Monthly Mortgage Digest

Fed Holds Steady as Spring Buyers Return, Inventory Climbs, & Buydowns Take Over the Conversation

Welcome to the May issue of The Monthly Mortgage Digest. May 2026 is not an easy market to read. The Fed held rates for a third meeting in a row with the most dissents in 34 years. Powell exits in two weeks. Mortgage rates are stuck in the low 6s, oil prices are climbing, and the headlines keep cycling between "rate cuts coming" and "rate cuts cancelled." And yet - purchase applications are running 21% above last year. Sellers are pricing realistically out of the gate. CMA requests on Homebot grew while clients quietly studied buydown structures with the AI assistant. The market didn't pause to wait for clean headlines.

This month we're covering what's actually happening in the market right now and what over 10M homeowners are doing in Homebot.

The takeaway is simple: this is a working market, and the lenders and agents leaning into it are the ones getting paid.

What's Happening in the Market

1. The Fed Held Steady (Again)

The Federal Reserve held the federal funds rate at 3.5% to 3.75% at the end of April. It was the third hold in a row. The vote was 8 to 4, and according to NerdWallet's May mortgage outlook, that's the most dissents the FOMC has seen in 34 years. Powell's term ends May 15. Kevin Warsh is expected to take the chair next. Most economists don't see a cut coming any time soon.

What it means for lenders:

- Stop pricing your strategy around future rate cuts. They aren't coming this quarter.

- Lead with buydowns, ARMs, and lender-paid temporary rate reductions. These are the affordability levers in 2026, and clients are already asking about them.

What it means for agents:

- Stop letting buyers defer with "I'll wait for rates to come down." Frame every conversation around what's possible at today's payment.

- Pair buyers with a lender who can run real-time buydown and concession scenarios. Affordability decisions live in those calls.

What it means for both:

- Use rate stability as a planning advantage. Clients can commit to a payment target when the number isn't whipping around week to week.

2. Rates Are Stuck in the Low 6s, but Down From Last Year

The 30-year fixed averaged 6.30% on April 30, per Freddie Mac. It briefly dipped close to 6% in mid-April before climbing back. A year ago this week it was 6.76%. That's an improvement, and buyers are responding. Mortgage purchase applications are running 21% above year-ago levels, and refinance applications are up 51%.

What it means for lenders:

- Lead refi conversations with year-over-year payment savings, not headline rates. Anyone who locked at 7%+ in 2023 or 2024 has real room to move at 6.30%.

- Refi applications are up 51% YoY. The cohort is back. Pull your high-rate client list this week and run scenarios.

What it means for agents:

- Anchor every buyer conversation in monthly payment targets. Buyers think in dollars per month, not basis points.

- Use the YoY rate improvement story with sellers who are also buying. Their move-up purchase comes with a better rate than they expect.

What it means for both:

- Purchase applications are running 21% above last year. Real demand is back in the market. Buyers are out there, and they're moving.

3. Spring "Delivered" Despite the Noise

Active listings hit 1,002,935 in April, up 4.6% year over year. New listings climbed 8.7% month over month. Median list prices fell for the sixth straight month. And the share of sellers cutting prices actually went down. That last point is the one to sit with. It means sellers are pricing realistically out of the gate instead of testing the market and dropping later. Realtor.com's chief economist called the month a quiet win for the spring market.

What it means for lenders:

- More inventory means more pre-approval conversations. Get ahead of buyer search activity by making sure clients know exactly what payment they're shopping with before they start touring.

- Buyers shopping today have negotiating room. Build buydown and seller concession structures into the upfront pre-approval conversation, so the client walks into offers with options ready.

What it means for agents:

- Pricing strategy now beats listing timing. Homes priced to current comps clear in days. Aspirational pricing sits and requires cuts later.

- Update your listing comps weekly. Median prices have fallen for the sixth straight month, so last year's comps are no longer relevant for sellers entering the market today.

What it means for both:

- The buyer conversation is shifting from "is there anything?" to "is this the one?" Position yourselves as advisors who can run specific scenarios, not just talk market generalities.

