Loan Officers

2026 Mortgage Rates Just Dropped Below 6%: What Lenders Need to Know Now

.png)

For the first time in nearly three years, mortgage rates briefly dipped below 6% on January 10, 2026. If you're a loan officer wondering what this means for your pipeline—and how to capitalize on the moment—here's what's happening, what's expected, and how to turn this market shift into closed loans.

What's Driving the Drop in 2026 Mortgage Rates?

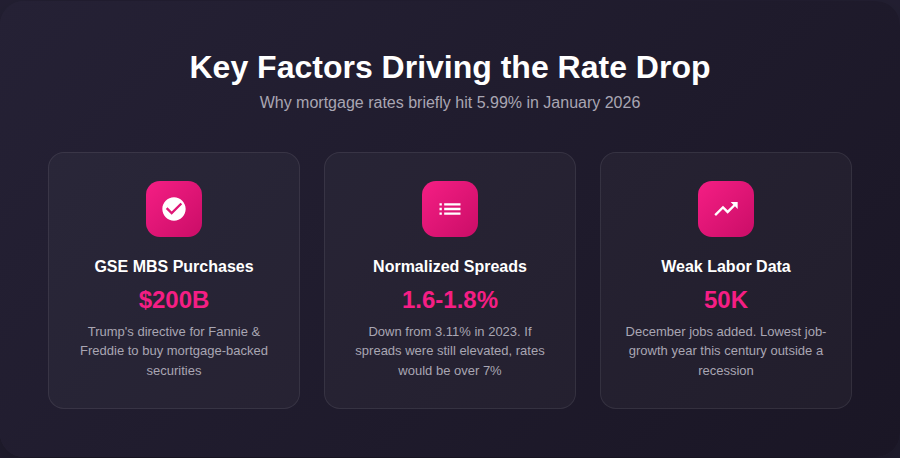

The rate decline wasn't random. According to HousingWire's analysis, President Trump's directive for the GSEs to purchase $200 billion in mortgage-backed securities sent spreads tumbling to near-normal levels, pulling rates down with them.

Key factors behind the move:

- Rates briefly touched 5.99% on Friday before settling at 6.06% by week's end

- Mortgage spreads are near normal (1.60%–1.80%) compared to 3.11% in 2023—if spreads were still elevated, rates would be over 7% today

- Weak labor data is providing tailwinds—December's jobs report showed just 50,000 jobs added, the lowest job-growth year this century outside of a recession

The spread story is the unsung hero here. Even when yields tick up, compressed spreads have kept rates more affordable than they'd otherwise be.

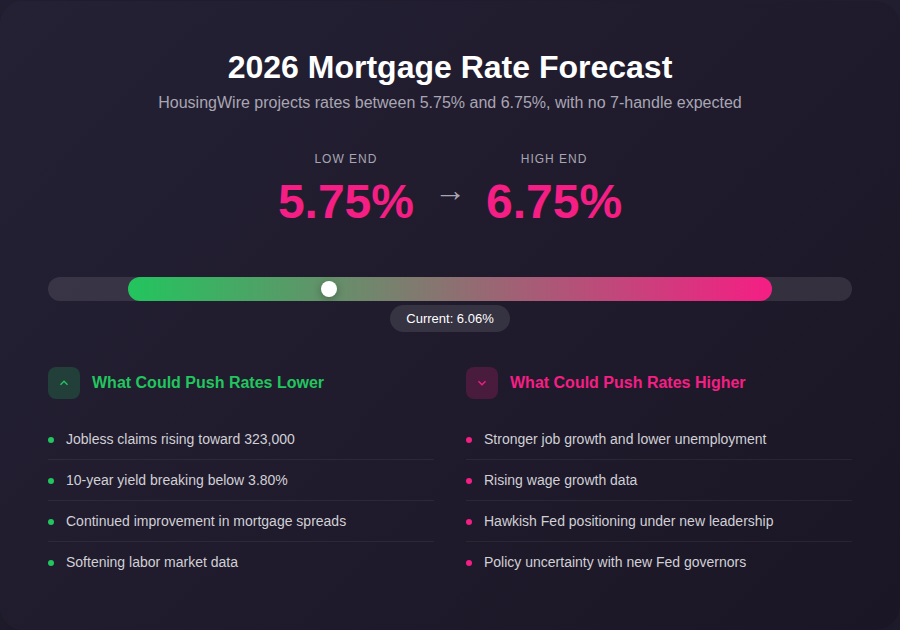

Mortgage Rate Predictions for 2026: Where Are We Headed?

HousingWire's 2026 forecast puts mortgage rates in a range of 5.75% to 6.75%—notably, no 7-handle is expected this year. That's a meaningful shift from the volatility lenders navigated in 2023-2025.

What could push rates lower:

- Jobless claims rising toward 323,000

- 10-year yield breaking below 3.80%

- Continued improvement in mortgage spreads

What could push rates higher:

- Stronger labor data (more job growth, lower unemployment, rising wages)

- Hawkish Fed positioning under new leadership

- Policy uncertainty with incoming Fed Chairman and potential new governors

The bottom line: 2026 is shaping up to be a year of recalibration, but the rate environment looks more favorable than anything lenders have seen since 2021.

