Monthly Mortgage Digest

Fed Holds Steady as Buyers Return, Affordability Improves, and 2026 Shows Early Signs of Market Momentum

.png)

Welcome back to the Monthly Mortgage Update, your resource for rate trends, homeowner behavior, and what it means for your pipeline.

January gave us the Fed's first decision of the year. We also saw early signs that buyers are coming back. And homeowners are starting to think more seriously about their equity and what to do with it.

The market isn't moving fast. But it is moving. And the direction matters.

This month, we're breaking down what's changing in the market, how we're seeing it affect homeowners, and how you should respond.

What's Happening in the Market

1. The Fed Held Rates Steady

The Federal Reserve voted to keep rates where they are. No surprise there. Fed Chair Powell said the economy is in good shape, but inflation is still a little high.

Here's the good news: mortgage rates are almost a full point lower than they were a year ago. The 30-year fixed is around 6.15% right now. Last January it was over 7%.

What this means for lenders and agents:

- Rates between 5.5% and 6.5% are the new normal. That's not what everyone hoped for, but it's predictable.

- Rocket Mortgage's Bill Banfield said it well: "The housing market doesn't turn on a single rate decision. It turns when people can plan with confidence."

- Predictability is what gets people off the sidelines. Use that in your conversations.

2. Buyers Are Showing Up

Pending home sales hit 56,252 for the week ending January 23. That's the highest we've seen in years. Purchase applications are up 18% compared to last year.

New listings are up too. About 54,000 homes came on the market last week. That's more than the same week last year. Prices are holding steady. Price cuts haven't increased. This all points to a stable market, not a stressed one.

What this means for lenders and agents:

- The 18% jump in purchase applications isn't a prediction. It's already happening.

- People who waited in 2025 are starting to act.

- Spring could be stronger than last year. The time to get positioned is now, not later.

3. Affordability Is Getting Better

First American says household income will grow faster than home prices this year. That hasn't happened in a long time.

Right now, the typical mortgage payment takes about 33% of median income. That's down from 38% in late 2023. Zillow thinks 20 of the 50 largest metros will hit the 30% affordability mark by the end of the year.

What this means for lenders and agents:

- When incomes grow faster than prices and rates stay flat, buyers who thought they were priced out can suddenly qualify.

- This is especially true in the Midwest and Northeast, where inventory is still tight.

- If you have clients who paused last year, now's the time to run the numbers again.

4. Down Payment Options Are Expanding

The Trump administration decided not to move forward with the 401(k) withdrawal idea. But there are other conversations happening.

The Community Home Lenders of America proposed a new idea. It would let parents and grandparents gift up to $50,000 in stocks to help a child buy their first home. They'd get to defer the capital gains tax.

Meanwhile, there are now over 2,600 down payment assistance programs across the country. That's up 6% from last year. The average benefit is about $18,000.

What this means for lenders and agents:

- NAR data shows first-time buyers are putting 10% down on average. That's the highest in nearly 40 years. One in four got help from family.

- The average first-time buyer is now 38 years old.

- You need to have the down payment conversation earlier. Know your DPA programs. Understand gift fund rules. Help buyers get creative.

5. Foreclosure Activity Went Up, But Don't Panic

Foreclosure auctions rose 48% compared to last year. That sounds scary, but context matters. We're still 39% below pre-pandemic levels.

This is the market returning to normal. Not a crisis. Homeowners still have strong equity. The job market is solid. Florida, Georgia, and Texas saw the biggest increases, but sales rates at auction actually dropped. Buyers are cautious, not desperate.

What this means for lenders and agents:

- Rising foreclosure volume isn't a warning sign. It means properties stuck in forbearance are finally working through the system.

- For agents, this could mean more inventory in some markets.

- For lenders, some borrowers may need help with a refi or modification. Keep an eye on your servicing clients.