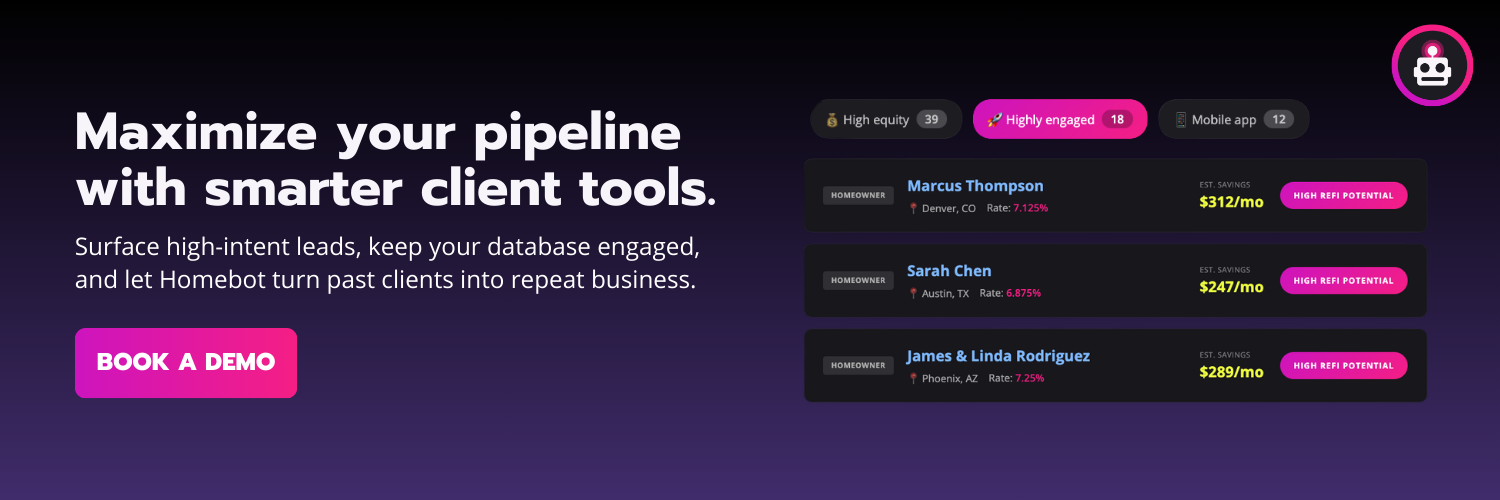

What We're Seeing in Homebot Engagement

Across the 10 million-plus homeowners using Homebot, April engagement told a clear story about where intent is concentrating: seller-side activity and creative financing. CMA requests grew month over month, the listings-search funnel drove over 1.3 million client touchpoints, and clients kept asking the AI assistant, lenders and agents the same question they were asking in March: how do I make a purchase work at today's rate?

Here's what stood out:

1. CMA Requests Up 2.7% - Sellers Are Doing the Math

CMA requests grew 2.7% month over month, with 1,157 homeowners running a Comparative Market Analysis in April. A CMA request is one of the strongest seller intent signals Homebot generates. It means a homeowner is actively pricing their property against current comps. Those 1,157 CMA-runners represent 1,157 conversations a real estate agent should be having this month, and 1,157 potential move-up loan opportunities for the loan officer attached to that client.

2. Selling Is Still the #1 Client Action

Selling led April with 1,140 client actions, followed by ownership at 1,030 and purchase at 896. Selling intent has now held above 1,100 actions for two consecutive months. That tracks with what Realtor.com reported in its April housing report, where new listings climbed 8.7% month over month and gains were strongest in the Northeast and Midwest. The seller-side pipeline inside Homebot is thicker than it has been in years. Most of those sellers will also be buyers in the same transaction window. The agent or lender who frames the listing and the next purchase together first wins both sides.

3. Clients Are Searching With Intent

Of the 1.74 million client actions in April, 756,620 happened in listings search and 563,110 in listing details. That's three of every four actions on the platform tied to real properties for sale. Clients are running affordability scenarios, comparing payments side by side, and saving favorites to revisit. Homebot tracks who is looking at what, and how often. Pull a weekly list of clients who have viewed the same property three or more times in seven days. Those clients have a stated buying intent that converts at materially higher rates than cold database outreach.

4. Buydowns Are the #2 AI Topic - Two Months Running

"Buy downs as a seller concession" was the second most-asked topic in client DMs to the Homebot AI Assistant in both March and April. Clients are teaching themselves how to make a purchase work at 6.30%. By the time they bring up a buydown with you, they have already done some math on their own. Build a one-page explainer that covers temporary 2-1 buydowns, permanent rate buydowns, and how to negotiate the concession from a seller. Send it in your next ten outreach touches. Lenders and agents who lead with these answers convert at higher rates than those who wait for the buyer to ask first.

What Lenders & Agents Should Do Right Now to Work Their Database

Lenders

- Pull your refi list. Identify every past client still sitting on a rate above 7%. Run a quick scenario at 6.30%. Reach out this week with the payment delta in writing. With purchase apps up 21% YoY and refi apps up 51%, the cohort that locked at 7%+ in 2023 and 2024 is the most actionable list on your books.

- Build a buydown one-pager. Cover temporary 2-1 buydowns, permanent rate buydowns, and how to negotiate the concession from a seller. Buyers are already running this math on their own through Homebot's AI assistant. Walk into the conversation with the answers ready instead of catching up to the question.

- Connect CMA activity to your move-up loan pipeline. When a client of yours runs a CMA, that's not just a listing signal for the agent. It's a next-purchase loan opportunity for you. Track CMA-runners on your books and start the financing conversation before they sign with another lender.

Real Estate Agents

- Call your CMA-runners. Anyone who pulled a Comparative Market Analysis in the last 30 days has stated selling intent. Lead with "I noticed you ran a market report on your home. What's on your mind?" That single question opens more listing conversations than any market update ever will.

- Update your listing presentations. Lead with current comps and price-realistic positioning. Show sellers what April's data says: new listings up 8.7% month over month, median prices down for the sixth straight month, and the share of sellers cutting prices actually declining. The market rewards realistic pricing out of the gate.

- Use listings-search activity to prioritize buyer outreach. Pull a weekly list of clients who have viewed the same property three or more times in seven days. Those are stated buying intent signals worth a phone call this week, not a generic email next month.

For Both Lenders and Real Estate Agents

- Reset client expectations for Q2 around stability. The Fed isn't moving. Powell is leaving May 15. Even if Warsh comes in dovish, mortgage rate response will be slow. Build your pipeline on the assumption that rates stay in the low 6s through Q3, and frame every client conversation around what's possible at today's number rather than what might happen later.

Closing Thought

The lenders and agents winning in May are not waiting for a perfect rate or a Fed pivot. They're staying close to the data, reading client intent before it becomes a phone call, and walking into conversations with answers ready - not just rate updates. Homebot surfaces these signals before they become obvious: who ran a CMA last week, which listings a client has viewed three times, who's still sitting on a 7% rate. Use that information. The professionals who act on it in May will own the pipeline everyone else is scrambling to build by July.

The clearest signal in a sticky market is the client already raising their hand inside Homebot. Show up for them.

See what Homebot surfaces in your database: Start free at homebot.ai