What Lower Rates Mean for Refi and Purchase Volume

When rates drop, borrowers pay attention. According to Jefferies analysts cited by HousingWire, a 22-basis-point decline in the 30-year fixed rate historically drives a 15% to 25% increase in refinancing activity.

The refi outlook by the numbers:

- Refinancing accounted for 28% of mortgage activity in 2025

- Fannie Mae projects refi volume to jump 64% in 2026, reaching approximately $882 billion

- Lenders are already fielding "hundreds and hundreds" of borrower inquiries following the rate drop

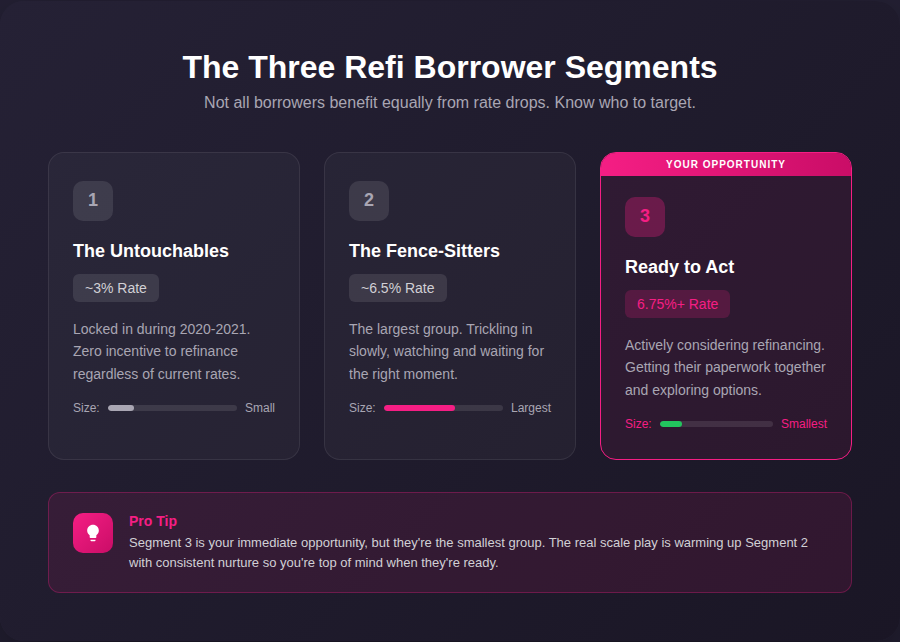

The three borrower segments to watch:

- The untouchables — Homeowners locked in at ~3% with zero incentive to move

- The fence-sitters — The largest group, holding mortgages near 6.5%, trickling in slowly

- The ready-to-act — Borrowers above 6.75% who are actively considering refinancing

That third group is your immediate opportunity—but they're also the smallest segment. Winning requires reaching the right borrowers before they start shopping around.

The Purchase Side: Inventory Dynamics to Watch

Lower rates don't just impact refi—they shift purchase dynamics too. HousingWire reports that year-over-year housing inventory growth has slowed dramatically:

Inventory trends:

- Growth dropped from 33% at its peak in 2025 down to just 9.99% as 2026 begins

- Weekly inventory fell from 720,102 to 686,784 (Jan. 3–Jan. 10)

- Price cuts are at 34.7%, up slightly from 34% last year

Why this matters for lenders:

- When rates fall below 6.64% and head toward 6%, housing demand improves

- More buyers entering the market = faster inventory absorption

- If rates stay at 6.25% or lower with slowing inventory growth, prices are likely to firm up rather than decline

This creates urgency on both sides: refi borrowers who need to act before rates tick back up, and purchase borrowers facing tightening inventory if they wait.

How Lenders Can Capitalize on This Moment

Rate drops create windows of opportunity, but those windows close fast. The lenders who win aren't blasting generic "rates are down!" emails to their entire database. They're reaching the right borrower with the right message at the right time.

That requires a shift from reactive marketing to proactive, signal-based outreach, and the right technology to make it scalable. Here's how top lenders are getting ahead.