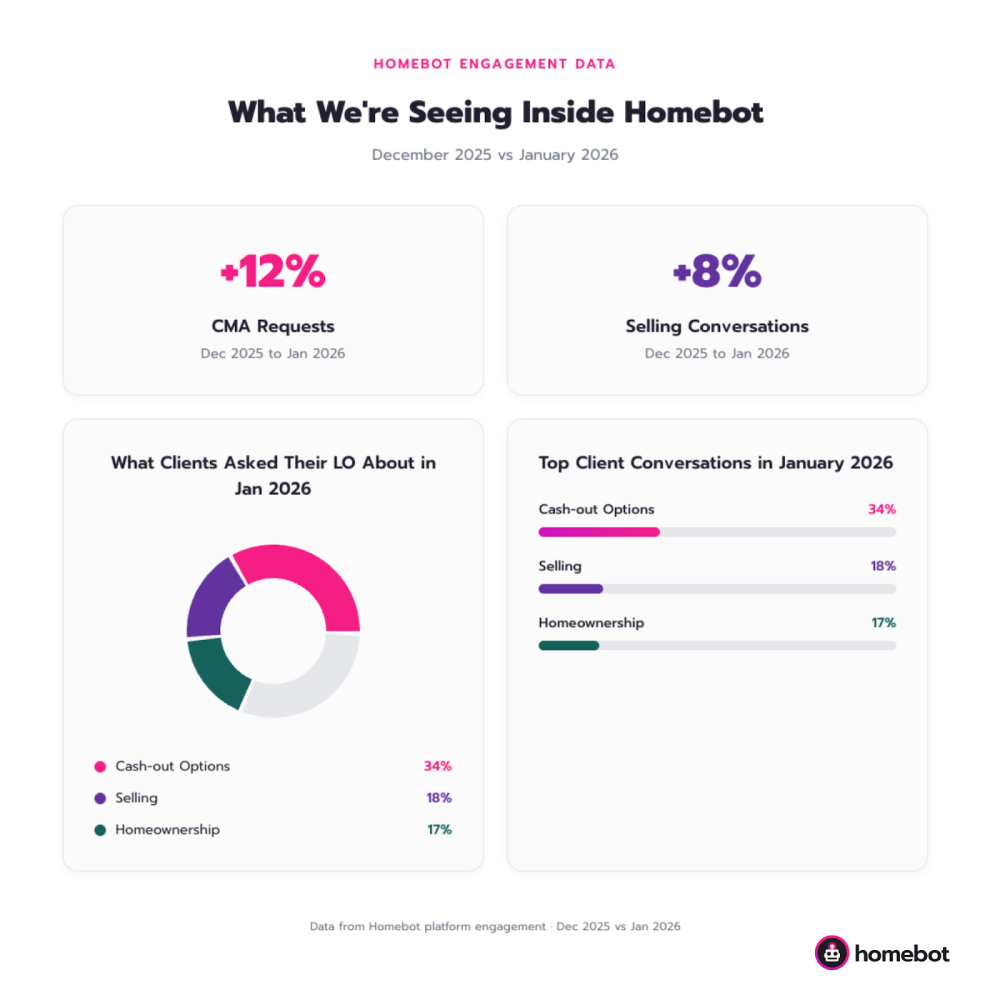

What We're Seeing in Homebot Engagement

These market trends are showing up in how homeowners interact with Homebot.

1. Equity Is Top of Mind

In January, 34% of client direct messages to their LO were about cash-out options. That was the top topic by far. Selling came in second at 18%, followed by general homeownership questions at 17%.

Homeowners are sitting on equity and thinking about what to do with it. They're reaching out to talk through their options.

2. Selling Conversations Are Picking Up

We saw an 8% increase in clients asking their LO about selling through Homebot. CMA requests were up 12% as well.

People aren't just thinking about selling. They're starting to take action and ask real questions.

3. Search Activity Is Up

More homeowners are using Private Home Search. Saved searches and likelihood to sell scores are increasing, especially in markets where inventory is growing.

People who were casually browsing are starting to look more seriously.

What to Do Next

- Check on borrowers with rates above 6.5%. These clients may be entering refinance territory. Use Homebot's key client lists to see who's exploring scenarios. Reach out before they start shopping around.

- Reconnect with first-time buyers. Affordability is improving. DPA programs are stronger than ever. If someone paused because of down payment concerns, it's time to revisit their file.

- Focus on high-engagement homeowners. Your Homebot dashboard shows who's actively engaging. These aren't cold leads. Prioritize outreach to homeowners viewing their digest, exploring move-up scenarios, or searching for homes.

- Update your market story. Buyers and sellers want context, not just data. The story has changed: rates are stable, affordability is improving, and inventory is growing. Lead with that.

- Strengthen your referral partnerships. Trust matters more than ever. Use Homebot Network to build partnerships with professionals who share clients with you. Build those relationships before spring kicks in.

Closing Thought

The market isn't waiting for a big breakthrough. It's building momentum slowly. Rates are lower than last year. Affordability is improving. Buyers are coming back.

The professionals who win in 2026 won't be the ones waiting for perfect conditions. They'll be the ones who stayed close to their database, spotted the signals, and showed up when it mattered.

Follow the Homebot Market Update for monthly insights on what's moving the market and what your clients are telling us through their behavior.

Identify ready-to-transact customers in your database. Request a demo of Homebot today.

.png)