepest drop since 2017, and new listings hit their highest May level since 2022. Realtor.com called it the most active spring in four years.

-

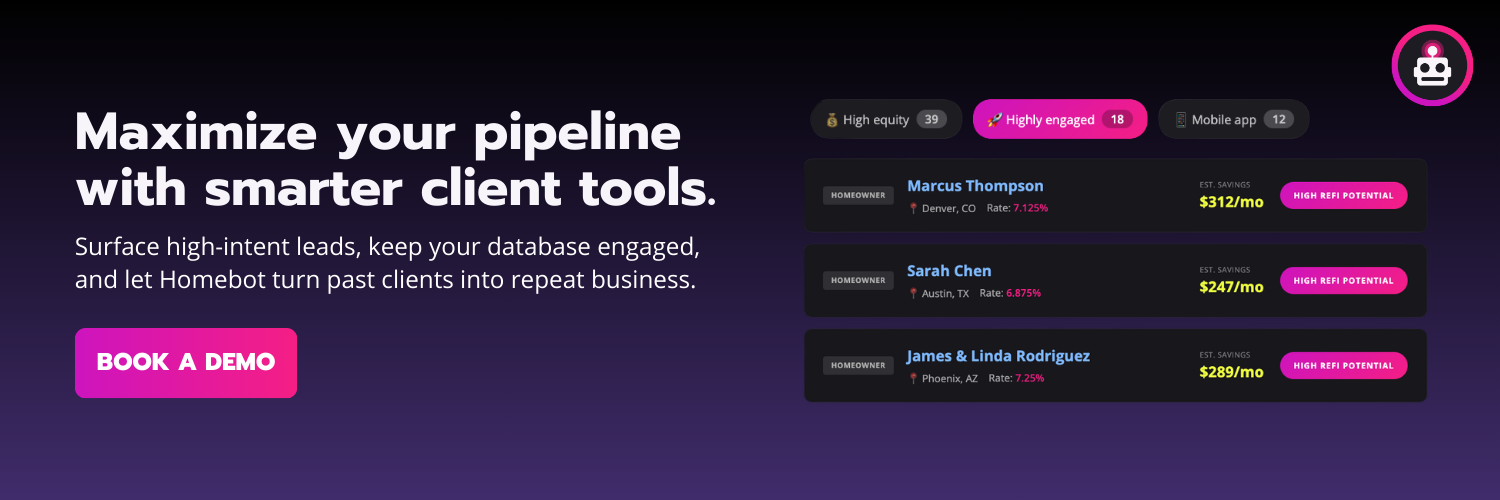

Your database is showing intent: Across 10M+ homeowners on Homebot, listings-search engagement rose 4% to 784,000 views and selling actions climbed 9% in May. The platform kept surfacing buyers and sellers who are close to a move.

-

Start here: Re-run your borrowers above 7%, pull your Likely to Sell list and run CMAs, and reach the clients already searching before they open a portal.

The spring was supposed to stall. Mortgage rates climbed to 6.53% the week ending May 28, the highest level since last August, after jumping nearly 30 basis points in five weeks on geopolitical volatility and a hot inflation print. Kevin Warsh took over as Fed chair from Jerome Powell in mid-May, and Zillow trimmed its 2026 home-sales growth forecast to 1.2% from 4%. And yet, the Realtor.com May report called it the most active spring market in four years. Pending sales rose a sixth straight month. Purchase applications ran about 7% above last year. And inside Homebot, selling actions climbed 9% while clients quietly studied buydowns with the AI assistant.

This is a working market. The lenders and agents leaning into it are the ones getting paid.

What's Happening in the Market

Rates Jumped to 6.53% - The Spring’s Cheapest Money Is Gone, For Now

The 30-year fixed averaged 6.53% the week ending May 28, up from 6.51% the week before. Rates climbed about 30 basis points over five weeks to their highest level since August 2025. Two things pushed them: geopolitical volatility lifted oil prices, and April inflation came in at 3.8% annually, a three-year high.