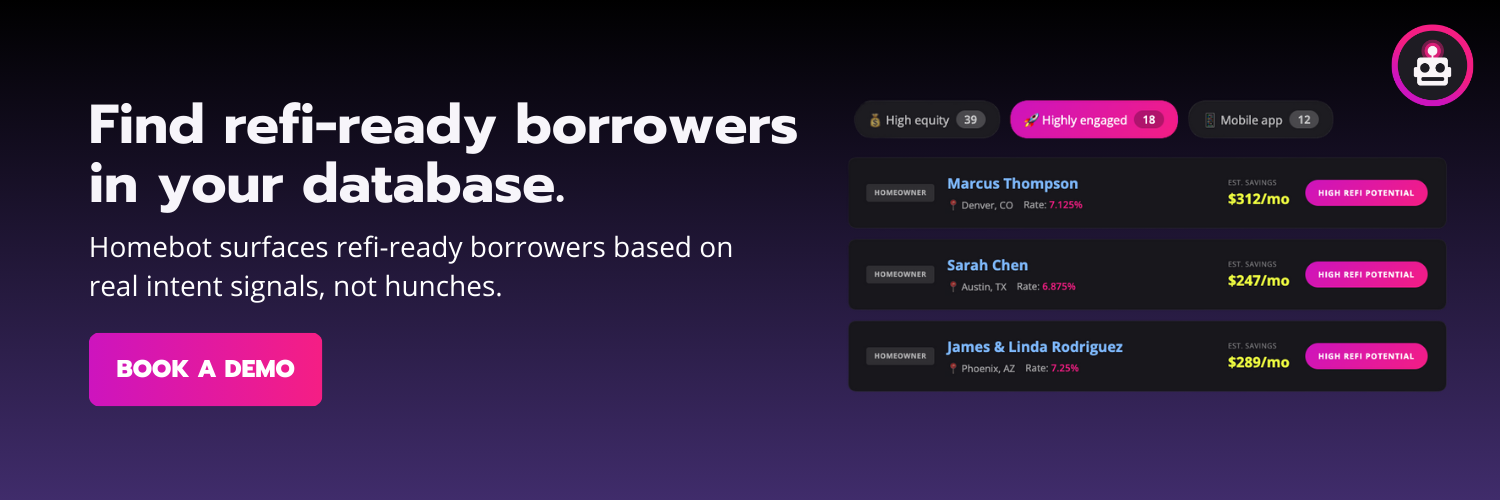

1. Identify Refi-Ready Borrowers Before They Shop

Not every borrower in your database is a refi candidate. The key is segmentation- filtering by:

- Current rate

- Equity position

- Engagement behavior

This helps you prioritize borrowers above 6.5% to 6.75% who have enough equity to make a move worthwhile.

Homebot makes this easy by tracking your clients' equity positions, current rates, and engagement signals automatically. When rates drop, you don't have to guess who might benefit. Homebot surfaces the borrowers most likely to act.

How it works:

- See which clients just opened their home equity digest

- Know who's running refinance scenarios in real time

- Reach out based on actual intent signals, not guesswork

That's not a cold call. It's a well-timed conversation with someone already thinking about their options. And when you reach out, you're not just talking rates. You're checking in on their goals, their equity position, and how their home fits into their broader wealth-building strategy.

2. Stay Top of Mind During Rate Volatility

Your clients are seeing the same headlines you are: rate drops, policy announcements, economic uncertainty. They have questions, and they're going to get answers from someone. The lenders who stay top of mind are the ones providing consistent, personalized value, not just showing up when they need something.

This means regular touchpoints with content that's actually relevant to each client's situation: their home's value, their equity position, what's happening in their specific market. Generic newsletters don't cut it anymore.

Homebot's automated monthly digests deliver exactly this:

- Their home's current estimated value

- Their equity position and what they can do with it

- Local market trends and recently sold comps

- Refinance and buying power scenarios

This automated email ensures you're not chasing clients down. You're already their trusted source when they're ready to make a move.

3. Catch Purchase Intent Early

With inventory tightening as rates improve, buyers need to move faster, and so do you. The lenders closing purchase deals are the ones spotting intent before borrowers formally raise their hand. That means tracking behavior: who's browsing in new areas, who's running affordability numbers, who's engaging more frequently with market content.

Homebot shows you when clients are actively in-market with intent signals you can act on:

- Clients searching for homes in new zip codes

- Borrowers running affordability calculators

- Engagement spikes that indicate readiness to transact

That signal tells you exactly when to reach out, not with a generic check-in, but with relevant insights and a clear path forward.

4. Turn Market Moments Into Pipeline

Lower rates are a headline. What you do with that headline determines whether it becomes business.

The challenge is doing all of this at scale. You can't manually track equity positions, monitor engagement signals, and send personalized nurture across hundreds of contacts. The lenders gaining ground right now are the ones with systems that deliver personalized insights automatically, surfacing the right opportunities so they can focus on high-value conversations.

Homebot gives you that infrastructure:

- Automated nurture running in the background

- Intent signals surfacing the right opportunities

- Personalized content positioning you as the expert

You're not hoping for callbacks. You're systematically converting market moments into closed loans.

The Bottom Line: Refi Boom Success Starts With Your Database

2026 mortgage rates are off to an encouraging start. With rates briefly touching the 5s and forecasts calling for a 5.75%–6.75% range, lenders have their best rate environment in years.

The opportunity:

- Refi volume projected to surge 64%

- Purchase demand poised to tighten already-constrained inventory

- Borrowers actively seeking guidance on what lower rates mean for them

The question isn't whether opportunities exist. It's whether you're positioned to capture them.

Ready to see how Homebot helps you reach the right borrower at the right moment? Request a demo and turn this rate environment into your strongest year yet.