The Fed held rates steady at its April meeting for the third time in a row, an 8-4 vote that was the most divided since 1992. Kevin Warsh has since taken over as chair, with his first meeting set for June. Even with the recent climb, rates are still 36 basis points below where they sat a year ago, when the 30-year averaged 6.89%.

For Lenders:

- The refi pool is real even at 6.53%. Refinance applications ran about 20% above last year in late May. Pull your 2024 and early-2025 borrowers who locked above 7% and re-run their numbers this week.

- Rate volatility is back, so lock-and-float conversations matter again. Have a clear position ready before the call instead of reacting after a bad day in the bond market.

For Real Estate Agents:

- A half-point swing rattles buyers. Reset the frame: the low-to-mid 6s is the planning range, not a reason to wait for a number that may not come.

- Predictability is what gets people off the fence. Buyers who understand the range act. Buyers waiting for a headline keep renting.

For Both:

- Sell the plan, not the headline rate. The clients who move are the ones who understand what 6.53% means for their payment.

The Spring That Wasn’t Supposed to Happen - Most Active in Four Years

Higher rates and geopolitical uncertainty were supposed to sideline buyers and sellers. Instead, the Realtor.com May report shows the most active spring market in four years. Pending sales rose for a sixth straight month, new listings hit their highest May level since 2022, and median list prices fell 2.4% year over year, the steepest drop in the data since 2017. Sellers adjusted their expectations, and buyers rewarded them.

The supply story is uneven but improving. National active listings are up 4.6% year over year, with new listings surging in the Northeast and Midwest after months of decline. At the same time, the listing landscape itself is splitting apart. Compass, Zillow, and Rocket are fragmenting private exclusive listings across four-plus platforms, so the buyer who used to check one portal now has to check several.

For Lenders:

- The buyers rewarding price cuts need pre-approvals in hand now. Get ahead of the offer, not behind it.

- Co-sponsor your agent partners to stay visible in the same client digest month after month. As listings scatter across portals, shared visibility is what keeps you in the deal.

.png)

For Real Estate Agents:

- Sellers who price to the 2.4% reality are the ones getting offers. Update your listing presentation with local price and inventory data so your sellers price to sell, not to sit.

- The pre-search relationship beats portal placement. The moment your client opens a portal, they become a shared lead. Be the call they make first.

For Both:

- As listings fragment, owning the client conversation before the search starts is worth more, not less. The relationship is the one thing no portal can replicate.

The Payment Is the Conversation - Buydowns and Concessions Take Center Stage

With rates in the mid-6s and list prices easing, the monthly payment is the decision, not the sticker rate. Sellers cutting prices have room to fund concessions, and buyers are doing the math before they ever sign anything. Purchase applications still ran about 7% above last year through May, even as week-to-week volume cooled with the rate climb and hit its slowest weekly pace since April.

The lever moving deals right now is the seller-paid buydown. It lowers the payment in the early years without forcing the buyer to wait for rates to drop. This is exactly what Homebot clients are researching on their own, before they pick up the phone.

For Lenders:

- Model 2-1 and permanent buydowns funded by seller concessions on your next batch of pre-approvals. Show the payment, not the rate. Your refi-curious borrowers above 7% belong on the same call list.

For Real Estate Agents:

- Write seller-paid buydowns and concessions into your offers. With sellers cutting prices, the room is there. The agents structuring the payment are the ones getting deals to the table.

For Both:

- The payment is what closes the deal. Lead every buyer conversation with it.

What We’re Seeing in Homebot Engagement

The market cooled in the headlines and stayed busy in the data. Across 10M+ homeowners on the platform, engagement in May concentrated exactly where the market is moving: buyers searching, sellers raising their hands, and clients studying the payment lever. Here’s what stood out:

What We're Seeing Inside Homebot

What Clients Took Action On

Where Homeowners Engaged

1. Listings Search Is the #1 Engagement Source - Up 4%

Listings search drove 784,000 engagements in May, up about 4% from 757,000 in April, making it the single largest source of client activity. Add listing-details views and the platform logged roughly 1.36 million listing-related engagements in the month. That is buyer intent in its earliest form, the pre-search browsing that happens before a client ever opens a portal. These clients will show up in your Likely to Buy and/or Highly Engaged Opportunity lists. Start the conversation before a portal lead form does it for you.

2. Selling Actions Climbed 9% - Sellers Are Leaning In

Selling was the top client action in May at roughly 1,250, up about 9% from April, with ownership actions close behind at around 1,130. This lines up cleanly with what Realtor.com is seeing nationally: sellers are adjusting their expectations and getting back in. A selling action inside the platform is one of the strongest seller-intent signals there is. Run through your Likely to Sell opportunity list. See if your clients might be interested in a CMA, and start a conversation early. Can be easy as “Just wanted to check in to find out if your home still fits your needs.”3. Buydowns Are the #2 AI Conversation - Up 22%

Buydown and seller-concession questions were the second most-asked AI assistant topic for the second month running, up about 22% from April. Assumable loans surfaced in the mix too. Clients are pre-researching the payment lever on their own time, which means the buydown conversation is already half-started by the time they call. Have your 2-1 and permanent buydown scenarios ready so you can meet them where they already are.

4. 1.74M Client Actions in May - The Database Didn’t Pause

The platform logged 1.74 million client actions in May across 10M+ homeowners. While national momentum cooled week to week and the headlines turned cautious, homeowners kept checking equity, browsing listings, and asking financing questions. The market does not pause for a noisy rate week. Neither do the people in your database. The transactions are forming now, whether or not the headlines say so.

What Lenders & Agents Should Do Right Now to Work Their Database

Lenders

- Re-run the 7%-plus vintage. Refinance applications ran about 20% above last year in late May. Pull every borrower who locked above 7% in 2024 and early 2025 and re-run their numbers this week, before they go shopping somewhere else. Review your Ready for Refi Opportunity list in your Homebot account.

- Build the buydown menu before the call. Buydown and seller-concession questions were the #2 AI conversation inside Homebot two months running, up 22%. Have 2-1 and permanent buydown scenarios ready so the answer is on the table the moment a client asks.

- Work your Cash Out Capable and Refi Ready lists. These clients are pre-search and already qualified. Start with the ones who are also engaging with equity content, where the signal jumps from qualified to interested.

Real Estate Agents

- Pull your Likely to Sell Opportunity list and run CMAs. Selling was the #1 client action in May, up 9%. The sellers raising their hand are already in your database. Get the CMA in front of them before they call anyone else.

- Reprice to the 2.4% reality. List prices fell 2.4% year over year, the steepest drop since 2017. Update your listing presentation with local price and inventory data so your sellers price to sell.

- Negotiate concessions into every offer. Sellers cutting prices have room to fund a buydown. Write it in. The payment is what gets the offer accepted and the deal closed.

For Both Lenders and Real Estate Agents

- Reach the searchers before the portal does. Listings search was the #1 engagement source in May, up 4%, with about 1.36 million listing views across the platform. Those are buyers in pre-search mode. Reach out before they fill out a portal form and become someone else’s lead.

Closing Thought

The professionals winning this spring did not wait for clean headlines.

- They re-ran the 7%-plus vintage when refis crossed 20% above last year.

- They pulled their likely-to-sell list when selling actions climbed 9%.

- They reached the buyers driving 1.36 million listing views before those clients ever opened a portal. Homebot surfaces these signals before they become obvious, so the conversation starts while there is still a conversation to have.

The clearest signal in a noisy market is the client already raising their hand inside Homebot. Reach them first.

See what Homebot surfaces in your database: Request a demo to get started..